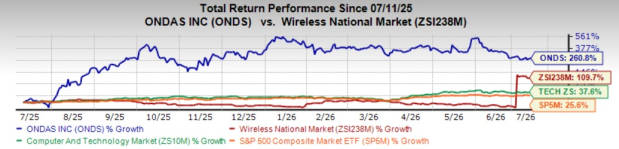

Ondas Stock Up 261% in a Year: Should Investors Buy, Hold or Sell?

Ondas Inc.'s ONDS shares have surged 260.8% a year, outperforming the Wireless National industry’s growth of 109.7%. The S&P 500 composite and the Zacks Computer and Technology sector are up 37.6% and 25.6%, respectively, in the same time frame.

Ondas has also outpaced its peers, Red Cat Holdings RCAT, Kratos Defense & Security Solutions KTOS and Draganfly DPRO. KTOS has lost 5.5%, over the same period, while RCAT and DPRO are up 7.2% and 21.6%, respectively.

Image Source: Zacks Investment Research

However, shares of Ondas have plunged 42% in the past six months.

Let us take a closer look at ONDS’ fundamentals, key growth drivers, competitive strengths and potential risks to determine whether the stock remains an attractive investment.

Key Factors to Consider

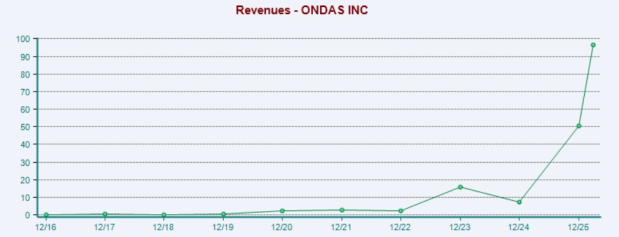

Ondas is benefiting from strong momentum across its defense, security and autonomous systems businesses as its Core + Strategic Growth strategy continues to gain traction. The company reported first-quarter 2026 revenue of more than $50.1 million, reflecting tenfold year-over-year growth and exceeding the high end of its prior target by more than 25%. Revenue for the quarter was nearly equal to the company's total revenue for full-year 2025, supported by strong demand for its Cyber-over-RF platform, Iron Drone interceptor systems and BIRD Aerosystems' airborne missile defense solutions. The company also achieved product company-level EBITDA profitability two quarters ahead of its internal plan. Ondas raised its full-year 2026 revenue forecast to at least $390 million (up from the earlier target of at least $375 million), implying roughly 670% year-over-year growth.

Image Source: Zacks Investment Research

The company is expanding its global operating platform through strategic acquisitions, partnerships and broader international reach. The acquisitions of World View and Mistral have strengthened its technology portfolio, customer relationships and operational capabilities, while its partnership with Palantir supports mission autonomy and multi-domain intelligence, surveillance and reconnaissance (ISR) solutions. The company also launched the ONBERG joint venture in Germany to strengthen its presence across European defense markets.

Ondas continues to strengthen its commercial position through expanding customer demand, backlog growth and program wins. Backlog increased to approximately $457 million following the World View and Mistral acquisitions, providing visibility into future revenue. Ondas highlighted growing demand across aerial security, ISR, unmanned ground vehicles and autonomous mission systems, supported by geographic expansion in the United States, Europe, the Middle East and Asia. The company also stated that it has a pipeline of approximately $4.3 billion across more than 45 active submissions and strategic programs with combined potential exceeding $1.6 billion.

Also, ONDS continues to enhance its technology portfolio by integrating autonomous platforms, AI capabilities and software solutions. The company introduced the IRON-WAVE multi-layered robotic platform, which combines aerial and ground systems with AI-assisted command and control for defense operations. Through its partnership with Palantir, Ondas is developing SkyWeaver, an AI-powered intelligence platform designed to integrate data across its autonomous systems and automate mission intelligence workflows. Management expects these capabilities to strengthen its software offerings, expand customer opportunities and support long-term growth across defense and security markets.

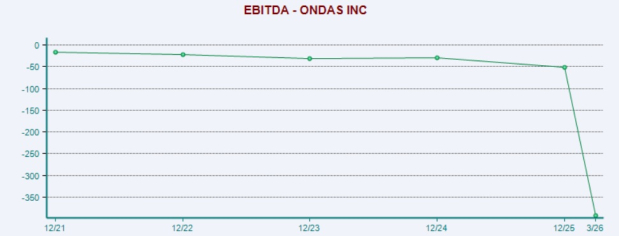

However, Ondas continues to increase operating expenses as it invests heavily in personnel, infrastructure, leadership expansion, operating capabilities and acquisitions to support future growth. Operating expenses rose to $67.3 million during the first quarter, and management expects operating expenses to continue increasing through the first half of 2026 as investments continue across the business. The company also expects higher cash usage in the near term due to acquisition-related spending and continued investment ahead of revenue growth.

The company stated that reported earnings will continue to experience volatility because of non-cash accounting items. The warrant liability is expected to create ongoing fluctuations in reported earnings, while quarterly profitability may also vary depending on product mix and investment priorities. Although product company profitability has been achieved ahead of schedule, management indicated that adjusted EBITDA at the broader Ondas Autonomous Systems level is now expected in the first quarter of 2027.

Image Source: Zacks Investment Research

Key Valuation Metric for ONDS

ONDS stock is trading at a substantial premium, with a forward 12-month price/sales of 7.1X compared with the industry’s 9.18X. In comparison, KTOS, RCAT and DPRO trade at multiples of 4.69X, 6.05X and 0.79X, respectively.

Image Source: Zacks Investment Research

What to Do With ONDS Stock Now?

Ondas is benefiting from strong execution across its defense and autonomous systems businesses, expanding global opportunities, a growing backlog, strategic acquisitions and AI-driven platform development, which bodes well for its long-term growth prospects. However, rising operating costs, continued EBITDA losses at the consolidated level and significant cash burn reflect near-term financial pressure.

Existing investors may consider holding their positions, while new investors could wait for a better entry point.

Currently, ONDS carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).