Is Bank of America Stock's Low Valuation a Bargain or a Warning Sign?

The Bank of AmericaBAC stock appears attractively valued, based on its price-to-sales (P/S) ratio, a metric often favored by value investors because sales figures are generally less prone to accounting adjustments than earnings.

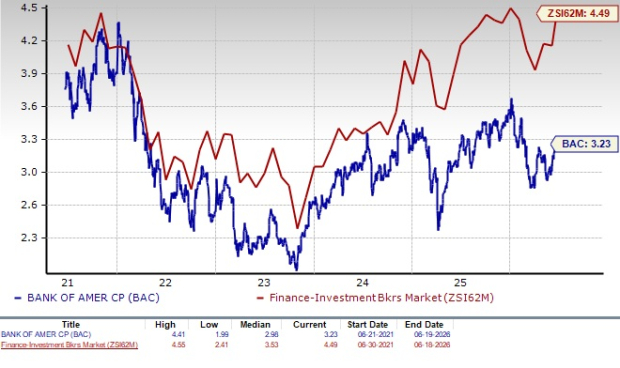

BAC is currently trading at a forward 12-month P/S ratio of 3.23X, which is below the industry average of 4.49X. The stock's current multiple is also lower than the upper end of its five-year historical range, indicating that shares may be trading at a discount to their historical valuation levels.

P/S (F12M)

Image Source: Zacks Investment Research

Compared with close peers like JPMorgan JPM and Morgan StanleyMS also, BAC looks inexpensive.

JPMorgan trades at a forward 12-month P/S ratio of 4.39X, while Morgan Stanley commands a multiple of 4.47X. This valuation gap suggests that investors are assigning a lower sales multiple to Bank of America despite its established franchise and earnings-generating capabilities.

The discounted valuation could offer an attractive opportunity for investors if the market eventually reassesses BAC's prospects and values the stock more in line with its peers and historical averages.

That said, valuation is only one part of the investment thesis, and investors should evaluate the company's fundamentals and growth prospects before making an investment decision.

Key Factors Supporting Bank of America

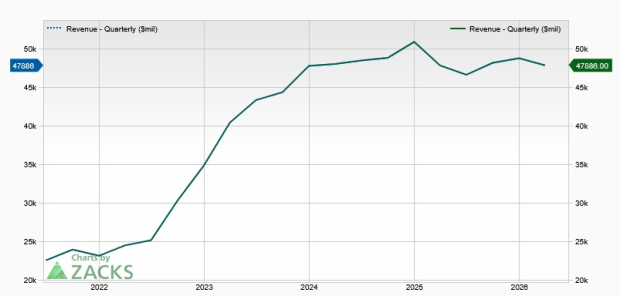

Robust Top-Line Growth: Bank of America has been witnessing an increase in revenues over the past several years. Total net revenues witnessed a compound annual growth rate (CAGR) of 5.7% over the last five years (2020-2025), with the uptrend continuing in the first quarter of 2026.

Revenue Trend

Image Source: Zacks Investment Research

The rise has been driven by consistent loan growth (net loans and leases saw a CAGR of 5.2% over the same time frame) and a favorable interest rate backdrop, along with a decent rise in fee income (total non-interest income witnessed a CAGR of 4.7%).

Despite declines in interest rates in 2024 and 2025, the company’s net interest income (NII) saw a CAGR of 6.7% in the five years ended 2025, primarily supported by increasing loan balances. The uptrend for NII continued in the first three months of 2026.

On the expectation of a continued rise in loan balances, along with stabilizing funding costs and fixed-rate asset repricing, BAC’s NII is expected to continue to improve in the near term. This, coupled with fee income growth, will likely keep supporting revenue growth.

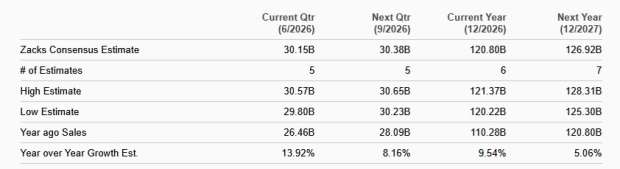

The Zacks Consensus Estimate for BAC’s 2026 and 2027 revenues is pegged at $120.80 billion and $126.92 billion, which indicates year-over-year growth rates of 9.5% and 5.1%, respectively.

Revenue Growth Estimates

Image Source: Zacks Investment Research

Solid Investment Banking (IB) Business: BAC’s IB business performance has been impressive of late. When global deal-making came to a grinding halt at the beginning of 2022, it weighed heavily on Bank of America’s IB business. The company’s total IB fees (in the Global Banking division) declined 45.7% in 2022 and 2.4% in 2023.

