3 Reasons Why You Should Hold Oracle Stock Despite a 29.5% YTD Drop

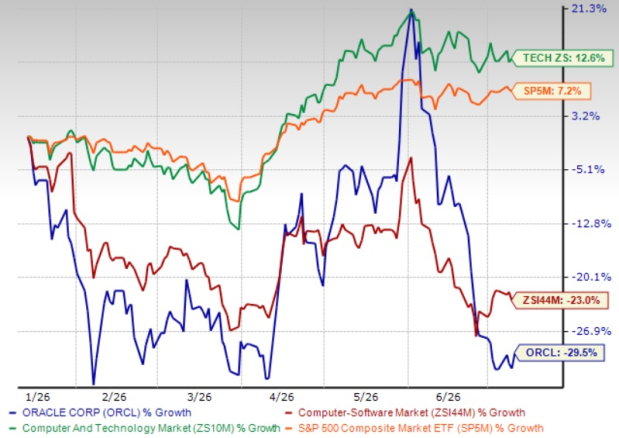

Shares of OracleORCL have tumbled roughly 29.5% year to date, underperforming the Zacks Computer and Technology sector’s appreciation of 12.6%. This has rattled investors who once viewed the enterprise database giant as a steady compounder, now reinvented as a major artificial intelligence (AI) infrastructure powerhouse.

Oracle shares have swung sharply in 2026, falling from a 52-week high to lows in the mid-$130s before stabilizing in the $140s range. The sell-off reflects mounting anxiety over the capital Oracle must deploy to build its cloud data centers and the debt load required to fund that expansion.

Yet beneath the volatility, Oracle's fourth-quarter and full-year fiscal 2026 results revealed record demand, an enormous contracted backlog and guidance pointing to accelerating growth in fiscal 2027. The board also declared a quarterly cash dividend of 50 cents per share, payable July 24, 2026, a signal of confidence in underlying cash generation even amid heavy AI-related spending.

For investors already holding the stock, several company-disclosed fundamentals argue for patience rather than capitulation, even as real risks keep the near-term outlook clouded.

Oracle Underperforms Industry, Sector YTD

Image Source: Zacks Investment Research

Record Backlog Signals Durable Demand

The clearest reason to stay invested is Oracle's Remaining Performance Obligations, which swelled to $638 billion at the close of the fourth quarter, up from $553 billion just one quarter earlier and up 363% from a year ago. Management has said most of this increase stems from large-scale AI contracts, many of which involve customers prepaying Oracle or supplying their own graphics processing units, a structure that helps offset the capital Oracle itself must raise. Total cloud revenues for the quarter reached $9.9 billion, up 47% in U.S. dollars, with Cloud Infrastructure revenues surging 93% to $5.8 billion and Cloud Applications revenues rising 10% to $4.1 billion. A backlog this size, built around committed AI spending, indicates demand for Oracle's cloud capacity is contractually secured, providing revenue visibility beyond the current fiscal year.

Guidance Points to Accelerating Growth

Oracle's own forward-looking commentary offers a second reason for continued conviction. For the first quarter of fiscal 2027, the company guided total revenue growth of 27% to 29% and total cloud revenue growth between 57% and 63% in constant currency, a marked acceleration from fiscal 2026 levels.

The Zacks Consensus Estimate for ORCL’s fiscal 2027 earnings is pegged at $8.03, which suggests 5.24% growth over the figure reported in fiscal 2026.

For fiscal 2027, Oracle reaffirmed its $90 billion total revenue target and raised its non-GAAP earnings-per-share guidance to $8.05, representing 18% growth after adjusting for one-time gains booked in fiscal 2026. Oracle also indicated it does not expect to issue additional debt during 2026, noting that prepaid and customer-supplied hardware tied to its largest AI contracts now total $75 billion, reducing the capital it must independently raise. This combination of accelerating top-line guidance and a funding plan that leans partly on customer contributions offers a more balanced financing picture than the headline capital expenditure figures alone might suggest.

Oracle Corporation Price and Consensus

Oracle Corporation price-consensus-chart | Oracle Corporation Quote

Diversification Beyond the Core Database Business

A third reason centers on Oracle's expanding footprint outside traditional licensing. The company reported that its Multicloud AI Database business grew 404% in the fourth quarter, which it described as its fastest-growing offering ever. Separately, Oracle said its Health application suite will soon incorporate a new AI-driven version of its Cerner patient care management system, which management expects to push overall Oracle Health growth into double digits in fiscal 2027. These initiatives suggest that Oracle's AI strategy extends beyond raw infrastructure capacity into higher-margin software and healthcare applications, potentially cushioning results if cloud infrastructure growth normalizes from its current elevated pace.

Headwinds That Keep the Outlook Balanced

These positives do not erase the concerns behind the stock's decline. Oracle recorded a negative free cash flow of $23.7 billion in fiscal 2026 as capital investment in data centers outpaced operating cash flow, and the company plans to raise roughly $40 billion more in debt and equity during fiscal 2027, including a previously announced $20 billion at-the-market equity program. Software revenues, historically Oracle's profit anchor, declined slightly for the year, underscoring the ongoing shift away from legacy licensing. Oracle has also flagged risks around its ability to secure sufficient data center capacity, source graphics processing units and manage complex, large-scale government and enterprise contracts, any of which could affect the pace at which today's record backlog converts into recognized revenues. Until financing costs and capital intensity show clearer signs of moderating, near-term price swings are likely to persist, keeping the investment case dependent on execution rather than sentiment alone.

Valuation and Competitive Landscape

From a valuation standpoint, ORCL stock is currently trading at a premium with a trailing 12-month Price/Earnings ratio of 22.64x, which is higher than the sector’s average of 0.96x. Oracle carries a Value Score of C. This reflects investor expectations for the accelerating cloud growth outlined in Oracle's own forward guidance.

ORCL’s Premium P/E TTM Valuation

Image Source: Zacks Investment Research

Oracle Cloud Infrastructure continues expanding against AmazonAMZN, MicrosoftMSFT and AlphabetGOOGL-owned Google, the three largest hyperscalers by cloud footprint and Oracle's primary rivals in enterprise AI workloads. Oracle has positioned its Multicloud AI Database, now available across Amazon and Microsoft data centers, with Google integration also underway, as a differentiator, letting customers run Oracle databases directly inside rival cloud environments. While Amazon and Microsoft maintain broader overall infrastructure scale, and Google keeps expanding its AI-optimized capacity, Oracle's fastest-growing segment and multicloud partnerships carve out a distinct niche. Continued execution relative to these rivals will determine whether Oracle's current valuation premium proves justified by delivered growth.

Conclusion

Oracle's record backlog, accelerating fiscal 2027 guidance, and expanding AI database and healthcare initiatives support holding the stock despite its steep year-to-date decline. However, heavy capital spending, rising debt financing needs, and execution risk mean investors should monitor upcoming quarterly results closely rather than adding aggressively in the near term. ORCL stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).