MRVL to Post Q4 Earnings: Should You Buy, Sell or Hold the Stock?

Marvell Technology, Inc.MRVL is scheduled to report fourth-quarter fiscal 2026 results after market close on March 5, 2026.

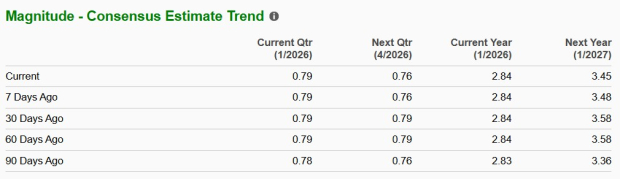

MRVL anticipates revenues to be $2.20 billion (+/- 5%) for fourth-quarter fiscal 2026. The Zacks Consensus Estimate for MRVL’s fiscal fourth-quarter revenues is pegged at $2.20 billion, indicating year-over-year growth of 21%.

For the fiscal fourth quarter, the company expects non-GAAP earnings of 79 cents (+/- $0.05) per share. The Zacks Consensus Estimate for MRVL’s fiscal fourth-quarter earnings is pegged at 79 cents per share, implying a 31.7% increase year over year. The consensus mark for earnings has remained unchanged over the past 60 days.

Image Source: Zacks Investment Research

In the trailing four quarters, Marvell Technology’s earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters, while missing the same on one occasion, with an average surprise of 1.17%.

Marvell Technology, Inc. Price and EPS Surprise

Marvell Technology, Inc. price-eps-surprise | Marvell Technology, Inc. Quote

What Our Model Says About MRVL

Our proven model does not conclusively predict an earnings beat for MRVL this season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. However, that’s not the case here. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

MRVL has an Earnings ESP of -1.81% and carries a Zacks Rank #4 (Sell) at present. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Factors Likely to Influence MRVL’s Q4 Results

MRVL’s custom business is tied to a limited number of large hyperscaler clients, creating customer concentration and revenue lumpiness risk. MRVL’s Celestial AI acquisition carries execution and commercialization risk before meaningful revenue contribution. Marvell Technology faces stiff competitive pressure from other semiconductor players. This remains an overhang on MRVL’s performance in the to-be-reported quarter.

Marvell Technology competes with Astera LabsALAB, Broadcom AVGO and Credo TechnologyCRDO in the connectivity market. Credo has a wide portfolio of AEC, SerDes IP, Retimer ICs and system design. Credo’s business is mainly driven by its strong AEC business, which posted double-digit sequential growth last quarter. Stiff competition is likely to affect MRVL’s fourth-quarter fiscal 2026 results.

Credo’s hyperscaler customer base is expanding, while it is also experiencing robust growth in optical DSP and LRO solutions, along with rising PCIe and Ethernet retimer adoption. Broadcom has a stronghold in carrier Ethernet and transport markets and is a major player in telecom optical interconnects and routing silicon space.

Astera Labs’ Leo CXL smart memory controllers are built for memory expansion up to two terabytes and improve interoperability to accelerate AI performance and cloud computing. However, not everything is gloom and doom for MRVL. MRVL’s outlook is supported by powerful tailwinds like the accelerating build-out of AI data center infrastructure. These factors are likely to have driven MRVL’s top line in the to-be-reported quarter.

The company delivered double-digit year-over-year growth in its data center segment in the previous quarter, reflecting strong hyperscaler demand for high-speed interconnect, custom silicon and switching solutions. MRVL's top line is likely to have been aided by rising cloud capital expenditure forecasts, expanding adoption of 1.6T optical products and a growing pipeline of XPU-attach.

MRVL Stock Price Performance & Valuation

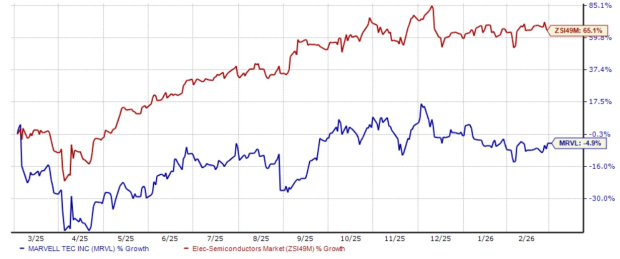

In the past year, Marvell Technology shares have lost 4.9%, underperforming the Zacks Electronics – Semiconductors industry’s growth of 65.1%.

MRVL One Year Performance Chart

Image Source: Zacks Investment Research

Now, let’s look at the value Marvell Technology offers investors at the current levels. Due to the recent fall, MRVL stock trades at a discounted price with a forward 12-month price-to-sales (P/S) multiple of 6.96X compared with the industry’s 8.09X.

MRVL Forward 12-Month (P/S) Valuation Chart

Image Source: Zacks Investment Research

Investment Thesis for MRVL Stock

MRVL is transforming itself into a key contributor to the connectivity hardware solutions for AI infrastructure and data centers. The company has launched the Golden Cable initiative to accelerate and expand thw Active Electrical Cable (AEC) ecosystem for faster deployment of AI infrastructure by cloud and hyperscaler customers.

AECs are crucial for short-reach, high-density connections inside and between racks. This technology supports next-generation 1.6 T connectivity for superfast networks. Now, MRVL’s partners will be able to validate cable architectures, advanced firmware, calibration data, and get support for integration and interoperability through the Golden Cable initiative.

MRVL is also gaining from the adoption of scale-up switches that connect AI accelerators within and across racks, requiring multi-terabit bandwidth and ultra-low latency. These switches will support both open standard Ethernet and UALink fabrics, leveraging Marvell Technology’s low-latency SerDes and Ethernet switch IP.

Macroeconomic and geopolitical uncertainties remain a meaningful overhang on Marvell Technology’s near-term performance. Evolving U.S. chip export restrictions and tariffs create operational and demand-side risks, particularly given Marvell Technology’s reliance on hyperscalers and global supply chains.

MRVL’s outlook for the fourth quarter of fiscal 2026 signals softer near-term growth. The company guided revenues of $2.2 billion (+/- 5%), indicating just 21% year-over-year growth, a slowdown compared to recent quarters.

Conclusion: Sell MRVL Stock

Customer concentration, rising competition, execution risks and softer near-term guidance overshadow MRVL’s AI tailwinds. Despite attractive valuation and data center momentum, risk-reward appears unfavorable ahead of the upcoming quarter.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Marvell Technology, Inc. (MRVL): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

Credo Technology Group Holding Ltd. (CRDO): Free Stock Analysis Report

Astera Labs, Inc. (ALAB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).