PNC vs. HBAN: Which Bank Stock Offers Stronger Growth Story?

When investors seek scale and stability among bank stocks, The PNC Financial Services Group, Inc. PNC and Huntington Bancshares Incorporated HBAN often emerge as prominent contenders. Both banks have built strong franchises through diversified lending operations, expanding deposit bases, and a broad focus on consumers, businesses and wealth management clients. However, both banks differ meaningfully in scale, profitability, growth strategy and shareholder returns.

PNC is expected to announce earnings on July 15 and Huntington is anticipated to report quarterly results on July 23. Ahead of these releases, investors may be wondering which of the two stocks offers the more compelling growth opportunity. Let us delve deeper and anlyze each bank growth prospects.

The Case for PNC

PNC Financial expects net interest income (NII) momentum to continue, supported by loan growth, asset repricing, deposit expansion, market investments, operational efficiencies and stabilizing funding costs. Over the six years ended 2025, the company’s NII saw a compound annual growth rate of 6.3%. Management expects NII to increase 14% year over year in 2026.

The company is also undertaking a major expansion of its U.S. branch network. PNC plans to open more than 300 branches across nearly 20 markets, renovate its entire branch network by 2029 and hire more than 2,000 employees by 2030 to support growth and customer service. By expanding into high-growth markets, PNC aims to strengthen its position as a leading financial institution serving consumers and businesses of varying sizes.

PNC has also been diversifying its operations through acquisitions, partnerships and strategic alliances. In January 2026, the company completed its acquisition of FirstBank Holding Company, significantly expanding its presence in Colorado and Arizona. In May 2025, it agreed to acquire Aqueduct Capital Group, enhancing fund-placement capabilities at Harris Williams, its global investment banking subsidiary.

PNC remains committed to returning capital to shareholders. Following the 2026 stress test, the company announced an 18% increase in its quarterly cash dividend to $2 per share. It also has an active share-repurchase authorization. Of the 100 million shares approved for repurchase in July 2022, nearly 32 million remained available as of March 31, 2026.

However, PNC’s growth initiatives involve substantial costs. Management expects $325 million in merger and integration expenses in 2026, including $150 million in the second quarter of 2026. Technology investments, branch expansion and rising personnel expenses are also likely to keep operating costs elevated and pressure near-term profitability.

The Case for HBAN

Huntington has expanded its geographic reach and capabilities across several business lines through acquisitions. In February 2026, the company completed its merger with Cadence Bank, strengthening its presence in Texas and the southern United States while expanding its branch network to nearly 1,400 locations across 21 states. In October 2025, Huntington acquired Veritex Holdings, accelerating its organic growth strategy in Texas by increasing its presence in the Dallas-Fort Worth and Houston markets. HBAN expects acquisition synergies, fee-income growth and capital returns to help it generate a return on tangible common equity of 18-19% by 2027.

The bank’s organic growth prospects also appear favorable. Huntington expects stand-alone NII to increase 10-13%, while Cadence is projected to contribute an additional $1.77-$1.82 billion in 2026. Growth is expected to be supported by rising loan balances, and stabilizing deposit and funding costs.

Huntington is also expanding in faster-growing markets, including the Carolinas, Texas and Florida. The company has been hiring commercial bankers and opening branches to attract deposits and deepen relationships with middle-market customers.

On the capital-return front, Huntington increased its quarterly dividend by 3.3% in October 2021 and has maintained the payout since then. Management has indicated plans to repurchase at least $550 million of shares in 2026 and approved a $3-billion share-repurchase authorization to replace the prior program. However, the company continues to prioritize funding loan growth and investing in strategic initiatives. As a result, the pace of share repurchases could be constrained if loan growth, acquisition-related adjustments or regulatory capital requirements increase.

Huntington’s rapid expansion also presents meaningful execution risks. Management expects $1.1 billion in incremental Cadence-related expenses in 2026, excluding nearly $500 million of remaining one-time costs. Successful integration and cost realization will therefore be crucial to Huntington’s earnings outlook.

PNC & HBAN’s Earnings Growth Prospects

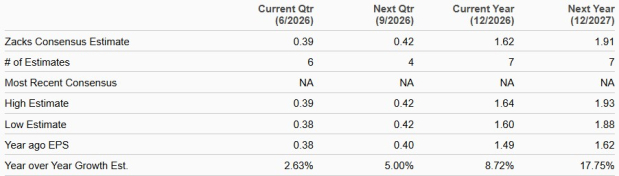

The Zacks Consensus Estimate projects Huntington’s earnings to rise 8.7% in 2026 and 17.8% in 2027.

