Altria or Philip Morris: Which Stock Looks Stronger in Today's Market?

For investors evaluating the tobacco sector, the decision often narrows to two industry leaders: Altria Group, Inc.MO and Philip Morris International Inc.PM. Although both companies derive significant revenues from tobacco, they operate in different geographic markets and are pursuing distinct strategies to adapt to a rapidly changing nicotine landscape.

Altria remains primarily focused on the U.S. market, leveraging the strength of its Marlboro franchise while expanding into smoke-free alternatives such as NJOY and oral nicotine products. Philip Morris, by contrast, generates the bulk of revenues internationally and has established itself as a global leader in reduced-risk products, anchored by the IQOS heated tobacco platform. For investors, the comparison extends beyond brand recognition; it hinges on fundamentals, growth trajectories and each company’s ability to execute transition toward a smoke-free future.

The Case for Altria Stock

Altria’s investment appeal is rooted in its exceptional cash-flow generation and shareholder returns, supported by the enduring strength of the U.S. tobacco franchise. In 2025, the company delivered steady earnings growth, with adjusted earnings per share rising 4.4%, while returning approximately $8 billion to its shareholders through dividends and share repurchases. This combination of pricing power, disciplined cost management and capital allocation continues to underpin Altria’s status as one of the most reliable income stocks in the consumer sector.

Despite ongoing secular volume declines in cigarettes, Altria continues to demonstrate pricing power and operational discipline. The smokeable products segment generated more than $11 billion in adjusted operating income for the full year, with margins expanding to 63.4%, supported by robust net price realization. This ability to offset volume pressure through pricing and cost management remains a critical pillar of Altria’s earnings stability and dividend sustainability.

At the same time, Altria is advancing its smoke-free strategy, particularly in oral nicotine. The on! brand continues to scale, with shipment volumes rising 10.9% in 2025, while the FDA authorization and planned national rollout of on! PLUS positions the company to participate more meaningfully in the fast-growing nicotine pouch category. Management also highlighted progress in product development, regulatory submissions and international modern oral expansion, signaling a long-term effort to diversify beyond combustibles.

However, Altria’s transition remains challenging amid structural and regulatory headwinds. Domestic cigarette volumes declined about 9.5% in 2025, underscoring persistent secular pressure on the combustible business. As a result, Altria’s long-term investment outlook increasingly depends on whether oral nicotine and other smoke-free products can scale fast enough to offset ongoing volume declines.

The Case for Philip Morris Stock

Philip Morris’ investment appeal is increasingly defined by its accelerating shift toward smoke-free products, a transformation that continues to reshape both revenue mix and earnings quality. In the third quarter of 2025, smoke-free products accounted for 41% of total net revenues and 42% of gross profit. Shipments rose 16.6% year over year, driven by strong momentum in IQOS, ZYN and VEEV. This growth translated into record quarterly smoke-free gross profit of $3.1 billion, underscoring the company’s progress toward a more sustainable long-term profit model.

The company’s flagship smoke-free brands, IQOS, ZYN and VEEV, continue to deliver broad-based gains across key geographies. IQOS remains the global leader in heated tobacco, while ZYN is rapidly scaling both in the United States and internationally. VEEV is also gaining traction, strengthening Philip Morris’ presence in the closed-pod e-vapor category and diversifying its smoke-free portfolio.

Operational discipline remains a key differentiator. Ongoing productivity initiatives and cost controls have supported margin expansion and solid earnings growth, alongside resilient performance in the combustible segment. Management’s focus on efficiency and its multi-year cost-savings program provides additional support to cash flows and earnings visibility.

That said, structural headwinds persist in the combustible business. Cigarette shipment volumes declined 3.2% in the third quarter, reflecting long-term secular declines in consumption. While pricing has partially offset volume erosion, this lever is increasingly constrained by regulatory pressure and consumer affordability. As Philip Morris becomes more reliant on smoke-free products, any slowdown in the adoption of IQOS, ZYN or VEEV, whether due to regulatory delays, competitive intensity or shifting consumer preferences, could materially weaken its ability to offset combustible volume declines, elevating execution and transition risk.

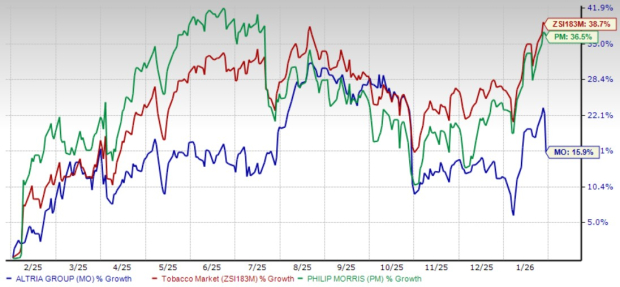

MO & PM: A Look at Past-Year Stock Performance

Over the past year, Altria’s shares have gained 15.9%, significantly underperforming Philip Morris, which surged 36.5%, and the industry’s growth of 38.7%. Currently, MO trades at $59.76, about 12.9% below its 52-week high. PM, at $177.89, sits roughly 4.7% below its peak.

Image Source: Zacks Investment Research

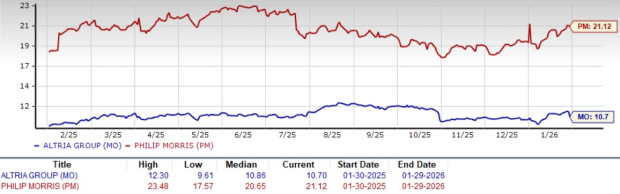

MO vs. PM: A Peek Into Stock Valuation

Altria is trading at a forward 12-month price-to-earnings (P/E) ratio of 10.7, just a tad below its one-year median of 10.86. Meanwhile, Philip Morris’ forward P/E ratio stands at 21.12, above its median of 20.65.

Image Source: Zacks Investment Research

MO vs. PM: Which Stock Looks More Promising Now?

Among the leading tobacco companies, Philip Morris appears to be the better bet right now. While Altria stands out for the stability and dependable income, its growth path is more limited by heavy exposure to the U.S. cigarette market and a slower shift away from traditional products. Philip Morris, on the other hand, is further along in reshaping business, with a diversified international footprint and a well-established portfolio of reduced-risk products that are increasingly central to its strategy.

PM’s execution, operational discipline and clearer pathway toward a smoke-free future give it a stronger long-term growth profile. This makes PM the more compelling choice for investors seeking both transformation and resilience in the evolving tobacco landscape.

Both MO and PM currently carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Altria Group, Inc. (MO): Free Stock Analysis Report

Philip Morris International Inc. (PM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).