2 Reasons to Like GRC and 1 to Stay Skeptical

What a fantastic six months it’s been for Gorman-Rupp. Shares of the company have skyrocketed 53.4%, hitting $69.01. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Following the strength, is GRC a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Does Gorman-Rupp Spark Debate?

Powering fluid dynamics since 1934, Gorman-Rupp (NYSE:GRC) has evolved from its Ohio origins into a global manufacturer and seller of pumps and pump systems.

Two Positive Attributes:

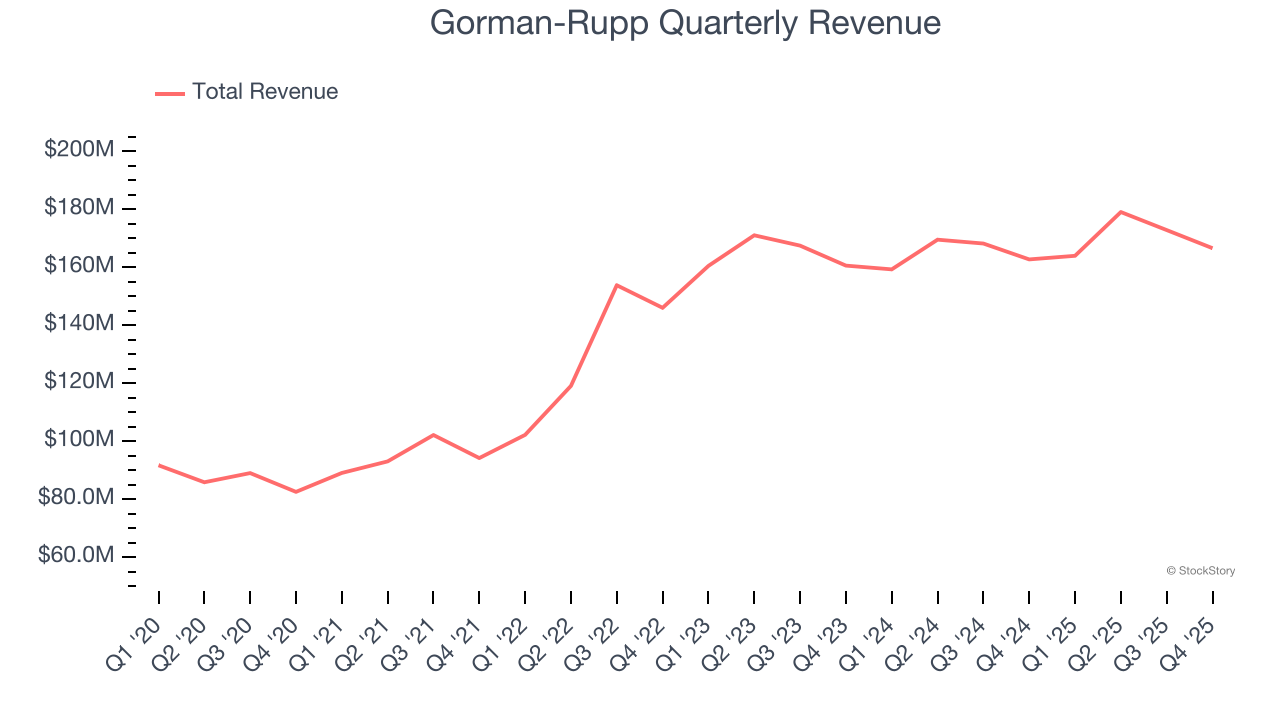

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Gorman-Rupp’s sales grew at an exceptional 14.4% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

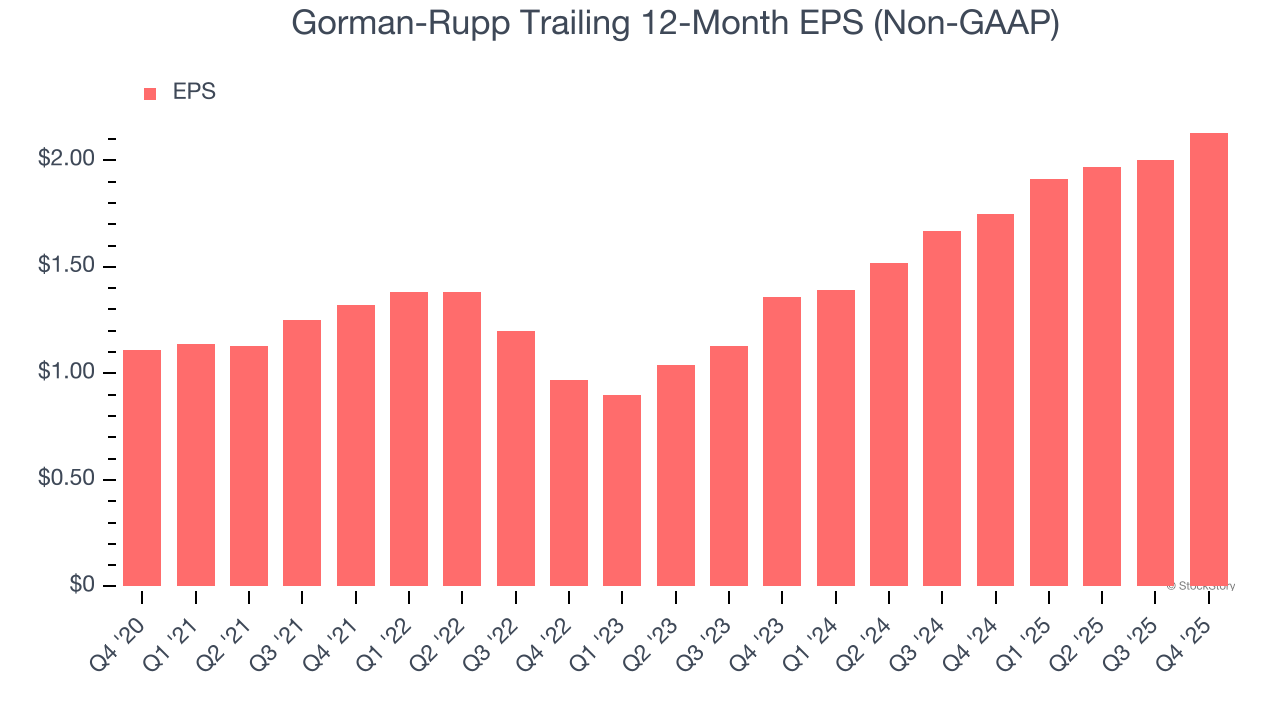

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Gorman-Rupp’s remarkable 13.9% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

One Reason to be Careful:

Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Gorman-Rupp’s revenue to rise by 5%. Although this projection indicates its newer products and services will spur better top-line performance, it is still below average for the sector. At least the company is tracking well in other measures of financial health.

Final Judgment

Gorman-Rupp’s merits more than compensate for its flaws, and after the recent rally, the stock trades at 29.8× forward P/E (or $69.01 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Gorman-Rupp

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.