Earnings Estimates

Image Source: Zacks Investment Research

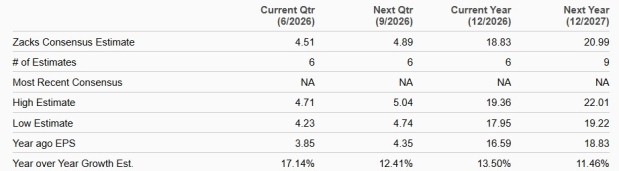

For PNC, the consensus estimate indicates earnings to increase 13.5% in 2026 and 11.5% in 2027.

Earnings Estimates

Image Source: Zacks Investment Research

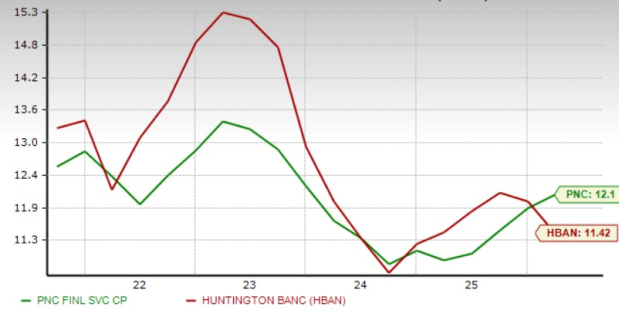

PNC & HBAN: Price Performance, Valuation & Other Comparisons

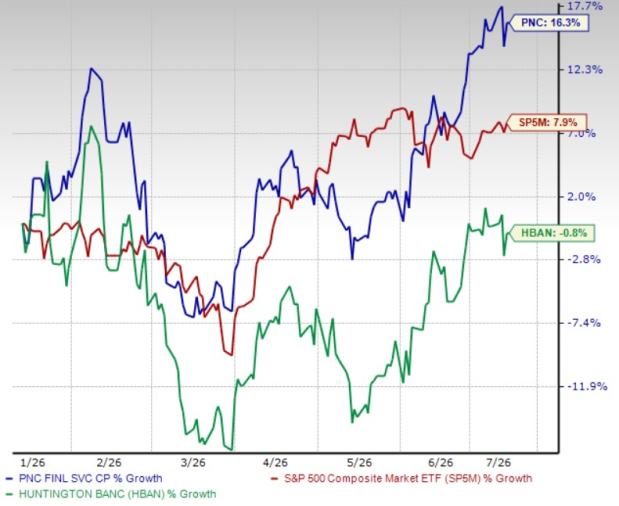

Over the past six months, PNC shares have jumped 16.3%, whereas Huntington shares have declined 0.8%. In comparison, the S&P 500 Index has advanced 7.9%.

Price Performance

Image Source: Zacks Investment Research

Based on price performance, investor sentiment toward PNC has clearly been stronger.

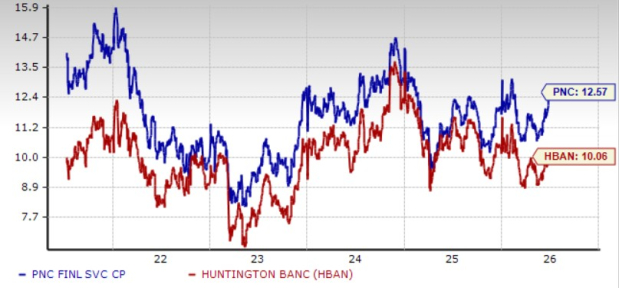

Huntington, however, appears more attractive from a valuation standpoint. HBAN currently trades at a 12-month forward price-to-earnings ratio of 10.06X, below PNC’s multiple of 12.57X.

Price-to-Earnings F12M

Image Source: Zacks Investment Research

PNC also has an edge in profitability. Huntington’s return on equity of 11.42% trails PNC’s 12.1%, suggesting that PNC is using shareholder capital more efficiently to generate profits.

Return on Equity

Image Source: Zacks Investment Research

HBAN or PNC: Which Has Better Potential

While Huntington offers stronger near-term revenue growth and a more attractive valuation, much of its expansion is acquisition-driven and accompanied by elevated integration costs, rising expenses and execution risks.

PNC, conversely, presents a more balanced investment case, supported by solid NII growth, superior profitability, stronger recent share-price performance and a more consistent capital-return strategy. Its expanding branch network, strategic acquisitions and improving operating momentum further strengthen its long-term growth outlook.

Therefore, despite trading at a premium valuation, PNC provides a more balanced investment profile by combining income generation with long-term growth potential.

Currently, HBAN and PNC carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).