Key Points

The smartphone chipmaker is diversifying into AI infrastructure.

Edge AI compute could be the next craze after data centers.

Today's stock rally reflects the market's confidence in Qualcomm's transformative AI ambitions beyond smartphones.

For years, Qualcomm(NASDAQ:QCOM) has been seen as a premium smartphone chipmaker that raked in billions from the mobile revolution. However, investors may be witnessing the beginning of a new chapter.

At yesterday’s investor day, the company unveiled ambitious plans to more than double its non-handset sales in just three years, to $40 billion. While total revenue growth doesn’t seem significant, what’s huge is the changing revenue composition, driven by AI compute, which signals massive opportunities ahead across multiple large markets. Management estimates a combined total addressable market of $1.7 trillion by 2030.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

Qualcomm stock was up 11% in pre-market trading, and while the initial excitement seems to have worn off, the stock is still up nearly 8.5% by 1:15 p.m. The bigger story, though, is the hidden opportunities for retail investors willing to hold this stock over the next three to five years.

The opportunity no one else is actively pursuing

Qualcomm’s expertise in smartphone chip manufacturing makes it the ideal candidate to pursue a potentially explosive segment lurking in the sidelines: edge AI compute.

Today, most artificial intelligence (AI) models run in the cloud, which explains the explosive growth in data centers worldwide. What’s yet to takeoff at a massive level is the ability to run AI models on the millions of devices themselves, whether owned by individuals or corporations.

Essentially, management at Qualcomm is predicting that AI models will become more efficient in both compute and energy use during inference, which is when the model produces an output based on what it has already learned. Additionally, there will be leaner, task-specific AI models trained for a particular job, which could then reside on the device itself.

Why edge AI matters

As large language models (LLMs) become more sophisticated and capable of performing more generalized tasks, their utility for niche, specialized, and privacy-focused applications could eventually become limited. As AI compute proliferates, the need to reduce latency between the device and the large language model, usually located on a distant server, can’t be overstated. A smartphone camera that needs instant photo processing, or self-driving cars that can’t wait for a response from the cloud, are examples where any latency could be a major hindrance.

The other advantages are increased privacy for in-device processing and lower costs for enterprises looking to wean certain compute activities off expensive data centers.

Expansion into multiple fields

Qualcomm expects to generate $40 billion in non-handset revenue by fiscal 2029. As of the second quarter of fiscal 2026, which ended on March 29, of the total $44 billion in trailing twelve-month sales, non-handset revenue stood at little over $16 billion, and the remaining $27 billion came from its smartphone chip business.

To reach a $40 billion annualized target, management needs to ramp up the non-smartphone business by a massive 150% over the next three and a half years, with edge computing contributing more than a third of the revenue.

Qualcomm’s foray into data centers could yield $15 billion annually. Meta Platforms(NASDAQ:META), the parent company of Facebook and Instagram, has agreed to use Qualcomm’s data center CPU, the Qualcomm Dragonfly™ C1000, to power its next-generation data centers. The CPU is expected to be in production in the second half of 2028.

The market is already pricing a different business

Today's rally reflects confidence in Qualcomm's transformative AI ambitions beyond smartphones.

The smartphone business is cyclical. People don’t usually upgrade their phones every year, but rather over a three- to four-year period, when existing handsets become obsolete. The result is faltering demand for legacy smartphone chips. Not surprisingly, over the last five years, the stock has gained only 57%, significantly underperforming both the Nasdaq-100 and the S&P 500.

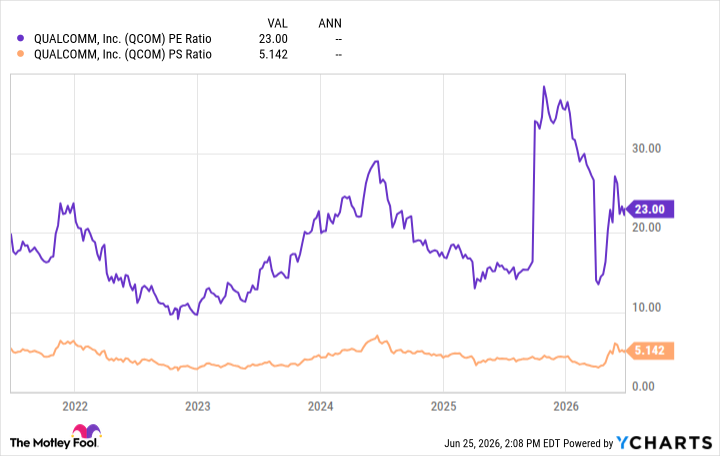

At a little over 23 times trailing 12-month earnings and five times sales, the stock looks quite cheap for a company that is inevitably moving into the red-hot AI-infrastructure business.

.

. QCOM PE Ratio data by YCharts.

Execution holds the key

While ambitions are easy to digest, what is actually challenging is gaining market share. Hyperscalers are competing for the best available chip at the lowest available price. In fact, many of them, such as Alphabet and Amazon, are designing their own chips.

The real question investors must ask is whether Qualcomm can prove it can live up to its ambitions.

Diversifying away from a predominantly single source of income, while initially scary, is a requirement. For Qualcomm, the next decade of growth could look very different from its last.

Should you buy stock in Qualcomm right now?

Before you buy stock in Qualcomm, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Qualcomm wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $387,428!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,221,398!*

Now, it’s worth noting Stock Advisor’s total average return is 895% — a market-crushing outperformance compared to 205% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of June 25, 2026.

Isac Simon has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Qualcomm. The Motley Fool has a disclosure policy.