Ulta Beauty Q4 Earnings & Revenues Beat Estimates, Sales Up 11.8% Y/Y

Ulta Beauty, Inc. ULTA reported fourth-quarter fiscal 2025 results, wherein both top and bottom lines beat the Zacks Consensus Estimate. While net sales increased, earnings decreased from the year-ago period’s actuals.

The company reported fiscal fourth-quarter earnings per share of $8.01, beating the Zacks Consensus Estimate of $8.00. However, the bottom line declined 5.3% compared with the year-ago reported figure.

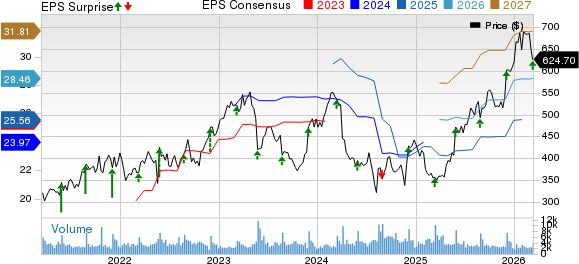

Ulta Beauty Inc. Price, Consensus and EPS Surprise

Ulta Beauty Inc. price-consensus-eps-surprise-chart | Ulta Beauty Inc. Quote

Net sales of this beauty product retailer increased 11.8% year over year to $3,898.4 million and beat the Zacks Consensus Estimate of $3,814 million. This growth was driven by higher comparable sales, the acquisition of Space NK and new store contributions.

Comparable sales rose 5.8%, supported by a 4.2% increase in average ticket size and a 1.6% increase in transactions.

ULTA’s Quarterly Results: Key Metrics & Insights

Ulta Beauty’s gross profit totaled $1,483.6 million, up 11.2% from $1,333.7 million. However, as a percentage of net sales, gross profit decreased 38.1% from 38.2%. The decrease was mainly due to an unfavorable channel mix, deleverage of store fixed expenses and other revenues, partially offset by lower inventory shrink and supply-chain efficiencies.

Selling, general and administrative (SG&A) expenses increased 23% to $1,003.1 million from $815.6 million reported in the prior-year quarter. As a percentage of net sales, SG&A expenses increased to 25.7% from 23.4%. This rise was due to the higher corporate overhead related to strategic enterprise investments, increased advertising expenses and higher incentive compensation.

Operating income was $476.9 million compared with $516.3 million in the prior-year quarter. As a percentage of net sales, operating income was 12.2%, down from 14.8% in the year-ago period.

ULTA’s Financial Health Snapshot & Store Update

This Zacks Rank #3 (Hold) company ended the quarter with cash and cash equivalents of $424.2 million. Net merchandise inventories were $2,181.1 million at the end of the reported quarter. Stockholders’ equity at the end of the quarter was $2,803.5 million. Net cash provided by operating activities was $1,502.8 million for the fiscal year ended Jan. 31, 2026.

In fiscal 2025, the company repurchased 2 million shares of its common stock for $890.5 million, excluding excise taxes. As of Jan. 31, 2026, $1.8 billion remained available under the $3 billion share repurchase program announced in October 2024.

What to Expect From ULTA in FY26

Ulta Beauty expects fiscal 2026 net sales growth in the range of 6% to 7%. Comparable sales growth is expected to be 2.5% to 3.5% year over year.

Management expects an operating income growth between 6% and 9% in fiscal 2026. Earnings per share are envisioned to be in the range of $28.05 to $28.55.

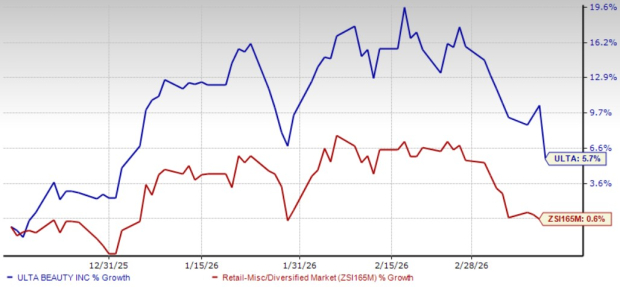

The stock has risen 5.7% in the past three months compared with the industry’s growth of 0.6%.

Image Source: Zacks Investment Research

Stocks to Consider

Five Below, Inc.FIVE operates as a specialty value retailer in the United States and currently flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Five Below’s current fiscal-year sales and earnings calls for growth of 22.1% and 25%, respectively, from the year-ago reported numbers. FIVE delivered a trailing four-quarter earnings surprise of 62.1%, on average.

Ross Stores, Inc. ROST, operates off-price retail apparel and home fashion stores under the Ross Dress for Less and dd's DISCOUNTS brands in the United States. It carries a Zacks Rank #2 (Buy) at present. ROST delivered a trailing four-quarter earnings surprise of 6.2%, on average.

The Zacks Consensus Estimate for Ross Stores’ current fiscal-year sales and earnings implies an increase of 5.6% and 9.4%, respectively, from the prior-year levels.

Williams-Sonoma, Inc. WSM operates as an omni-channel specialty retailer of various products for home. It carries a Zacks Rank #2 at present. WSM delivered a trailing four-quarter average earnings surprise of 8.6%.

The Zacks Consensus Estimate for Williams-Sonoma’s current fiscal-year sales indicates growth of 1.9% from the previous year’s reported figure.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ross Stores, Inc. (ROST): Free Stock Analysis Report

Ulta Beauty Inc. (ULTA): Free Stock Analysis Report

Williams-Sonoma, Inc. (WSM): Free Stock Analysis Report

Five Below, Inc. (FIVE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).