SoundHound (SOUN) vs. Palantir (PLTR): Which AI Stock Should You Buy Ahead of Q1 Earnings?

AI companies SoundHound AI (SOUN) and Palantir Technologies (PLTR) are set to report their Q1 2026 earnings, and investors are weighing which stock offers the better opportunity. Palantir will report on May 4, while SoundHound is likely to report in the first or second week of May. Using TipRanks’ Stock Comparison tool, we compared SOUN and PLTR to see which stock analysts favor ahead of earnings. Currently, SOUN carries a Strong Buy rating with over 85% upside potential. In comparison, PLTR has a Moderate Buy rating, with a more modest upside of around 36%.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Both companies are part of the AI boom, but they operate differently. Palantir focuses on data platforms and government clients, while SoundHound is focused on voice AI and fast-growing consumer and enterprise applications. Year-to-date, PLTR stock is down almost 20%, while SOUN has fallen 22%.

Let’s dig deeper.

What Analysts Expect from Palantir’s Q1 Earnings

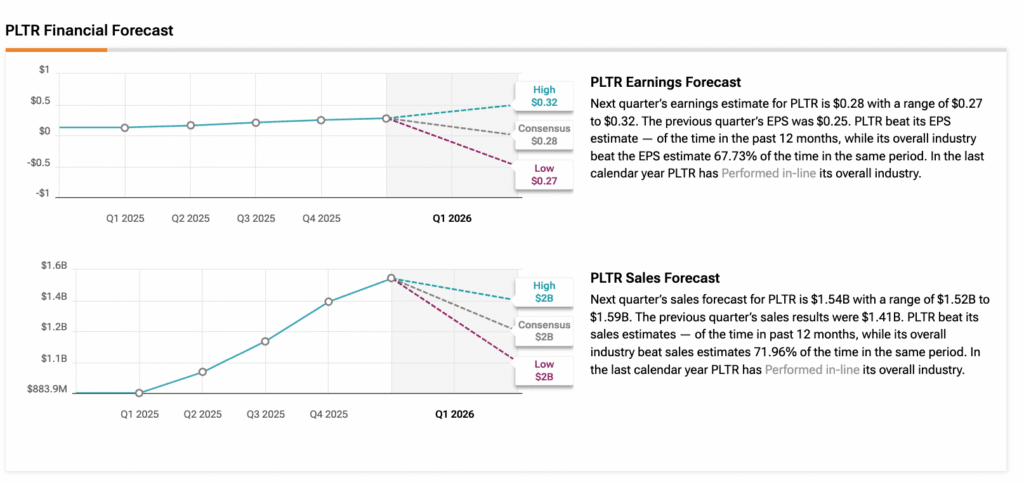

Wall Street expects Palantir to report Q1 2026 earnings per share (EPS) of $0.28, up from $0.13 a year ago. At the same time, revenue is projected to rise over 70% to $1.54 billion.

The company is heading into Q1 earnings with high expectations after a strong Q4 2025. Investors are focused on whether Palantir can maintain its fast AI-driven growth in the U.S. commercial segment. The key question is whether revenue will keep accelerating or start to slow.

Analysts’ Views on PLTR

On Wall Street, analysts are divided. Bulls point to Palantir’s strong AI momentum and growing demand in the U.S. commercial segment as key drivers of future growth. Bears, however, remain cautious about the stock’s high valuation and question whether this pace of growth can be sustained.

Recently, DA Davidson’s four-star-rated analyst Gil Luria reiterated his Hold rating on PLTR. He called it “the best story in software,” but flagged valuation as the key concern. He sees Palantir as a critical enabler of AI, helping companies safely deploy AI tools across their operations rather than competing with players like OpenAI. While this strong positioning supports long-term growth, Luria believes much of that upside is already priced into the stock.

Before this, Mizuho analyst Gregg Moskowitz lowered his price target on PLTR to $185 from $195 but maintained a Buy rating. He updated his outlook ahead of Q1 earnings, noting that cloud demand and AI adoption remain strong.

What to Expect from SoundHound’s Q1 Earnings

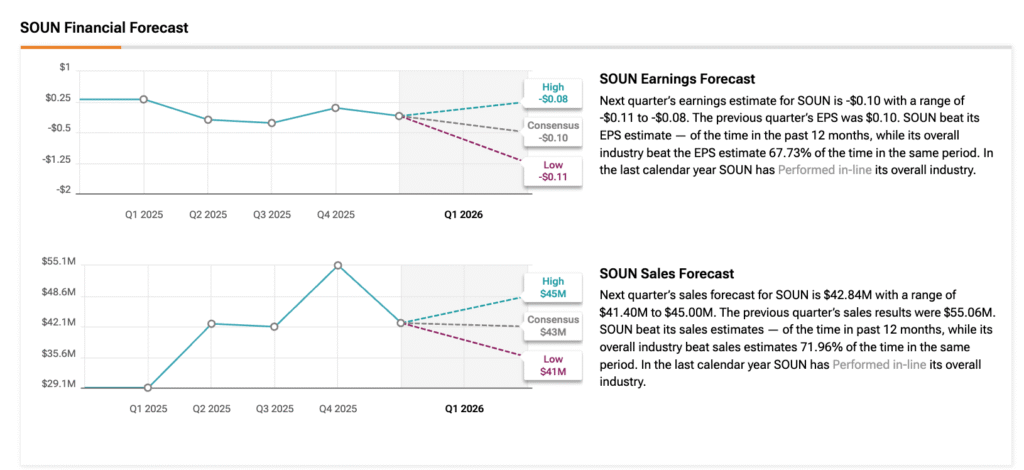

For Q1 2026, analysts expect SoundHound to report revenue of about $42.8 million, up more than 45% year over year. In the previous quarter, the company delivered $55.1 million in revenue, a 59% increase. For full-year 2026, SoundHound is guiding for $225 million to $260 million in revenue, reflecting strong growth of 33% to 54%.

Looking ahead, the company aims to become a high-margin business, targeting over 70% gross margins and around 30% EBIT margins. While it hasn’t given clear profitability guidance yet, management says it is moving toward a break-even phase after years of heavy investment.

Analysts Stay Bullish on SOUN Stock

H.C. Wainwright analyst Scott Buck has set a Street-high $20 price target on SOUN stock, implying nearly 160% upside. He expects the company to reach adjusted EBITDA break-even by late 2026 while continuing to focus on growth.

While this approach may pressure margins in the short term, Buck believes SoundHound is well-positioned long term. He points to its scalable voice AI platform and growing enterprise adoption as key drivers of future revenue growth and margin expansion.

Meanwhile, DA Davidson analyst Luria highlighted SoundHound’s solid financial position, pointing to its current ratio of 4.59. He added that the company’s core voice AI business remains healthy and may be undervalued following the recent pullback in the stock.