Buy NIO Stock Ahead of ES9 Debut at the Beijing Auto Show?

NIO Inc. NIO is heading into the 2026 Beijing Auto Show with products that could keep its momentum going. NIO will be showcasing 11 models and 12 full-stack technologies across its three brands—NIO, Onvo, and Firefly—all under one roof for the first time, per CnEVPost. So, should you buy the stock ahead of what looks like a major product cycle?

Well, we think so. NIO is entering one of its strongest launch phases yet, backed by real delivery growth, improving margins, and a clearer execution strategy. At around $7 a share, NIO looks quite a bargain. Let’s see how the fundamentals for the stock are improving.

NIO ES9 to Take Center Stage After ES8 Success

The spotlight at the auto show will be firmly on ES9, NIO’s new flagship SUV. This isn’t just another launch—it’s the company doubling down on the premium segment where it has already proven it can win.

The third-generation ES8 has been a breakout success. It hit 100,000 deliveries in just 215 days—setting a record in China’s premium vehicle segment above 400,000 yuan. That’s not easy, especially for a domestic automaker competing with global luxury brands. The ES8 alone contributed over 54% of total deliveries in the first quarter of 2026. Monthly deliveries crossed 10,000 units for five straight months.

The ES9 is expected to carry this momentum forward. It comes loaded with 43 industry-first technologies and has already opened for pre-sales at a starting price of 528,000 yuan. That price point matters. It signals confidence. NIO isn’t chasing volume at the low end—it’s pushing deeper into high-margin territory.

The ES9 may be the headline grabber, but NIO is entering an intensive launch cycle across brands and segments.

Alongside the ES9, the company is preparing to roll out Onvo L80, while the recently launched 2026 L90 already adds momentum to the sub-brand. At the same time, refreshed versions of ET5, ET5 Touring, ES6 and EC6 are hitting the market with upgraded features at unchanged prices.

NIO’s Delivery Growth Beating Rivals

NIO delivered 83,465 vehicles in the first quarter of 2026, representing a 98.3% increase year over year and exceeding its own guided range of 80,000-83,000 units. First-quarter deliveries consisted of 58,543 units from the NIO brand, 13,339 units from the ONVO brand and 11,583 from Firefly.

Meanwhile, growth at close peers XPeng XPEV and Li Auto LI was less impressive. XPeng’s first-quarter deliveries came in at 62,682 units, marking a decline from 94,008 units in the year-ago period. In contrast, Li Auto reported 95,142 deliveries, up modestly from 92,864 vehicles a year earlier.

Margins Are Finally Moving in the Right Direction

For a long time, the biggest concern around NIO wasn’t demand—it was profitability. That narrative is starting to shift.

Vehicle margins improved to 18.1% in the last quarter of 2025 from 13.1% in the corresponding period of 2024. The company is now targeting 20-25% margins for the NIO brand, above 15% for the Onvo brand and above 10% for Firefly.

Those are meaningful targets. And they look achievable if the current product cycle—especially high-end models like ES8 and ES9—continues to scale.

NIO has moved to a more decentralized operating model, improving cost discipline and return on investment. The company is no longer chasing growth at any cost—it’s aiming for balanced execution.

NIO’s Battery Swap Edge & Global Push

Its battery swap network remains one of its biggest competitive advantages. With more than 3,800 swap stations and more than 28,000 charging points, it offers a level of convenience that most EV players still can’t match. The Battery-as-a-Service model also lowers upfront costs for buyers—making premium EVs more accessible.

At the same time, NIO is expanding globally. It was present in 20 markets by the end of 2025 and aims to double that to 40 by the end of 2026.

NIO: Price, Valuation & Estimates

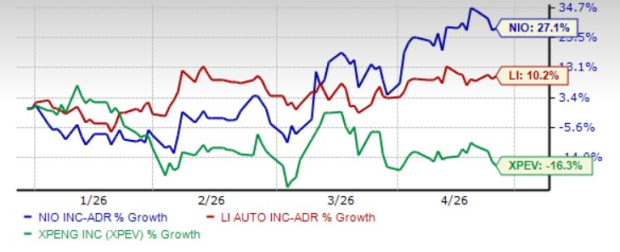

Year to date, shares of NIO have risen over 27%, outperforming Li Auto and XPeng.

YTD Price Performance Comparison

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

From a valuation perspective, NIO currently trades at a forward price-to-sales ratio of 0.76, below Li Auto and XPeng.

NIO Looks Undervalued Relative to LI & XPEV

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

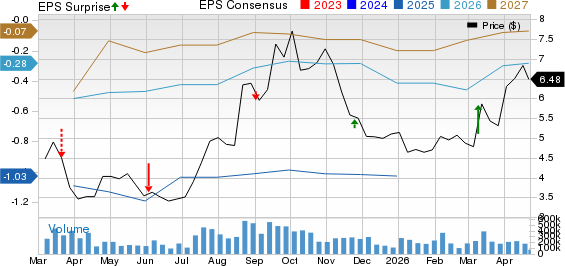

The Zacks Consensus Estimate for NIO’s 2026 and 2027 sales implies year-over-year growth of 50% and 19%, respectively. The consensus mark for the bottom line for the current and next year implies 71% and 76% improvement, respectively.

NIO Inc. Price, Consensus and EPS Surprise

NIO Inc. price-consensus-eps-surprise-chart | NIO Inc. Quote

Investor Takeaway

So, a lot of things are working in NIO’s favor now. Strong delivery growth, a proven premium model (ES8), a major upcoming launch (ES9), improving margins, a multi-brand strategy, battery swap technology and global expansion underway. Right now, the setup looks compelling. The ES9 debut could mark the next leg of growth.

NIO currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).