META's $9B AI Infrastructure Bet, Cloud Ambitions: Is the Stock a Buy?

Meta PlatformsMETA has built one of the world's most profitable digital advertising businesses. Nearly 98% of its revenues still comes from ads, while artificial intelligence (AI) has helped improve content recommendations, advertising performance and user engagement across its apps.

But the company is thinking beyond advertising and is laying the groundwork for its next phase of growth. In the latest infrastructure push, Meta is building its first data center outside the United States—a 1-gigawatt facility in Alberta, Canada, expected to cost about $9 billion. That would be the company’s 33rd data center. Separately, reports indicate Meta is exploring a cloud computing business by potentially renting excess computing capacity or offering AI services to outside customers.

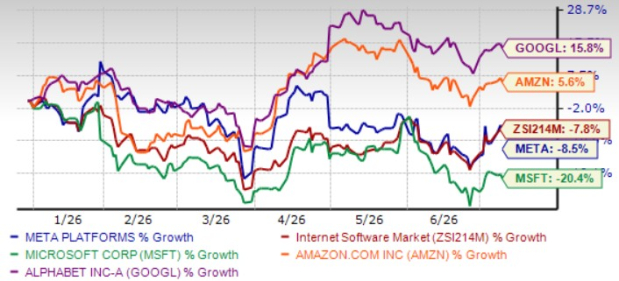

Over the past year, META stock has underperformed the broader industry and peers like AmazonAMZN and AlphabetGOOGL but has surpassed MicrosoftMSFT.

1-Year Price Performance Comparison

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Do Meta's aggressive AI infrastructure investments and potential cloud plans strengthen its long-term investment case? And is META stock a buy at current levels?

The AI Infrastructure Build-Out Continues

Meta's Alberta facility is the latest step in the company's AI infrastructure expansion. As AI models become larger and more compute-intensive, Meta is rapidly adding data center capacity to support growing demand for AI infrastructure and services.

Alberta offers several advantages for such a project, including abundant energy, industrial land and a business-friendly regulatory environment. The data center is also expected to create more than 3,000 construction jobs at its peak, while supporting local infrastructure and community investments.

Meta is building this infrastructure to train and deploy its Llama AI models and power AI experiences across Facebook, Instagram, WhatsApp, Messenger and Threads.

Meta is not alone. Amazon, Microsoft and Alphabet are also investing on a huge scale in AI infrastructure and data centers to meet surging demand for generative AI.

Could Meta Become the Next Cloud Provider?

Alongside its infrastructure expansion, Meta is reportedly evaluating another opportunity—cloud computing.

Per Bloomberg reports, the company is debating whether to offer customers access to AI models hosted on its infrastructure or simply rent out excess computing capacity. If launched, the business would compete with Amazon Web Services, Microsoft Azure and Google Cloud, which have become major revenue contributors for Amazon, Microsoft and Alphabet, respectively.

For investors, the significance lies in diversification. Meta has invested significantly in AI infrastructure over the past several years. A cloud business could provide another way to generate returns from those investments while reducing the company's overwhelming dependence on advertising.

However, cloud computing also comes with challenges. Unlike advertising, cloud infrastructure is a lower-margin business that requires significant investments in servers, networking, enterprise sales and customer support. Alphabet offers a useful example. While Google's advertising business enjoys operating margins above 40%, Google Cloud took years to become profitable and still operates at much lower margins. If Meta eventually enters the cloud market, investors should expect greater revenue diversification, but potentially lower overall profitability.

AI Is Already Strengthening Meta’s Core Business

Meta is already benefiting from its AI investments. Instagram Reels watch time increased 10% globally during the first quarter of 2026, while Facebook video watch time rose 8%. AI-translated videos are now watched weekly by more than 500 million users across Facebook and Instagram. Threads also surpassed 500 million monthly active users.

Meta's ecosystem remains one of its biggest competitive advantages. More than 3.56 billion people use at least one of its apps every day, giving the company enormous amounts of data to improve AI models and deliver better advertising results.

The company is also expanding monetization opportunities through paid messaging on WhatsApp, subscription offerings across Facebook, Instagram and Meta AI, and new AI tools such as Muse Image.

Meta’s Elevated Spending Remains a Concern

While Meta is seeing tangible benefits from AI, the cost of building that advantage remains a key concern. Its aggressive AI spending has raised investor concerns, as the financial returns from these massive investments are likely to take time to materialize.

Meta now expects 2026 capital expenditures between $125 billion and $145 billion, above its previous guidance, while operating expenses are projected between $162 billion and $169 billion. This is expected to put pressure on free cash flow and near-term earnings.

Meta is not alone in this spending race. Alphabet raised its 2026 capital expenditure outlook to $180-$190 billion, reflecting higher AI compute demand and additional investments tied to the Wiz acquisition. Microsoft expects to invest roughly $190 billion during fiscal 2026, while Amazon plans to spend around $200 billion and continues investing aggressively to expand AWS and its AI infrastructure.

META Valuation Check

META stock is trading at a premium valuation. Its forward 12-month P/S of 5.45X is above the Zacks Internet Software industry's 3.89X. The stock also carries a Value Score of C.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

How to Play META Stock Now

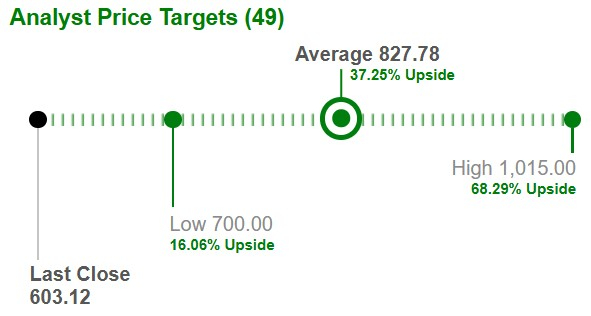

Meta is making the right long-term strategic bets, but investors may have to wait longer for those investments to deliver meaningful financial returns. The stock has a rich valuation, and heavy AI spending is likely to weigh on free cash flow and earnings over the near term. Although Wall Street's consensus price target implies roughly 37% upside from current levels, that potential is accompanied by significant execution risk.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Existing shareholders can continue to hold the stock for its long-term AI potential, but new investors may be better off waiting for a more attractive entry point. META currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).