Darden Stock Trends Show Digital Gains and Margin Pressure

Darden RestaurantsDRI is showing how full-service restaurant operators are adapting to a more selective consumer. Its fiscal 2026 performance benefited from same-restaurant sales gains, brand-level execution and ongoing investments in delivery and development.

The stock story is not only about growth. Darden is also managing a cost environment where pricing decisions, menu value and traffic protection remain central to the margin outlook.

Darden Shows How Value Still Wins Traffic

Olive Garden remains a useful example of how value can support traffic without leaning heavily on broad discounting. The brand’s lighter portion offerings and protein-forward menu additions have expanded guest choice while preserving the affordability message that has long been part of the concept.

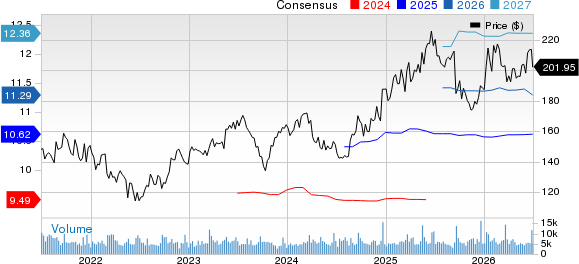

Darden Restaurants, Inc. Price and Consensus

Darden Restaurants, Inc. price-consensus-chart | Darden Restaurants, Inc. Quote

Management has also kept pricing below inflation to protect value perception. That approach may limit near-term margin expansion, but it supports the traffic base that full-service restaurants need when consumers are more careful with discretionary spending.

DRI Digital Efforts Broaden the Customer Mix

Digital convenience is becoming a more visible part of Darden’s operating story. Olive Garden’s partnership with Uber Direct continues to generate incremental orders and attract younger, higher-income customers, giving the brand another way to reach guests outside the dining room.

Yard House is also seeing encouraging early delivery results. That matters because full-service dining has historically been more dependent on in-restaurant occasions than quick-service peers, making digital access a useful way to broaden demand.

Chipotle Mexican GrillCMG remains an important restaurant peer for investors focused on digital ordering and consumer convenience. Restaurant Brands International Inc.QSR, with brands such as Burger King, Tim Hortons, Popeyes and Firehouse Subs, gives investors another comparison point for scale and brand reach across the broader restaurant space.

Darden Uses Brand Variety to Spread Risk

Darden’s portfolio is becoming less dependent on Olive Garden than it was several years ago. Olive Garden represented about 42% of fiscal 2026 sales compared with 50% in fiscal 2019, while other concepts are taking on a larger role in revenue growth.

Cheddar’s Scratch Kitchen, Yard House, Chuy’s and the fine dining brands give Darden multiple demand lanes. That variety can help spread risk when consumer behavior shifts by occasion, price point or dining format.

The company’s reporting structure also reflects this broader mix. In fiscal 2026, Olive Garden accounted for 42.3% of revenues, LongHorn Steakhouse represented 25.9%, Fine Dining contributed 10.4% and Other Business made up 21.3%.

DRI Highlights the Inflation Squeeze on Margins

Cost pressure remains the clearest counterweight to Darden’s growth trends. Management expects total inflation of roughly 3% in fiscal 2027, with beef inflation the highest early in the year before moderating later.

That backdrop creates a trade-off. Darden can protect traffic by holding pricing below inflation, but doing so may keep restaurant margins from expanding as quickly as investors would prefer.

The company’s full-service model also remains tied to discretionary spending. If employment, inflation, fuel prices or consumer confidence weaken, traffic and comparable sales could face pressure even with strong brand execution.

Darden Ratings Reflect Growth Over Momentum

Darden’s current stock signals fit a company with better operating trends than price momentum. The stock carries a Zacks Rank #3 (Hold), which points to a more balanced near-term setup rather than a clear buy signal. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Style Scores add useful context. DRI has a VGM Score of B and a Growth Score of A, supporting the view that earnings growth and operating execution remain relative strengths.

The Value Score of C and Momentum Score of D are more cautious. For investors, that mix suggests Darden’s digital gains, menu work and portfolio diversification are promising trends, but stronger estimate support or price action may be needed before the stock becomes a more decisive market favorite.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).