Microsoft vs. Alibaba: Which Cloud Titan Is the Smarter Buy Right Now?

MicrosoftMSFT and Alibaba BABA lead Western and Chinese cloud-AI markets, respectively, both pouring capital into generative models, agentic platforms and custom silicon. With upcoming quarterly results and major recent AI announcements from both, this comparison is timely.

Let’s delve deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

The Case for MSFT Stock

Microsoft's AI-driven cloud franchise continues scaling at a remarkable pace. In second-quarter fiscal 2026, Microsoft Cloud surpassed $50 billion in quarterly revenues for the first time, up 26% year over year, while Azure and other cloud services grew 39% (up 38% in constant currency). Total revenues climbed 17% to $81.3 billion, with operating margin expanding to 47%. Commercial remaining performance obligations reached $625 billion, up 110% year over year, signaling robust multi-year demand visibility.

Microsoft's full-stack AI platform is a key differentiator. In January 2026, the company brought its Maia 200 accelerator online, delivering 30%+ improved total cost of ownership, and supports the broadest model catalog of any hyperscaler, including GPT-5.2, Claude 4.5, Mistral, and first-party models. Paid Microsoft 365 Copilot seats hit 15 million, up more than 160%, while GitHub Copilot subscribers surpassed 4.7 million.

Recent announcements reinforce momentum. Microsoft rolled out Agent 365 as an agent control plane extending governance across clouds, introduced Copilot Tuning templates for enterprises, and scheduled Microsoft 365 E7 for general availability on May 1, 2026. Commercial pricing updates effective July 1, 2026, should provide additional revenue uplift.

For third-quarter fiscal 2026, management guided Azure growth of 37-38% in constant currency and expects fiscal 2026 operating margins to be up slightly versus prior commentary. Capex intensity and GPU-supply constraints create near-term gross-margin pressure. However, Microsoft's sold-through RPO, deep enterprise moat and diversified revenue base across Azure, Microsoft 365 Copilot, GitHub Copilot, Dragon Copilot and Security Copilot position it to extract durable long-term returns.

The Zacks Consensus Estimate for MSFT’s fiscal 2026 earnings is pegged at $17.10 per share. The estimate indicates 25.37% year-over-year growth.

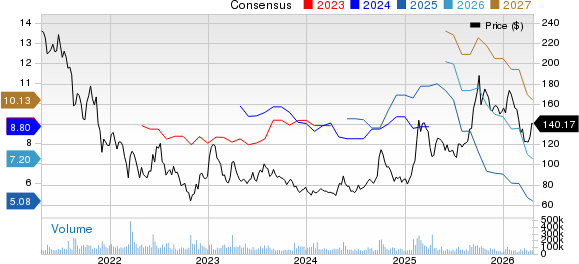

Microsoft Corporation Price and Consensus

Microsoft Corporation price-consensus-chart | Microsoft Corporation Quote

The Case for BABA Stock

Alibaba's cloud and AI story is compelling on paper, but increasingly strained in execution. In fiscal third-quarter 2026, Alibaba's total revenues rose just 2% to RMB 284.8 billion ($40.7 billion), missing expectations, while GAAP net income plunged 66%. Adjusted EBITA declined 57% and free cash flow fell sharply, down RMB 27.7 billion year over year, reflecting aggressive spending on AI infrastructure and its loss-making quick-commerce push.

The bright spot remains Cloud Intelligence Group, which grew 36% with AI-related revenues posting triple-digit growth for the 10th consecutive quarter. Management unveiled an ambitious five-year goal to surpass $100 billion in combined external cloud and AI revenues. However, these gains are being eroded by heavy capital expenditure and intense domestic competition in China's AI market, which is pressuring pricing discipline and the overall margin structure.