However, the trend reversed thereafter. In 2024, the company’s IB fees rose 31.4% year over year. Then again, in 2025, IB fees increased 8.4%.

In the first quarter of 2026, IB fees increased 23.6% year over year. While equity underwriting income increased 31.3%, debt underwriting income rose 2.7%. Advisory revenues grew 46.6%.

Since the market for global mergers and acquisitions has been improving, Bank of America is expected to continue witnessing solid growth in IB fees in the near term, supported by a healthy IB pipeline.

Integration of Artificial Intelligence (AI) With Branch Expansion: Bank of America is integrating AI with its branch expansion strategy by building a “phygital” banking model that combines AI-driven digital capabilities with modern, tech-enabled financial centers. While the bank plans to open more than 150 new centers by 2027, AI tools like Erica, fraud-detection systems and automated workflows are increasingly handling routine transactions and customer interactions.

This allows branch employees to focus on higher-value advisory services and cross-selling products such as mortgages, auto loans and credit cards. The strategy is expected to improve operating efficiency, lower costs, enhance customer engagement, and drive stronger fee income and NII growth over the long term, ultimately supporting sustained operating margin expansion.

Strong Balance Sheet & Liquidity Position: As of March 31, 2026, Bank of America had total debt worth $736.6 billion. Its cash and cash-equivalents balance was $242.5 billion. Despite a high debt burden, the company’s liquidity position seems sufficient to meet near-term obligations since BAC has easy access to the debt markets, given its investment-grade long-term credit ratings of A1, A- and AA- from Moody’s, S&P Global Ratings and Fitch Ratings, respectively, along with a stable outlook.

The company has an efficient capital distribution plan, supported by its earnings strength, through which it keeps enhancing shareholder value. After clearing the 2025 stress test, Bank of America raised its quarterly dividend 7.7% to 28 cents per share. Prior to this, it increased its dividend 8.3% in 2024, 9.1% in 2023, 4.8% in 2022 and 17% in 2021.

Also, BAC engages in regular share repurchases. In July 2025, it authorized a $40-billion repurchase program. As of March 31, 2026, $22.9 billion worth of authorization remained available for repurchase.

Analyzing Bank of America’s Price Performance

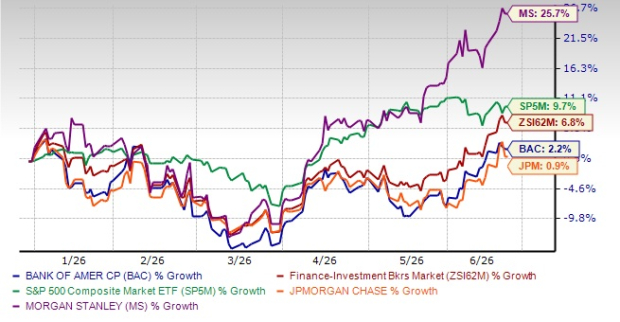

Despite the impressive first-quarter 2026 results, supported primarily by loan growth, along with trading and IB strength, BAC shares have gained 2.2% so far this year.

Year to date, the S&P 500 Index has rallied 9.7%, and the industry to which the BAC stock belongs has risen 6.8%.

If we look at JPMorgan and Morgan Stanley’s performance, it appears that BAC has underperformed MS but outperformed JPM. Shares of JPMorgan have gained 0.9% so far this year, whereas the Morgan Stanley stock has appreciated 25.7%.

YTD Price Performance

Image Source: Zacks Investment Research

How to Approach Bank of America Stock?

Driven by scalable AI capabilities, a data advantage from its vast customer base and a well-executed strategy that blends digital efficiency with targeted branch expansion, BAC has a strong fundamental positioning. With continued investments in technology and a disciplined expansion approach, the company will likely deliver steady margin expansion and long-term value creation.

In addition to this, the bank continues to benefit from a large, low-cost deposit franchise and improving NII, all of which are expected to support steady profitability.

However, the company’s total non-interest expenses have increased, seeing a six-year (2019-2025) CAGR of 4.1%, with the uptrend expected to continue in the near term. Elevated costs will likely hurt the bottom line to an extent.

Moreover, analysts have a mixed stance regarding BAC’s earnings growth potential. Over the past 30 days, the Zacks Consensus Estimate for the company’s 2026 earnings has been revised lower. Its 2027 earnings estimate has been revised only marginally higher.

Earnings Estimate Revision

Image Source: Zacks Investment Research

Thus, despite a favorable valuation and solid revenue growth prospects, it does not seem wise to invest in Bank of America immediately because its profitability might be hampered by elevated costs. Analysts also do not seem very optimistic regarding the company’s earnings growth prospects.

Yet, those who already own the BAC stock in their portfolio should hold on to it because the company is less likely to disappoint in the long run.

At present, Bank of America carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).