Here's How to Play Newmont Stock Before Q1 Earnings Release

Newmont CorporationNEM is slated to report first-quarter 2026 results after the closing bell on April 23. The mining giant is expected to have benefited from higher gold prices in the quarter amid headwinds from weaker production and higher costs.

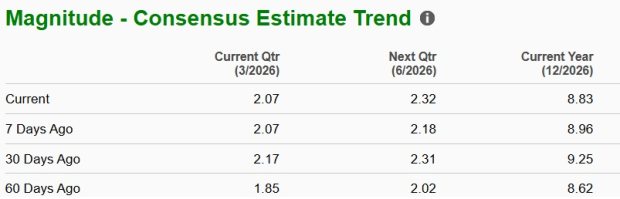

The Zacks Consensus Estimate for first-quarter earnings was revised upward in the past 60 days. The consensus estimate for earnings is pegged at $2.07 per share, suggesting a 65.6% year-over-year rise. The Zacks Consensus Estimate for first-quarter revenues currently stands at $6.36 billion, indicating a roughly 27% increase from the year-ago quarter.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

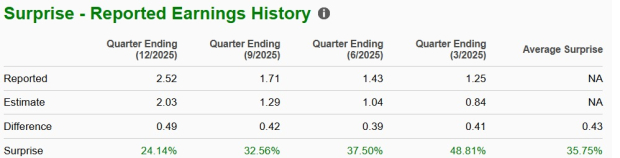

NEM beat the Zacks Consensus Estimate for earnings in each of the last four quarters. It has a trailing four-quarter earnings surprise of 35.8%, on average.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Q1 Earnings Whispers for NEM

Our proven model predicts an earnings beat for NEM this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. That is just the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

NEM has an Earnings ESP of +1.16% and a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Shaping NEM’s Q1 Results

The impact of higher gold prices is expected to be reflected in Newmont’s results for the to-be-reported quarter. Higher realized gold prices are likely to have driven its top line and margins.

Gold entered 2026 with a stronger momentum after racking up a 65% gain in 2025. U.S.-Iran tensions, a weaker U.S. dollar and concerns over the independence of the Federal Reserve fueled the spike in bullion to record levels, with prices soaring to a fresh high of nearly $5,600 per ounce in late January. This was followed by a brief pullback to below $4,900 per ounce due to aggressive profit-booking and a rebound in the U.S. dollar.

Bullion strengthened again early last month, surging past $5,400 per ounce on March 2, as safe-haven demand spiked, following joint U.S.-Israel strikes on Iran. A stronger U.S. dollar, inflation fears tied to a spike in oil prices and the Fed’s hawkish tone weighed on gold prices around late March, dragging bullion to near $4,400 per ounce on March 26. This was followed by a recovery to above $4,600 per ounce to close the month 12% lower.

Despite the plunge in March, prices of the yellow metal closed roughly 7% higher in the first quarter. Our estimate for the average realized prices of gold for NEM stands at $4,934 per ounce, which indicates a 67.6% year-over-year rise.

Newmont’s first-quarter performance is likely to be impacted by weaker production and higher costs. NEM saw lower gold production for the fourth quarter of 2025, partly linked to its strategic divestment of non-core assets. NEM reported a roughly 24% year-over-year decline in gold production to 1.45 million ounces, although increasing modestly from the prior quarter. The company also reported a roughly 14% year-over-year decline in gold production in 2025, reaching 5.89 million ounces. The company anticipates gold production at about 5.26 million ounces for 2026, indicating a year-over-year decline.

Lower production is also expected to lead to higher unit costs in 2026. NEM expects all-in-sustaining costs (AISC) — a critical cost metric for miners — to be $1,680 per ounce on a by-product basis, a notable increase from $1,358 per ounce in 2025. The expected increase is due to lower sales volumes as a result of planned mine sequencing, higher royalties and production taxes, deferral of sustaining capital from 2025 into 2026 and inventory changes.