Recent March-April 2026 announcements reflect strategic reshuffling rather than clear wins. Alibaba established the Alibaba Token Hub business group on March 16, 2026, launched the Wukong enterprise AI agent platform on March 17, 2026, and released Qwen 3.6-Plus on April 2, 2026. While these position Qwen competitively, the sweeping AI team reorganization highlights ongoing execution uncertainty and internal realignment risks for investors to monitor closely.

Broader risks weigh heavily. BABA faces persistent U.S.-China trade tensions, regulatory overhang, and softer Chinese consumer demand, pressuring its core e-commerce base. Management guidance explicitly warns that adjusted EBITA will continue to fluctuate quarter over quarter due to competition and investment intensity. Profitability is not expected to normalize for several years, making near-term upside uncertain for investors.

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $5.08 per share, implying a 43.62% year-over-year decline.

Alibaba Group Holding Limited Price and Consensus

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

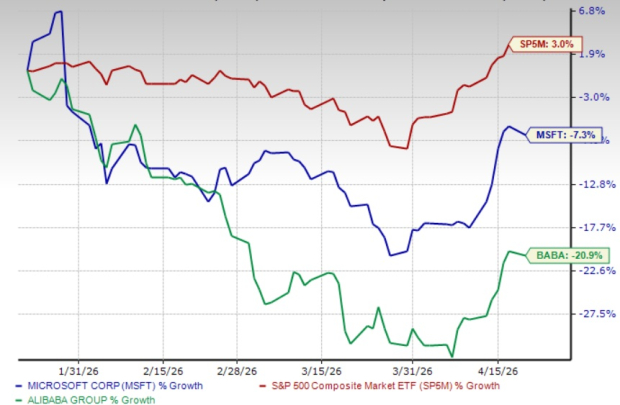

Valuation and Price Performance Comparison

MSFT shares have lost 7.3% in the past three-month period. In sharp contrast, BABA shares have tumbled 20.9% in the same time frame, reflecting deteriorating investor sentiment amid profit pressure, competitive intensity and regulatory overhang.

MSFT Outperforms BABA in 6-Month Period

Image Source: Zacks Investment Research

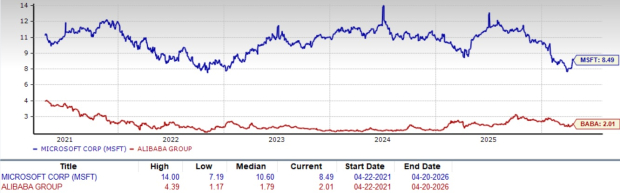

Both Microsoft and Alibaba shares are currently overvalued, as suggested by a Value Score of D. Microsoft trades at an 8.49x forward price-to-sales multiple compared with BABA’s 2.01x multiple. However, Microsoft's premium valuation is clearly justified. Its accelerating Azure growth, expanding operating margins, $625 billion commercial RPO backlog, rising Microsoft 365 Copilot seats and strong free cash flow generation support the higher multiple. Alibaba's premium, by contrast, looks stretched given its plunging profits, negative free cash flow, loss-making quick-commerce investments and uncertain near-term monetization trajectory. Microsoft offers superior earnings quality and visibility, making its valuation defensible while BABA's premium appears increasingly difficult to sustain

MSFT vs. BABA: P/S F12M Ratio

Image Source: Zacks Investment Research

Conclusion

Microsoft's edge over Alibaba is multidimensional. Microsoft delivers accelerating cloud growth (Azure up 39%), expanding operating margins, a $625 billion RPO backlog and industry-leading agentic AI adoption through Copilot, Agent 365 and Maia 200 silicon. Its enterprise customer base, diversified revenue streams and shareholder-friendly capital returns stand in contrast to Alibaba's declining profits, sharply lower free cash flow, AI team reorganization, regulatory overhang and U.S.-China friction. While both trade at premium valuations, Microsoft is supported by superior fundamentals and clearer guidance. Given these factors, Microsoft has better upside potential; investors should buy MSFT stock and stay away from BABA stock for now. MSFT currently carries a Zacks Rank #2 (Buy), whereas BABA has a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).