Is Procedure Growth Broad-Based Enough to Support ISRG's 2026 Outlook?

Intuitive Surgical’s ISRG raised its full-year outlook on the first-quarter earnings call, primarily supported by a broadly diversified procedure growth profile. The management increased its 2026 da Vinci procedure growth guidance to 13.5-15.5% from 13-15%, reflecting confidence in sustained adoption trends.

The biggest growth driver continues to be U.S. general surgery, where procedures such as cholecystectomies and appendectomies surged 31% year over year. Growth was supported by increased after-hours utilization and higher adoption of the da Vinci 5 platform, which delivers utilization rates roughly 11% higher than those of the earlier Xi system.

International markets are also becoming an increasingly important contributor, with ex-U.S. da Vinci procedures growing 19%, driven by strong momentum in Europe, India, Korea, Taiwan, and Canada. Overseas procedures now represent 38% of total da Vinci volume, highlighting the growing diversification of Intuitive Surgical’s revenue base and long-term expansion potential.

However, some headwinds could limit upside. In the United States, bariatric procedures declined approximately 10%, as rising adoption of GLP-1 obesity drugs continues to reduce surgical demand in weight-loss procedures.

Internationally, China remains challenged by weak tender activity, domestic competition, and pricing pressure, while Japan continues to face slower adoption following reduced system placements.

Management remains cautious about external risks, particularly the potential impact of ACA subsidy changes in the U.S. healthcare market and broader macroeconomic pressures affecting hospital capital spending in Europe and Asia. While procedure growth appears broad-based enough to support 2026 guidance, sustaining momentum will depend on whether strength in general surgery and international expansion can offset these emerging structural headwinds.

Peer Updates

Boston Scientific BSX delivered solid procedural momentum in the first quarter of 2026, supported by strength across electrophysiology, cardiovascular, and neuromodulation franchises. The standout performer was electrophysiology, where sales surged 22% organically, driven by strong adoption of the FARAPULSE pulsed field ablation platform, expanded OPAL mapping utilization, and robust international demand, particularly in Europe.

Cardiovascular procedures also remained healthy, with WATCHMAN growing 19%. The interventional cardiology is benefiting from strong demand for AGENT DCB and imaging portfolio. However, procedural growth was partially offset by weakness in standalone WATCHMAN procedures due to hospital capacity constraints and softer Urology volumes, highlighting pockets of demand normalization despite innovation-led strength.

Medtronic’s MDT results in the fourth quarter of fiscal 2026 reflected broad-based procedural strength, led by exceptional performance in high-growth cardiovascular technologies. Cardiac Ablation Solutions grew 78% globally, with Pulsed Field Ablation procedures surging 145%, driven by rapid adoption of the Affera platform and Sphere-9 catheter. The expanding installed base, rising 40% sequentially in the United States, also aided growth.

Surgical procedures gained momentum as Hugo robotic-assisted surgery system volumes grew 2x–3x faster than the market, supported by rising utilization and expanding U.S. placements. Additional procedural tailwinds came from the Symplicity renal denervation platform, where weekly procedure volumes doubled, reinforcing Medtronic’s innovation-driven growth trajectory and supporting an increasingly favorable procedure growth outlook heading into fiscal 2027.

ISRG’s Price Performance, Valuation and Estimates

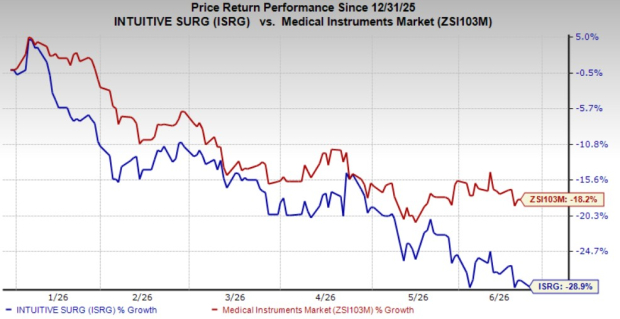

Shares of ISRG have lost 28.9% so far this year compared with an 18.2% decline of the industry.

Image Source: Zacks Investment Research

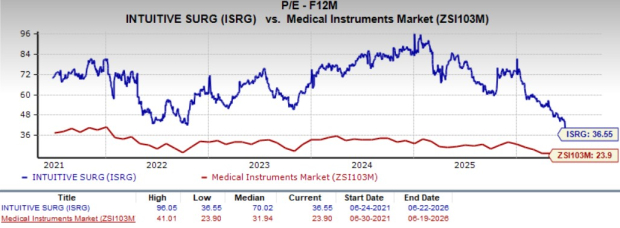

From a valuation standpoint, Intuitive Surgical trades at a forward price-to-earnings ratio of 36.55X, above the industry average. But, it is still lower than its five-year median of 70.02X. ISRG carries a Value Score of D.

Image Source: Zacks Investment Research

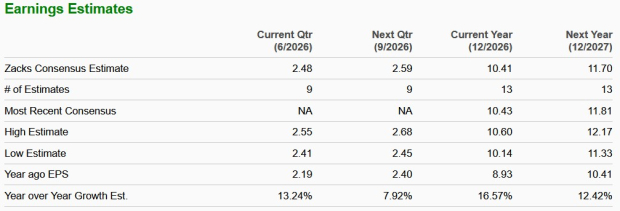

The Zacks Consensus Estimate for Intuitive Surgical’s 2026 earnings implies a 16.6% rise from the year-ago period’s level.

Image Source: Zacks Investment Research

The stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).