Our estimate for attributable gold production stands at 1.22 million ounces for the first quarter, which indicates a 20.3% year-over-year decline.

Newmont Stock’s Price Performance and Valuation

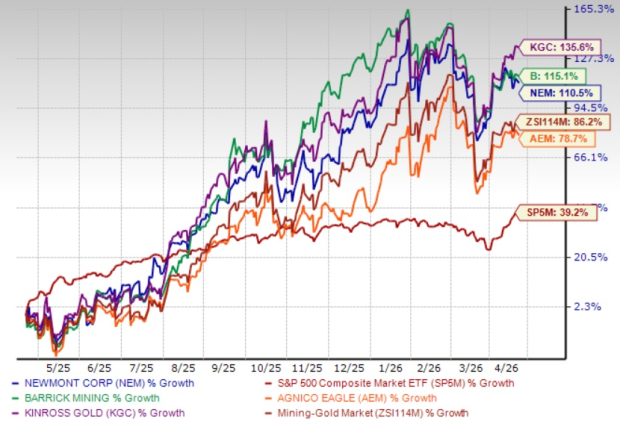

Newmont’s shares have surged 110.5% in the past year, outperforming the Zacks Mining – Gold industry’s 86.2% increase and the S&P 500’s rise of 39.2%. Its gold mining peers, Barrick Mining CorporationB, Agnico Eagle Mines LimitedAEM and Kinross Gold CorporationKGC have surged 115.1%, 78.7% and 135.6%, respectively, over the same period.

NEM’s One-year Price Performance

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

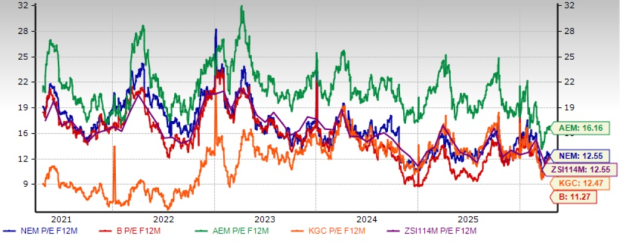

From a valuation standpoint, Newmont is currently trading at a forward 12-month earnings multiple of 12.55, in line with the peer group average. NEM is trading at a premium to Barrick and Kinross Gold and at a discount to Agnico Eagle. Newmont, Barrick and Kinross Gold have a Value Score of B, while Agnico Eagle currently has a Value Score of D.

NEM’s P/E F12M Vs. Industry, B, AEM and KGC

Image Source: Zacks Investment Research

Investment Thesis for NEM Stock

Newmont is well-placed for growth with a robust portfolio of projects, which should expand production capacity and extend mine life, thereby driving revenues and profits. The acquisition of Newcrest Mining Limited has also created an industry-leading portfolio and is expected to deliver significant value for its shareholders and generate meaningful synergies. The asset streamlining rooted in Newmont’s objective to concentrate capital on high-return, long-life assets underpins its long-term sustainability.

NEM has a strong liquidity position and generates substantial cash flows, which allows it to fund its growth projects, meet short-term debt obligations and drive shareholder value. As a leading gold producer, Newmont stands to benefit from favorable gold prices, which should boost its profitability and drive cash flow generation.

However, weaker gold production and higher costs cast a pall on Newmont’s prospects. The anticipated production decline due to divestments and lower grades could undercut the profitability goals.

Final Thoughts: Hold Onto NEM Shares

Newmont is well-positioned for future expansion, supported by the solid performance of its assets and a strong pipeline of projects that are expected to lift production capacity and prolong mine life, thereby fueling revenue and earnings growth. Its asset optimization strategy, focused on allocating capital to high-return, long-life operations, further strengthens its long-term outlook. Elevated gold prices should also enhance margins and cash flow generation. However, softer production levels and higher expected costs could pressure near-term results. Investors who already own NEM shares may consider maintaining their positions while awaiting greater visibility following the company’s upcoming earnings release.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).