5 Large-Cap Fintech Stocks to Buy to Tap Huge Near-Term Upside

Financial technology (fintech) represents a transformative investment space in a hybrid sector merging finance and technology. The companies featured on the screen encompass a variety of services, like online banking, peer-to-peer payments, insurance, cryptocurrency and cybersecurity, among others.

The performance of the fintech space is inversely related to the movement of interest rates. A low-interest-rate regime will be beneficial for this space as a higher interest rate significantly affects technological improvement and product innovation of fintech companies.

Fintech's innovative nature positions it as a fascinating choice in the evolving financial landscape. With the expansion of mobile and broadband networks, fintech is poised for significant growth. The rise of artificial intelligence (AI) technologies and machine learning further revolutionizes banking, payments, and investments, offering efficient and secure financial solutions.

At this stage, we recommend investing in five financial technology bigwigs to tap into the digital finance revolution in 2026. These are: Interactive Brokers Group Inc.IBKR, Moody's Corp. MCO, LPL Financial Holdings Inc.LPLA, Paychex Inc.PAYX and Jack Henry & Associates Inc. JKHY.

These stocks have significant short-term price upside potential. Each of our picks currently carries either a Zacks Rank #1 (Strong Buy) or 2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

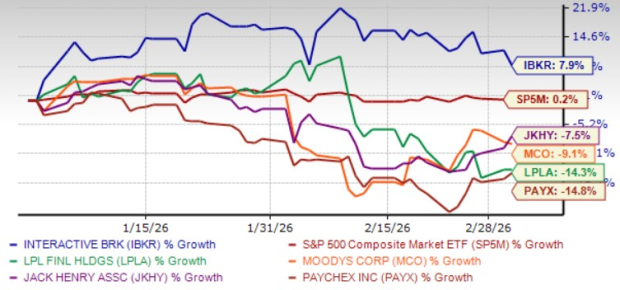

The chart below shows the price performance of our five picks year to date.

Image Source: Zacks Investment Research

Interactive Brokers Group Inc.

Zacks Rank #1 Interactive Brokers Group’s product suite expansion initiatives, along with efforts to broaden its emerging-market customer base and develop proprietary software, are expected to support top-line growth and improve its market share.

Lower compensation expenses as a percentage of net revenues remain a major positive catalyst, which provides IBKR a competitive edge. Furthermore, a solid liquidity position is likely to support continued capital distribution activities.

IBKR has been undertaking several product diversification efforts to expand the reach of its services. In February 2026, the company expanded its crypto futures offerings with the launch of Coinbase Derivatives, LLC.

In January 2026, the company announced that eligible clients can now fund their brokerage accounts using stablecoin, providing near-instant processing and 24/7 availability, enabling clients to deposit funds and begin trading across global markets within minutes of initiating a transfer.

Interactive Brokers Group has an expected revenue and earnings growth rate of 6.1% and 7.3%, respectively, for the current year. The Zacks Consensus Estimate for the current year’s earnings has improved 5.4% in the past 60 days.

The short-term average price target of brokerage firms for the stock represents an increase of 25.5% from the last closing price of $69.40. The brokerage target price is currently in the range of $75-$91. This indicates a maximum upside of 31.1% and a downside of 8.1%.

Moody's Corp.

Zacks Rank #2 Moody's dominant position in the credit rating industry, along with opportunistic acquisitions and restructuring efforts to diversify revenues and footprint, will support top-line expansion.

MCO has been meaningfully growing through strategic acquisitions, increasing scale and cross-selling opportunities across products and vertical markets. In August 2025, it announced plans to secure a majority equity ownership in Middle East Rating & Investors Service. In June 2025, MCO fully acquired ICR Chile, solidifying its presence in Latin America’s domestic credit markets.

A solid rebound in bond issuance volume is expected to drive MCO’s growth. A strong balance sheet position and earnings strength are likely to keep MCO’s capital distributions sustainable.

