JD's Food Delivery Business Expands: Can Margins and Growth Align?

JD.com's JD food delivery segment represents a strategic expansion beyond traditional e-commerce, positioning the company to capture on-demand retail opportunities while deepening customer engagement. The business leverages JD's established supply chain infrastructure and premium user base to differentiate in a market dominated by established players. China's online food delivery market is projected to reach $181.43 billion by 2033, per Grand View Research. However, this growth backdrop masks intensifying competition and margin pressures that challenge newer entrants.

JD's approach centers on differentiation through supply chain innovation. The 7Fresh Kitchen model addresses persistent food safety concerns in China's restaurant industry, attempting to solve a fundamental trust issue that resonates with Chinese consumers increasingly focused on food quality and transparency. The integration with JD's retail ecosystem creates potential synergies, as food delivery users showed cohort conversion rates approaching 50%, indicating cross-platform engagement that could justify customer acquisition investments beyond standalone delivery economics.

The financial reality presents significant challenges. China's food delivery market operates on razor-thin margins, with profitability historically achieved only at massive scale. JD's New Businesses segment generated RMB15.6 billion in revenues during the third quarter, up 213.7% year over year, yet operating loss margins expanded from 12.4% to 100.9% as aggressive customer acquisition spending outpaced revenue growth. Marketing expenses surged 110.5% year over year, reflecting the high cost of market share expansion.

However, as JD continues to scale its food delivery business, the balance between rapid expansion and margin discipline remains uncertain. The Zacks Consensus Estimate for JD’s fourth-quarter revenues is pegged at $51.61 billion, indicating 8.57% year-over-year growth, against a backdrop of elevated investment intensity in food delivery. While the segment is expanding quickly, costs have so far risen in tandem, leaving open the question of whether efficiency gains and reduced subsidy intensity can meaningfully narrow losses over time. How this trade-off evolves will determine whether growth and margins can ultimately align.

JD Faces Intensifying Competition

JD faces intensifying competition from Alibaba BABA and GrabGRAB as all three scale food delivery under margin pressure. Alibaba runs food delivery within its local services ecosystem, using Ele.me to drive user frequency while managing subsidy intensity, with Alibaba prioritising ecosystem monetization over standalone profits. Grab treats food delivery as a core engagement layer in its super-app, with Grab’s focus on improving unit economics through higher order density. Compared with Alibaba and Grab, JD’s approach leans more heavily on supply-chain control, underscoring different paths toward balancing growth and margins.

JD.com's Price Performance, Valuation & Estimates

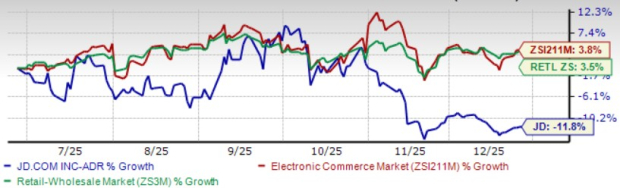

Shares of JD.com have declined 11.8% in the past six months, underperforming the Zacks Internet-Commerce industry and Zacks Retail-Wholesale sector’s return of 3.8% and 3.5%, respectively.

JD’s Six-Month Price Performance

Image Source: Zacks Investment Research

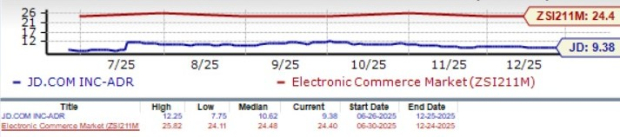

From a valuation standpoint, JD.com is trading at a forward 12-month price-to-earnings ratio of 9.38X, lower than the industry’s 24.4X. JD carries a Value Score of B.

JD’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for JD’s 2025 earnings is pegged at $2.82 per share, unchanged over the past 30 days. The earnings figure suggests a 33.8% decline year over year.

JD.com currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Naming Top 10 Stocks for 2026

Want to be tipped off early to our 10 top picks for the entirety of 2026? History suggests their performance could be sensational.

From 2012 (when our Director of Research Sheraz Mian assumed responsibility for the portfolio) through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Now Sheraz is combing through 4,400 companies to handpick the best 10 tickers to buy and hold in 2026. Don’t miss your chance to get in on these stocks when they’re released on January 5.

Be First to New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

JD.com, Inc. (JD): Free Stock Analysis Report

Alibaba Group Holding Limited (BABA): Free Stock Analysis Report

Grab Holdings Limited (GRAB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).