Is Costco Stock a Buy Now or Still Too Expensive to Touch?

Costco Wholesale CorporationCOST, a prominent player in the membership-based retail sector, is currently trading at a forward 12-month price-to-earnings (P/E) multiple of 46.21, which is above the industry average of 32.63 and the S&P 500's 22.97. The stock is trading marginally below its 12-month median P/E of 48.16. This suggests that although Costco is slightly cheaper than its recent historical average, it remains an expensive stock in a broader market context.

This premium positioning is particularly noticeable compared to peers such as Ross Stores, Inc.ROST, Dollar General CorporationDG and Target CorporationTGT. While Ross Stores trades at a forward 12-month P/E multiple of 26.97, Dollar General and Target trade at 20.72 and 14.75, respectively.

COST Valuation Picture

Image Source: Zacks Investment Research

Has Costco’s Price Run Already Capped Its Upside?

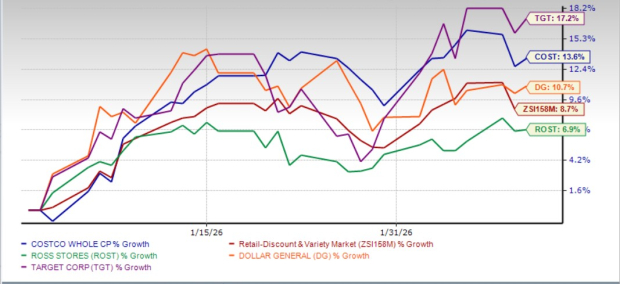

Despite the elevated valuation, investors have shown strong confidence in Costco, supported by its resilient business model, decent membership renewal rates and consistent traffic growth. The company’s ability to deliver steady same-store sales gains and earnings resilience, even in a challenging retail environment, has helped sustain buying interest. The stock has jumped 13.6% so far this year, outperforming the industry’s rise of 8.7%.

During the same period, Costco has outperformed Dollar General and Ross Stores but trailed Target. Shares of Target have advanced 17.2% year to date, while Dollar General and Ross Stores have risen 10.7% and 6.9%, respectively.

COST, ROST, DG & TGT YTD Stock Performance

Image Source: Zacks Investment Research

Costco’s Fundamentals Remain Robust, Yet Fully Valued

Costco’s resilient membership model remains a key growth driver, supported by high renewal rates and operational efficiency. In the first quarter of fiscal 2026, renewal rates stayed robust — 92.2% in the United States and Canada and 89.7% globally — reflecting strong customer loyalty. This, combined with Costco’s bulk purchasing power and efficient supply chain, enables the company to maintain competitive pricing and withstand economic pressures.

Costco’s brand name, geographic presence and product breadth attract customers, resulting in solid comparable sales. Costco reported a 7.1% year-over-year increase in total comparable sales for January. Regionally, comparable sales rose 5.8% in the United States, 11.4% in Canada and 9.5% in Other International markets. This follows total comparable sales growth of 7% in December and 6.9% in November, indicating consistent momentum.

By steadily enhancing its e-commerce capabilities and investing in fulfillment infrastructure, Costco is creating a more integrated omnichannel shopping experience. Digitally enabled comparable sales in January surged 34.4%. This follows gains of 18.9% and 16.6% registered in December and November, respectively, underscoring sustained momentum in the company’s online channel.

To sustain this momentum, Costco is enhancing the online experience with upgraded product pages, improved search and new personalization that recommends relevant items based on members’ search history. It has also expanded purchasing flexibility through its Buy Now Pay Later program, which is particularly helpful for higher-ticket items. Costco's same-day delivery offering, powered by Instacart in the United States and Uber Eats and DoorDash internationally, is performing well. Initiatives like the Costco Digital Wallet and pre-scanning technology are speeding up checkout, while AI is being deployed to optimize pharmacy inventory and improve gas station business management.

Costco’s disciplined focus on cost control, product mix optimization and growing penetration of its private-label brand, Kirkland Signature, continues to support margin expansion. Complementing these initiatives is Costco’s steady pace of new warehouse openings. Management plans to open 28 net new warehouses during fiscal 2026 and aims for 30 or more annual openings in subsequent years. New warehouses are reaching maturity faster, with fiscal 2025 openings generating an annualized $192 million in sales per location during the first year.

Competitive Landscape: Can Costco Stay Ahead?

Costco’s impressive sales growth comes in an increasingly competitive retail environment. While rivals such as Ross Stores, Dollar General and Target continue to invest in value offerings and customer engagement, Costco’s differentiated membership-driven model and private-label strength remain key competitive advantages.

That said, margins remain an area to monitor. Any SG&A deleverage, particularly if discretionary demand softens further, could pressure operating profitability. Foreign exchange volatility and potential tariff-related costs introduce uncertainty. Although consumer spending is tilting toward essentials, which supports Costco’s core offering, weaker discretionary demand could moderate overall basket expansion.

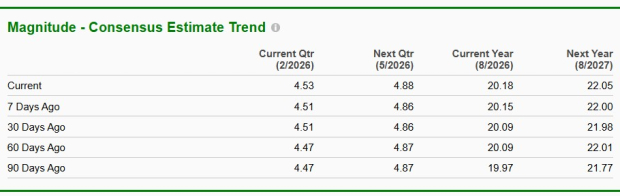

How Consensus Estimates Stack Up for Costco

Wall Street analysts have expressed confidence in Costco by raising their earnings estimates. Over the past 30 days, the Zacks Consensus Estimate for the current and next fiscal years has risen by 9 cents and 7 cents to $20.18 and $22.05 per share, respectively. These estimates indicate expected year-over-year growth rates of 12.2% and 9.3%, respectively.

Image Source: Zacks Investment Research

COST: A Quality Stock but a Hold for Now

Costco’s strong fundamentals, including a growing membership base, solid digital sales, and ongoing investments in its footprint and capabilities, continue to support its market leadership. While the stock’s premium valuation warrants caution, its resilient business model offers a compelling case for long-term investors. The prudent move for existing investors may be to hold their positions rather than chase the stock at its current highs. Prospective investors may prefer to wait for a more attractive entry point to improve the risk-reward profile. Costco currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Dollar General Corporation (DG): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

Ross Stores, Inc. (ROST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).