GIS vs. SJM: Which Food Stock Offers Better Upside Today?

General Mills, Inc. GIS and The J. M. Smucker CompanySJM operate at the core of the food industry, which is focused on producing, marketing and distributing branded staples across retail, e-commerce and foodservice channels. This space is shaped by shifting consumer preferences, pricing dynamics and input cost pressures, making brand strength, innovation and supply-chain efficiency essential for sustained performance.

General Mills focuses on a diversified portfolio spanning cereals, snacks, meals and pet food, leveraging scale and omnichannel execution. Coming to J. M. Smucker, the company emphasizes coffee, spreads, frozen handhelds and pet food, with a strong tilt toward branded, value-added offerings. The face-off highlights how each company navigates demand trends, pricing strategies and margin pressures within a competitive packaged foods landscape.

The Case for General Mills

General Mills demonstrates improving competitive traction, supported by strengthening market share trends and household penetration gains across core U.S. categories. The company held or grew pound share in more than 70% of priority businesses in third-quarter fiscal 2026 and in eight of its top 10 categories year to date, reflecting solid positioning within packaged foods. Enhanced baseline volume trends signal stabilizing demand and improving consumer engagement.

The company’s strategy centers on its “remarkability” framework, emphasizing product innovation, pricing architecture, packaging, brand communication and omnichannel execution. Increased investment has driven a roughly 25% rise in new product sales, while e-commerce momentum accelerated significantly across key retail partners. Portfolio breadth across cereal, snacks, pet food and foodservice reinforces its diversified market presence and multi-channel reach.

Despite these strengths, General Mills’ financial performance reflects pressure from reinvestment initiatives, divestitures and input cost inflation. Organic sales declined 3% in the fiscal third quarter, trailing retail sales due to inventory headwinds. Operating profit and earnings dropped more than 30%, highlighting margin compression and the financial trade-offs associated with its strategic repositioning efforts.

Volume softness also persists in select categories, with North America Retail volumes still slightly declining and certain segments like dog feeding facing contraction. External disruptions, including weather-related supply-chain volatility and retailer inventory adjustments, are further impacting consistency. While digital and innovation investments are progressing, execution risks remain as the company balances growth initiatives with cost discipline.

The Case for J. M. Smucker

J. M. Smucker demonstrates solid scale and category presence, with quarterly net sales reaching $2.3 billion, up 7% year over year, and comparable sales rising 8% in third-quarter fiscal 2026. The company’s portfolio spans coffee, pet foods, spreads and frozen handhelds, positioning it across multiple high-demand categories while maintaining broad household penetration and steady share trends in measured retail channels.

SJM’s strategy centers on building leading brands and expanding distribution across channels where consumers shop. Growth platforms like Uncrustables, Cafe Bustelo, Milk-Bone and Meow Mix are driving momentum, supported by consumer-led innovation and targeted marketing. Notably, nearly two-thirds of the portfolio is maintaining or growing dollar share, reflecting effective execution and brand resilience.

Portfolio strength is reinforced by diversified category leadership and targeted demographic appeal. Brands like Uncrustables are expanding into new dayparts and attracting Millennials and families, while Cafe Bustelo resonates with Gen Z and younger consumers. Simultaneously, pet food offerings benefit from premiumization and humanization trends, strengthening J. M. Smucker’s positioning across both food and pet care segments.

However, performance remains uneven across segments, particularly in Sweet Baked Snacks, where net sales declined 19% and profit dropped sharply due to volume pressures, higher costs and operational challenges. Ongoing restructuring actions, SKU rationalization and reduced promotions are expected to improve long-term outcomes, but continue to create near-term volatility in growth, margins and overall portfolio balance.

GIS vs. SJM: How Do Estimates Stack Up?

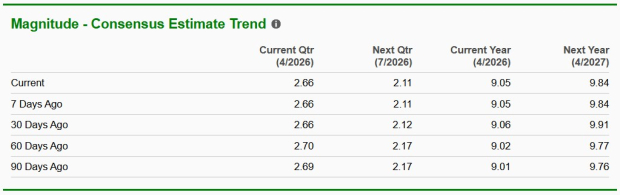

The Zacks Consensus Estimate for General Mills’ current fiscal-year earnings per share (EPS) has moved down 1.7% over the past 30 days to $3.44. The consensus mark indicates a year-over-year decrease of 18.3%.

Image Source: Zacks Investment Research

The consensus estimate for J. M. Smucker’s current fiscal-year EPS has fallen a cent to $9.05 in the past 30 days. The consensus mark implies a 10.6% decline from the year-ago period reported figure.

Image Source: Zacks Investment Research

GIS & SJM: A Look at Past-Year Stock Performance

Over the past year, shares of General Mills have declined 38.8%, underperforming J. M. Smucker and the broader industry, which posted declines of 17.1% and 25.5%, respectively, over the same period.

Image Source: Zacks Investment Research

GIS vs. SJM: A Peek Into Stock Valuation

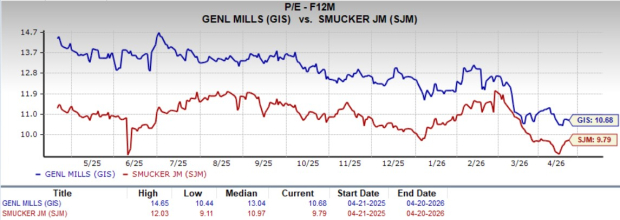

General Mills is trading at a forward 12-month price-to-earnings (P/E) ratio of 10.68, modestly below its one-year median of 13.04. Meanwhile, J. M. Smucker trades at a forward P/E of 9.79, also below its one-year median of 10.97.

Image Source: Zacks Investment Research

GIS vs. SJM: Which Is the Better Bet Now?

Among the two, J. M. Smucker stands out as the stronger near-term story, supported by steadier sales momentum, diversified growth platforms and more stable earnings visibility. Its balanced portfolio across coffee, pet food and frozen offerings continues to support consistent performance in a competitive environment. In contrast, General Mills is in a reinvestment phase, where improving market share and consumer engagement are encouraging, but earnings and margins remain under pressure. For investors prioritizing stability and near-term visibility, J. M. Smucker appears better positioned, while General Mills represents a longer-term recovery opportunity.

SJM currently has a Zacks Rank #3 (Hold), while GIS carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).