Should Investors Bet, Hold, or Offload CRWV Stock Before Q4 Earnings?

CoreWeave, Inc. CRWV is scheduled to report fourth-quarter 2025 results on Feb. 26, after market close.

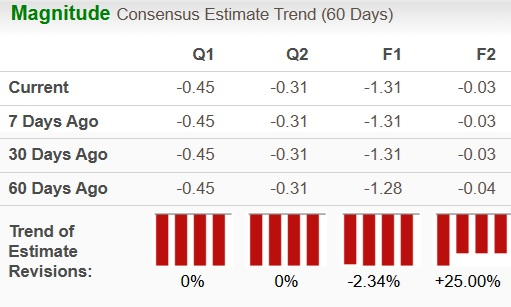

The Zacks Consensus Estimate for the bottom line in the to-be-reported quarter is pegged at a loss of 45 cents, unchanged in the past 60 days. The consensus estimate for total revenues is pinned at $1.5 billion.

Image Source: Zacks Investment Research

CoreWeave, which went public in March 2025, will report its fourth earnings release since the IPO. It has positioned itself as a purpose-built AI cloud provider that scales GPU capacity aggressively for model training and inference.

CRWV’s loss narrowed to 22 cents per share in the third quarter from a loss of $1.82 in the year-ago quarter. Adjusted net loss for the quarter was $41 million against adjusted net income of $67 million a year ago.

What Our Model Predicts for CRWV

Our proven model does not predict an earnings beat for CRWV this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is not exactly the case here. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

CRWV has an Earnings ESP of 0.00% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Key Factors Investors Should Not Ignore

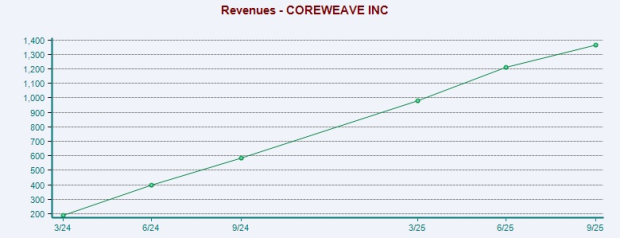

CoreWeave’s fourth-quarter performance is likely to have been driven by booming AI cloud demand, enhanced revenue visibility from backlog expansion and a steadily widening customer mix. With strong visibility into future demand, the company is accelerating capacity expansion and solidifying its AI cloud dominance, as fresh product rollouts, high-value partnerships, and federal engagements power its hypergrowth trajectory. In the last reported quarter, CRWV’s revenues jumped 134% year over year, driven by increasing demand for the AI-cloud platform.

CRWV’s order pipeline and backlog trends can provide insight into future revenue stability. A strong order book suggests sustained momentum, while weakening demand could signal near-term headwinds. Growth has been fueled by multi-billion-dollar AI cloud deals. In 2025, it expanded its OpenAI partnership to as much as $22.4 billion in total contracts and signed a Meta capacity agreement worth up to $14.2 billion through 2031. These long-term commitments significantly enhance revenue visibility and growth predictability.

Strong demand has sharply reduced customer concentration, with no single client accounting for more than 35% of backlog in the third quarter, down from 50% in the second quarter and 85% at the start of the year. Over 60% of backlog now comes from investment-grade customers, highlighting successful diversification.

Image Source: Zacks Investment Research

Strategic ties with NVIDIA Corporation NVDA, the dominant manufacturer of GPUs used in AI computing, continue to power CRWV’s revenues and profitability. In January 2026, NVDA invested $2 billion into CoreWeave, nearly doubling its stake, to expand data centers aimed at 5 gigawatts of capacity by 2030, reflecting confidence in AI demand and CoreWeave’s role in meeting it. To strengthen its AI infrastructure footprint, CRWV announced plans to integrate NVIDIA’s Rubin technology into its AI cloud platform. As one of the first cloud providers expected to deploy Rubin in the second half of 2026, the company is positioning itself at the forefront of agentic AI, advanced reasoning models and large-scale inference workloads.

CRWV’s disciplined capacity expansion lifted contracted power to 2.9 GW in the third quarter, with no data center partner accounting for more than roughly 20%, improving resilience and geographic diversification. The company also walked away from the Core Scientific acquisition on valuation grounds, noting the decision does not affect its growth outlook and that it will continue leveraging the approximately 590 MW already leased. Expanding its capacity and service offerings remains a key performance catalyst to its success in a structurally undersupplied market.

However, powered shell delays are set to drag on fourth-quarter results, with softer 2025 revenue and profit guidance, even though active power is still expected to exceed 850 MW by year-end. As major deployments come online in the fourth quarter, a timing gap between initial cost outlays and revenue contribution will likely weigh on adjusted operating margins in the quarterly numbers. Nonetheless, with powered shell deliveries taking longer, more infrastructure is staying in the build phase, pushing most of the previously expected fourth-quarter spend into first-quarter 2026.

CRWV Stock vs. Industry

CRWV shares have rallied 123.1% in the past year, outperforming the Zacks Internet Software industry’s fall of 14.6%. The stock has also outpaced the Zacks Computer & Technology sector and the S&P 500’s growth of 25% and 18.2%, respectively.

Image Source: Zacks Investment Research

The company has outperformed its peers and tech behemoths like Microsoft MSFT, which has declined 1.7% during the same time frame, while Nebius Group N.V. NBIS, another strong contender in the AI infrastructure space, has risen 170.4%.

Key Valuation for CRWV

In terms of Price/Book, CRWV shares are trading at 8.89X, higher than the Internet Software industry’s 5.03X, but it could mean more risk than opportunity.

Image Source: Zacks Investment Research

NBIS and MSFT shares are trading at multiples of 5.35X and 7.55X, respectively.

Our Verdict: Stay Put on CRWV for Now

CRWV continues to benefit from structural AI demand, multi-year hyperscaler and enterprise contracts, and a rapidly expanding power and data center footprint. Its growing backlog, improving customer diversification, and rising share of investment-grade clients strengthen revenue quality and reduce concentration risk. These factors support a long runway for hypergrowth and make the long-term story compelling. However, the near term is challenging. Delays in powered shell deliveries, the timing mismatch between upfront infrastructure costs and revenue recognition, and the shifting CapEx cycle are expected to weigh on fourth-quarter margins and push some financial benefits into future quarters.

The stock appears to be treading in the middle of the road, and new investors could be better off if they trade with caution.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Nebius Group N.V. (NBIS): Free Stock Analysis Report

CoreWeave Inc. (CRWV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).