IBM Beats Q1 Earnings Estimates on Solid Revenue & Margin Expansion

International Business Machines CorporationIBM reported strong first-quarter 2026 results, with adjusted earnings and revenues beating the respective Zacks Consensus Estimate.

The company witnessed healthy demand trends for hybrid cloud and artificial intelligence (AI) solutions with a client-focused portfolio and broad-based growth. Despite economic uncertainty stemming from geopolitical conflicts and volatility in crude oil prices, the company expects to deliver sustainable growth through advanced technology and deep consulting expertise, supported by diversity across businesses, geographies and industries.

Net Income

On a GAAP basis, net income for the reported quarter was $1.216 billion or $1.28 per share compared with $1.055 billion or $1.12 per share in the year-ago quarter. The significant improvement in GAAP earnings was primarily due to top-line growth.

Excluding non-recurring items, non-GAAP net income from continuing operations was $1.91 per share compared with $1.60 in the prior-year quarter. The bottom line beat the Zacks Consensus Estimate by 10 cents.

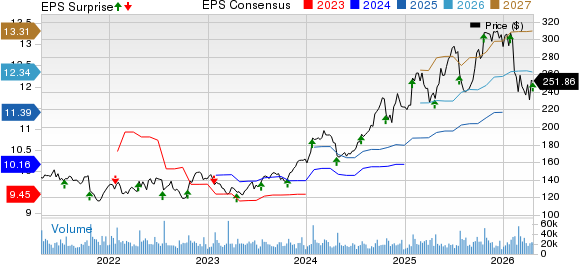

International Business Machines Corporation Price, Consensus and EPS Surprise

International Business Machines Corporation price-consensus-eps-surprise-chart | International Business Machines Corporation Quote

Quarter Details

Quarterly total revenues increased to $15.92 billion from $14.54 billion on strong demand for hybrid cloud and AI, driving growth in the Software segment. On a constant currency basis, revenues were up 6% year over year. The top line exceeded the consensus estimate of $15.68 billion.

Gross profit increased to $8.95 billion from $8.03 billion in the prior-year quarter, resulting in respective gross margins of 56.2% and 55.2%, driven by a solid portfolio mix. Total expenses increased to $7.56 billion from $6.87 billion on higher research and development costs.

Segmental Performance

Software: Revenues improved to $7.05 billion from $6.34 billion, driven by growth in Hybrid Cloud (up 10% year over year), Automation (7%), Data (16%) and Transaction Processing (2%). Segment profit was $2.1 billion compared with $1.85 billion in the year-ago quarter for margins of 29.8% and 29.1%, respectively. The company is witnessing healthy hybrid cloud adoption by clients and solid demand trends across automation and generative AI offerings like watsonx.

Consulting: Revenues were $5.27 billion compared with $5.07 billion a year ago, with growth in Strategy and Technology, and Intelligent Operations. Segment profit remained flat at $558 million, while margin declined to 10.6% from 11% a year ago.

Infrastructure: Revenues were $3.33 billion compared with $2.89 billion on higher demand for hybrid and distributed infrastructure. Segment profit was $524 million compared with $248 million in the year-ago quarter, for respective margins of 15.8% and 8.6%. This reflected strength in the IBM Z, Power and Storage offerings. Higher investments in the business across areas like AI, hybrid cloud and quantum also buoyed segment performance.

Financing: Revenues improved to $220 million from $191 million a year ago. Segment profit was up to $118 million from $69 million in the year-ago quarter for respective margins of 53.8% and 35.8%.

Cash Flow & Liquidity

During the quarter, IBM generated $5.17 billion in cash from operations compared with $4.37 billion in the year-ago quarter. Free cash flow was $2.22 billion in the quarter, up from $1.96 billion in the prior-year period, driven by higher profit and working capital efficiencies. As of March 31, 2026, the company had $10.82 billion in cash and cash equivalents with $57.71 billion of long-term debt.

Outlook

For 2026, the company expects revenues to grow more than 5% on a constant currency basis, driven by a strong portfolio mix, operating leverage and yield from productivity initiatives. Free cash flow is expected to increase by about $1 billion year over year.

Zacks Rank

IBM currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Upcoming Releases

Arista Networks Inc.ANET is scheduled to release first-quarter 2026 earnings on May 5. The Zacks Consensus Estimate for earnings is pegged at 81 cents per share, suggesting a growth of 24.6% from the year-ago reported figure.

Arista has a long-term earnings growth expectation of 17.9%. Arista delivered an average earnings surprise of 9% in the last four reported quarters.

Akamai Technologies, Inc. AKAM is slated to release first-quarter 2026 earnings on May 7. The Zacks Consensus Estimate for earnings is pegged at $1.61 per share, indicating a 5.3% decline from the year-ago reported figure.

Akamai has a long-term earnings growth expectation of 7%. Akamai delivered an average earnings surprise of 9.4% in the last four reported quarters.

Pinterest, Inc.PINS is set to release first-quarter 2026 earnings on May 4. The Zacks Consensus Estimate for earnings is pegged at 22 cents per share, implying a fall of 4.3% from the year-ago reported figure.

Pinterest has a long-term earnings growth expectation of 24.5%. Pinterest delivered an average negative earnings surprise of 3.6% in the last four reported quarters.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).