Opendoor (OPEN): Buy, Sell, or Hold Post Q4 Earnings?

What a brutal six months it’s been for Opendoor. The stock has dropped 23.2% and now trades at $5.35, rattling many shareholders. This might have investors contemplating their next move.

Is now the time to buy Opendoor, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Opendoor Will Underperform?

Despite the more favorable entry price, we're cautious about Opendoor. Here are three reasons we avoid OPEN and a stock we'd rather own.

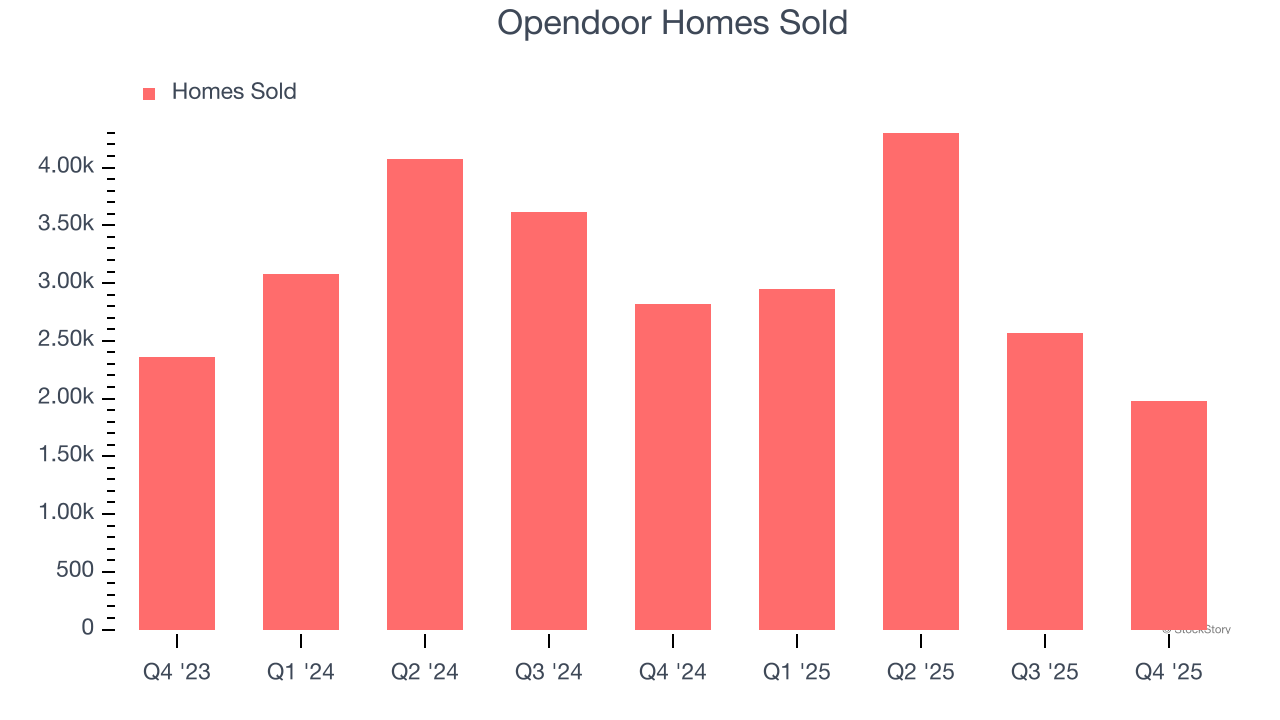

1. Decline in Homes Sold Points to Weak Demand

Revenue growth can be broken down into changes in price and volume (for companies like Opendoor, our preferred volume metric is homes sold). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Opendoor’s homes sold came in at 1,978 in the latest quarter, and over the last two years, averaged 7.7% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Opendoor might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

2. Cash Flow Margin Set to Decline

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the next year, analysts predict Opendoor will flip from cash-producing to cash-burning. Their consensus estimates imply its free cash flow margin of 23.7% for the last 12 months will decrease to negative 3.8%.

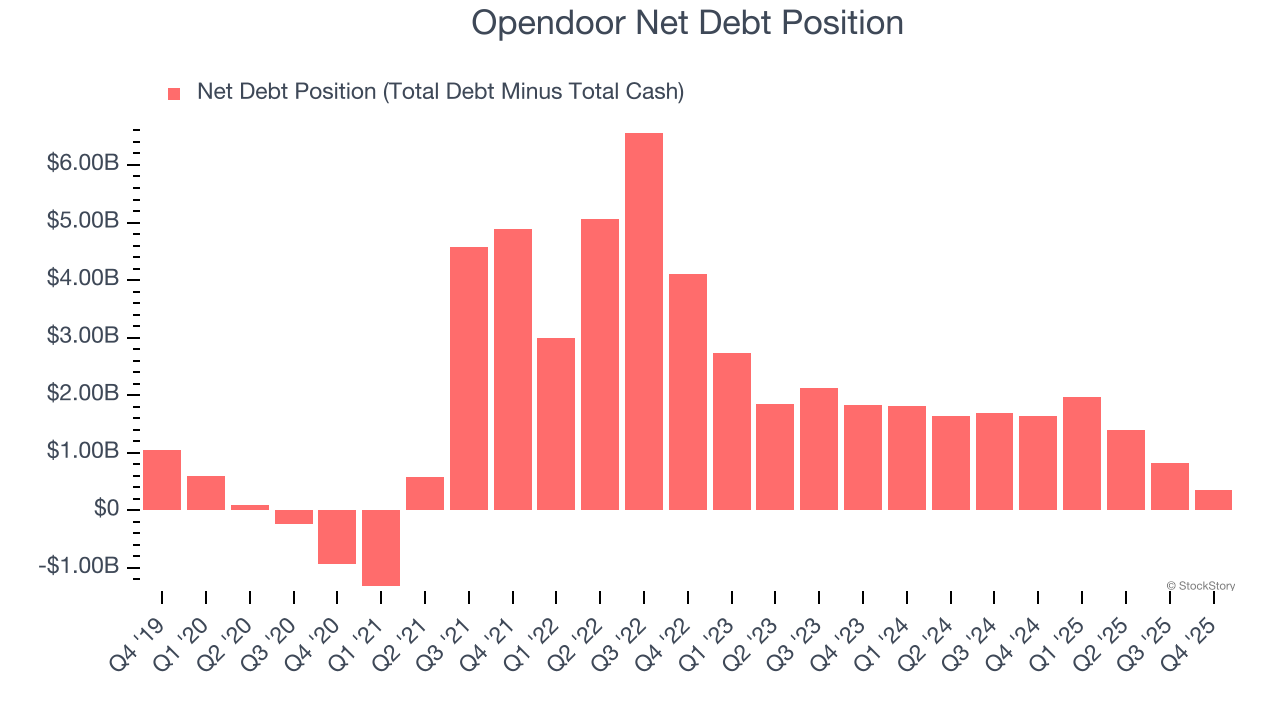

3. Restricted Access to Capital Increases Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Opendoor posted negative $83 million of EBITDA over the last 12 months, and its $1.32 billion of debt exceeds the $962 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade Opendoor if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Opendoor can improve its profitability and remain cautious until then.

Final Judgment

Opendoor doesn’t pass our quality test. After the recent drawdown, the stock trades at $5.35 per share (or a forward price-to-sales ratio of 1.1×). The market typically values companies like Opendoor based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy. We’d suggest looking at the most entrenched endpoint security platform on the market.

Stocks We Like More Than Opendoor

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.