Should You Buy Comfort Systems Stock Ahead of Q1 Earnings?

Comfort Systems USA, Inc.FIX is slated to report its first-quarter 2026 results on April 23, after market close.

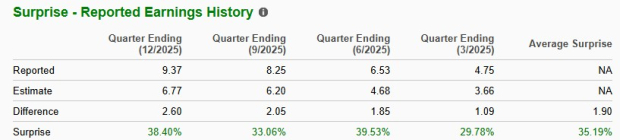

In the last reported quarter, the company’s earnings and revenues topped the Zacks Consensus Estimate by 38.4% and 15.8%, respectively. Adjusted earnings per share (EPS) of $9.37 grew a whopping 129.1% from $4.09 reported in the year-ago quarter. Revenues of $2.65 billion also increased 41.7% on a year-over-year basis.

FIX’s earnings topped the consensus mark in each of the trailing four quarters. The average surprise is shown in the chart below.

Image Source: Zacks Investment Research

How Are Estimates Placed for FIX Stock?

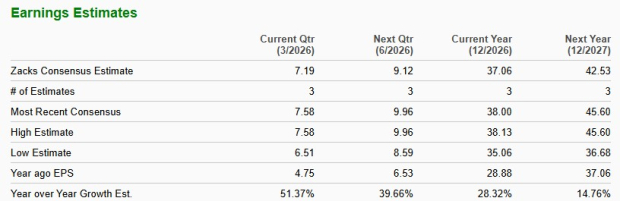

The Zacks Consensus Estimate for first-quarter EPS has increased to $7.19 over the past seven days. The estimate indicates 51.4% growth from the year-ago EPS of $4.75. The consensus mark for revenues is pegged at $2.43 billion, indicating a 32.5% year-over-year increase.

For 2025, Comfort Systems is expected to register a 20.3% increase from a year ago in revenues. Its EPS is expected to grow 28.3% from a year ago. Below is what to expect from the FIX stock.

Image Source: Zacks Investment Research

Factors Likely to Have Defined FIX's Q1 Performance

Strong Backlog Likely Supported Revenues: A key driver of first-quarter performance is expected to be the company’s record backlog of $11.94 billion at the end of 2025, up sharply from $5.99 billion a year earlier. Management noted that backlog growth was led by technology customers, especially data center projects, while pipelines remained solid across manufacturing, healthcare, education and government markets. This large backlog is likely to have provided strong revenue visibility entering 2026.

The company also projected same-store revenue growth in the mid-teen to high-teen percentage range for 2026, with growth weighted more toward the first half. That outlook depicts first-quarter revenues are likely to have benefited from continued project execution across electrical, mechanical and modular operations.

Data center demand remains the biggest tailwind. In 2025, technology customers accounted for 45% of revenue, up from 33% in the prior year, highlighting strong hyperscaler and digital infrastructure spending. Continued momentum in this end market is expected to have supported the March quarter.

However, management also indicated that first-quarter results are usually seasonally lower. In addition, some large operations experienced temporary job shutdowns in January due to ice storms in parts of the South and Southeast, which may have weighed modestly on revenue conversion during the quarter.

Segment-Wise: Comfort Systems operates through two main segments — Mechanical and Electrical. For first-quarter 2026, Comfort Systems’ Mechanical segment (which accounted for 73.3% of total revenues in 2025) is expected to post steady growth, supported by HVAC, piping, modular construction and service demand, particularly from data centers and industrial projects. Modular capacity expansion likely aided revenue conversion, though weather disruptions may have caused some delays. The Zacks Consensus Estimate for the segment’s revenues is currently pegged at $1.75 billion for the first quarter, up from $1.4 billion reported a year ago.

The Electrical segment (26.7%) is expected to outperform again, driven by strong demand for power distribution and controls work tied to hyperscale data centers and other large infrastructure projects. The Zacks Consensus Estimate for the segment’s revenues is currently pegged at $687 million for the first quarter, up from $429.1 million reported a year ago.

Margins Likely Healthy, Though Seasonally Lower: Comfort Systems posted an impressive 25.5% gross margin in fourth-quarter 2025. While management expressed confidence that margins would remain in strong ranges during 2026, it also cautioned that first-quarter margins are typically lower than the full-year average due to seasonal factors.

Still, a favorable project mix, strong pricing discipline, execution gains and growing modular manufacturing scale are likely to have supported profitability. SG&A leverage may have remained a tailwind as revenues continued to rise faster than overhead costs.

Overall, Comfort Systems’ first-quarter results are expected to reflect continued strong demand and execution, offset partly by weather disruptions and normal seasonal softness.

What the Zacks Model Says for FIX Stock

Our proven model predicts an earnings beat for Comfort Systems this time around. A combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. This is exactly the case here.

FIX’s Earnings ESP: The company has an Earnings ESP of +5.42%. You can uncover the best stocks before they’re reported with our Earnings ESP Filter.

FIX’s Zacks Rank: The company currently carries a Zacks Rank of 1. You can see the complete list of today’s Zacks #1 Rank stocks here.

FIX Stock’s Price Performance

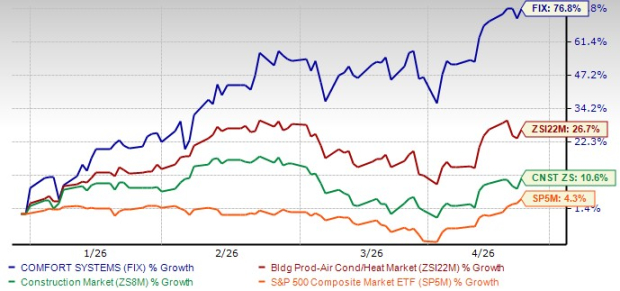

FIX stock has surged 76.8% year to date (YTD), significantly outperforming the Zacks Building Products - Air Conditioner and Heating industry, the Construction sector and the S&P 500 Index.

FIX Stock's Price Performance (YTD)

Image Source: Zacks Investment Research

Comfort Systems sits at a critical execution layer of the AI-driven data center and technology infrastructure boom, competing with Quanta Services, Inc.PWR, EMCOR Group, Inc.EME and Carrier Global Corp.CARR across distinct but overlapping segments. So far this year, FIX has also outperformed these market players, of which Quanta and EMCOR have gained 42.6% and 31.8%, respectively, while Carrier Global has gained 16.1%.

FIX’s Valuation Trend

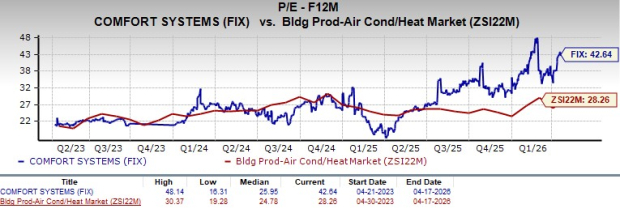

FIX stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 42.64, as evidenced by the chart below.

Image Source: Zacks Investment Research

This is compared with the forward 12-month P/E ratios of 43.7, 27.75 and 21.52 at which Quanta, EMCOR and Carrier Global are currently trading, respectively.

Investment Decision

Comfort Systems looks attractive ahead of first-quarter earnings due to strong growth visibility and AI infrastructure exposure. Its record $11.94 billion backlog, nearly double the year ago, supports steady project execution across data centers, healthcare, manufacturing and government markets. Data center demand remains a major catalyst, with technology customers contributing 45% of 2025 revenue. The company beat earnings estimates in each of the last four quarters, and first-quarter 2026 EPS is expected to rise 51% with revenue up 32.5%, making it appealing for investors seeking momentum and earnings strength.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).