Is ZIM Stock's Cheap Valuation Reason Enough to Bet on it?

ZIM Integrated ShippingZIM shares are one of the cheaper ones in the Zacks Transportation-Shipping industry, with a Value Score of A.

ZIM stock is trading at a significant discount, with a forward 12-month P/S of 0.32X compared with the industry’s 1.95X. ZIM is also cheaper than other shipping stocks like Star Bulk CarriersSBLK and Euroseas ESEA. Star Bulk Carriers and Euroseas have a Value Score of B each.

ZIM’s P/S F12M Vs. Industry, SBLK & ESEA

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

ZIM’s cheap valuation is attractive for investors. However, is it worth buying at current prices? Let’s dig deep to find out.

Major Tailwinds for ZIM Stock

ZIM’s Business Model Looks Impressive

ZIM has an asset-light model, which means that the focus is more on leasing rather than owning vessels. This allows it to adjust capacity rapidly in response to market changes.

ZIM’s focus on niche markets and high-margin trade routes helps it avoid crowded, low-margin segments, thereby maintaining strong pricing power. This, too, aids profitability. The shipping company’s operational efficiency is being aided by investments in digitalization and innovative technologies.

ZIM’s Generous Dividend Payouts Boost Optimism

ZIM’s shareholder-friendly approach reflects its financial prosperity. The shipping company’s high dividend yield is a huge positive for income-seeking investors. This highlights confidence in its cash flow and prospects. In the December quarter, ZIM’s board declared a regular dividend of approximately $382 million or $3.17 per ordinary share.

In the first quarter of 2025, ZIM’s board of directors declared a regular cash dividend of approximately $89 million, or 74 cents per share, reflecting approximately 30% of the quarter’s net income.

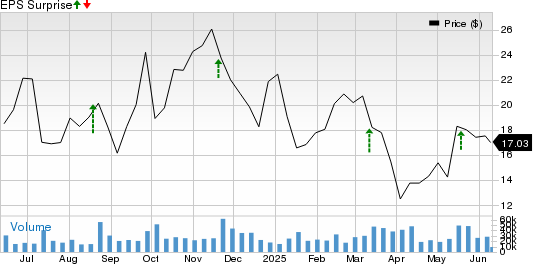

Upbeat Earnings Surprise History

In its recently released first-quarter 2025 results, ZIM continued its streak of beating earnings expectations, showing resilience despite tough conditions. In fact, the shipping stock outpaced the Zacks Consensus Estimate for earnings in each of the last four quarters, with the average being 34.5%.

ZIM Integrated Shipping Services Price and EPS Surprise

ZIM Integrated Shipping Services price-eps-surprise | ZIM Integrated Shipping Services Quote

Some Headwinds

Tariff Tensions: The ongoing trade tension does not bode well for ZIM, as the company has significant exposure to both China and the United States. Transpacific volumes have been suffering due to the trade woes hurting ZIM. Agreed that tariff woes are showing signs of easing, with the United States and China announcing a 90-day suspension on mutual tariffs; however, in the absence of a long-term trade deal, the scenario will continue to be uncertain. Even on the first-quarter conference call, management sounded cautious regarding transpacific trade during the remainder of 2025 in the absence of a longer-term agreement.

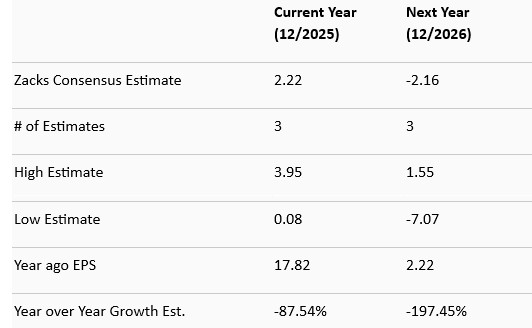

Earnings Estimates Unimpressive for ZIM: The trade tensions are primarily responsible for the year-over-year decline in the 2025 and 2026 earnings estimates of this shipping stock.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

High Debt Load: We are concerned about ZIM’s high debt levels. Long-term debt more than doubled to $4.7 billion at 2024-end from 2019.

Long-Term Debt to Capitalization

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Unimpressive Price Performance of ZIM Stock: Shares of ZIM have not had a good run on the bourses so far this year, declining 19.6% compared with the industry’s 4.8% fall. Star Bulk Carriers and Euroseas have performed much better year to date.

YTD Price Comparison

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Not an Opportune Time to Buy ZIM Stock

There is no doubt that the stock is attractively valued. The company’s shareholder-friendly initiatives also add to its appeal. However, the tariff-induced economic uncertainty clouds its near-term outlook. High debts also do not help matters.

Given the current uncertainty, it is not at all advisable to buy this Zacks Rank #3 (Hold) stock. Investors should monitor the company’s developments closely for an appropriate entry point. For those who already own the stock, it will be prudent to stay invested.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Star Bulk Carriers Corp. (SBLK): Free Stock Analysis Report

Euroseas Ltd. (ESEA): Free Stock Analysis Report

ZIM Integrated Shipping Services Ltd. (ZIM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).