Omnicom's Q4 Earnings and Revenues Miss Estimates, Increase Y/Y

Omnicom OMC reported unimpressive fourth-quarter 2025 results, with both earnings and revenues missing the Zacks Consensus Estimate.

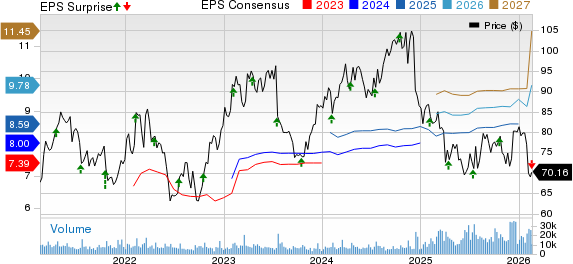

OMC’s earnings were $2.59 per share, missing the Zacks Consensus Estimate by 11.9% but increasing 7.5% from the year-ago quarter. Total revenues came in at $5.5 billion, lagging the consensus estimate by 25.3% but rising 27.9% on a year-over-year basis.

OMC shares have declined 12.7% in the past year compared with 24.5% decline of the industry. In contrast, the Zacks S&P 500 composite has risen 13.9% in the said time frame.

Omnicom Group Inc. Price, Consensus and EPS Surprise

Omnicom Group Inc. price-consensus-eps-surprise-chart | Omnicom Group Inc. Quote

OMC’s Q4 Revenue Breakdown by Disciplines and Regions

Media & Advertising contributed 60.1% of revenues in the quarter, while Precision Marketing contributed 10.3%. Public Relations, Healthcare, Experiential, Execution & Support, and Branding & Retail Commerce contributed 9.1%, 7.3%, 6.5%, 3.7% and 3.0%, respectively.

Across regional markets, the contribution was 51.9% from the United States and 17.6% from the Euro Markets and Other Europe. The United Kingdom contributed 9.6%, while Asia Pacific, Latin America, the Middle East and Africa, and Other North America contributed 10.7%, 3.7%, 3.7% and 2.4%, respectively.

OMC’s Margin Performance

Adjusted EBITA in the quarter came in at $928.9 million, up 28.6% year over year. The adjusted EBITA margin was 16.8%, up 10 basis points year over year. The operating loss was $977.2 million against an operating profit of $685.3 million in the year-ago quarter.

OMC currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Recent Earnings Snapshot

Waste Connections, Inc. WCN reported impressive fourth-quarter 2025 results.

Waste Connections’ adjusted earnings (excluding 28 cents from non-recurring items) of $1.29 per share marginally surpassed the Zacks Consensus Estimate and increased 11.2% year over year. WCN’s revenues of $2.4 billion met the consensus estimate and grew 5% from the year-ago quarter.

Equifax Inc. EFX posted impressive fourth-quarter 2025 results.

EFX’s adjusted earnings were $2.09 per share, outpacing the Zacks Consensus Estimate by 2.5% but declining 1.4% from the year-ago quarter. Equifax’s total revenues of $1.6 billion surpassed the consensus estimate by 1.3% and grew 9.2% on a year-over-year basis.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Omnicom Group Inc. (OMC): Free Stock Analysis Report

Equifax, Inc. (EFX): Free Stock Analysis Report

Waste Connections, Inc. (WCN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).