Moody's has an expected revenue and earnings growth rate of 7.7% and 11.7%, respectively, for the current year. The Zacks Consensus Estimate for the current year’s earnings has improved 1% in the past 30 days.

The short-term average price target of brokerage firms for the stock represents an increase of 18.6% from the last closing price of $464.30. The brokerage target price is currently in the range of $460-$660. This indicates a maximum upside of 42.1% and a downside of mere 0.9%.

LPL Financial Holdings Inc.

Zacks Rank #2 LPL Financial Holdings continues to benefit from efforts to increase its client base. Opportunistic acquisitions of Commonwealth Financial and Investment Center, combined with solid advisor productivity and recruiting efforts, are expected to bolster LPLA’s advisory revenues.

LPLA considers acquisitions a core part of its business expansion strategy. Given a strong balance sheet position, it has accomplished several opportunistic deals over the years. Additionally, a solid balance sheet and robust liquidity position will likely facilitate sustainable capital distribution activities, through which, LPLA will keep enhancing shareholder value.

LPL Financial Holdings has an expected revenue and earnings growth rate of 25.7% and 19%, respectively, for the current year. The Zacks Consensus Estimate for the current year’s earnings has improved 0.9% in the past 30 days.

The short-term average price target of brokerage firms for the stock represents an increase of 45.6% from the last closing price of $306.22. The brokerage target price is currently in the range of $378-$543. This indicates a maximum upside of 77.3% and no downside.

Paychex Inc.

Zacks Rank #2 Paychex gains from an expanding cloud computing market and rising client adoption of cloud computing solutions. PAYX has been able to retain 83% of clients across the past three years, beating industry standards and facilitating steady revenues. This, along with improving employee productivity, is resulting in solid cash flows and liquidity, in turn, facilitating consistent dividends.

Paychex’s rise in Revenues Per Employee (RPE) by 7% from 2021-2025 shows workforce efficiency and operational productivity. This points to the company's ability to optimize its talent utilization and adapt to challenges, indicating efficient management and resource allocation. The rising RPE is viewed by investors as a positive indicator of value creation and financial health.

It indicates that PAYX’s workforce is delivering higher output, boosting the potential for profitability, and reinforcing the company’s growth narrative, encouraging long-term investment in the stock.

Paychex has an expected revenue and earnings growth rate of 16.7% and 9.2%, respectively, for the current year (ending May 2026). The Zacks Consensus Estimate for the current year’s earnings has improved 0.3% in the past 60 days.

The short-term average price target of brokerage firms for the stock represents an increase of 26.5% from the last closing price of $95.56. The brokerage target price is currently in the range of $98-$150. This indicates a maximum upside of 57% and no downside.

Jack Henry & Associates Inc.

Zacks Rank #2 Jack Henry & Associates is benefiting from growing services, support and processing revenues. The rise in data processing and hosting fees is contributing well. Strength in its card processing solutions due to expanding transaction volumes is a plus.

Growing payment processing and digital revenues are major upsides for JKHY. Strong momentum across the Core, Payments, Complementary and Corporate segments is positively impacting JKHY’s top-line growth.

Solid demand for the company’s AI-powered fraud detection platform is acting as a tailwind. JKHY’s growing initiatives to incorporate AI into select client solutions are expected to boost its revenues in the near term.

Jack Henry & Associates has an expected revenue and earnings growth rate of 5.9% and 5.5%, respectively, for the current year (ending June 2026). The Zacks Consensus Estimate for the current year’s earnings has improved 0.6% in the past seven days.

The short-term average price target of brokerage firms for the stock represents an increase of 18.1% from the last closing price of $168.75. The brokerage target price is currently in the range of $158-$220. This indicates a maximum upside of 30.7% and a downside of 6.4%.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Paychex, Inc. (PAYX): Free Stock Analysis Report

Moody's Corporation (MCO): Free Stock Analysis Report

Interactive Brokers Group, Inc. (IBKR): Free Stock Analysis Report

Jack Henry & Associates, Inc. (JKHY): Free Stock Analysis Report

LPL Financial Holdings Inc. (LPLA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).