ALB vs. SQM: Which Lithium Stock Should You Bet on Now?

Albemarle Corporation ALB and Sociedad Quimica y Minera de Chile S.A.SQM are prominent players in the lithium space. Both are well-placed to benefit from higher lithium prices driven by strong demand from electric vehicles (EVs) and energy storage systems, along with supply disruptions partly due to supply reductions in China. Lithium prices have rebounded from the trough levels seen last year, supported by tightening supply and strong demand in China and globally.

Let’s dive deep and closely compare the fundamentals of these two major lithium stocks to determine the better investment option now.

The Case for ALB

Albemarle is well-placed to gain from long-term growth in the battery-grade lithium market. The market for lithium batteries and energy storage remains strong, especially for EVs, offering significant opportunities for the company to develop innovative products and expand capacity. Lithium demand is expected to grow on the back of significant global EV penetration.

ALB expects lithium demand to witness a compound annual growth rate (CAGR) of 10-20% from 2025 to 2030. Stationary storage is expected to be a significant driver for lithium demand along with EVs. Albemarle expects demand to grow roughly 15-40% this year. Demand indicators stayed positive in the first quarter of 2026, with global Energy Storage Systems production rising 117% year over year.

The company is strategically executing its projects aimed at boosting its global lithium conversion capacity. It remains focused on investing in high-return projects to drive productivity. Healthy customer demand, capacity expansion and plant productivity improvements are supporting its volumes. ALB saw higher sales volumes (up 14% year over year) in its Energy Storage unit in the first quarter on the strength of its integrated conversion facilities.

The Salar yield improvement project in Chile has achieved a 50% operating rate, and the ramp-up continues to deliver encouraging outcomes. ALB has started the environmental permitting process for a commercial direct lithium extraction project at Salar de Atacama. The ramp-up at the Meishan lithium conversion facility in China is also progressing ahead of schedule.

Albemarle is taking aggressive cost-saving and productivity actions. The company delivered roughly $450 million in cost and productivity improvements for full-year 2025, having surpassed its initial target of $300-$400 million. It expects additional cost and productivity improvements of $100-$150 million in 2026, with $40 million already delivered this year. ALB is taking actions to maintain its competitive position, including the initiation of a comprehensive review of cost and operating structure, optimization of the conversion network and reduction of capital expenditure.

Albemarle remains committed to driving shareholder value by leveraging healthy cash flows and strong liquidity. Its operating cash flow was around $1.3 billion in 2025, up roughly 86% from the prior-year period. At the end of the first quarter, ALB had liquidity of around $2.7 billion, including cash and cash equivalents of around $1.1 billion. ALB generated an operating cash flow of $346 million and free cash flow of $248 million in the quarter.

The company paid down $1.3 billion of outstanding debt in March 2026, reducing annual interest expense by roughly $60 million. This followed the successful divestments of the controlling stake in Ketjen and its 50% interest in the Eurecat joint venture, which together generated $670 million in pre-tax proceeds.

The company remains focused on maintaining its dividend payout. It has raised its quarterly dividend for the 30th straight year. ALB offers a dividend yield of 1.2% at the current stock price.

The Case for SQM

Chile-based Sociedad Quimica produces plant nutrients, iodine, lithium and industrial chemicals. SQM is gaining from the favorable trends in the lithium market underpinned by strong EV sales. Higher demand is expected to continue to support the company’s lithium sales volumes.

SQM logged strong lithium sales volumes of 69,000 metric tons in the first quarter on strong market demand, driven by battery energy storage systems. The Nova Andino Litio business recorded roughly 19% higher volumes compared to the prior-year quarter, driven by capacity expansion actions, and the company expects continued sequential increase.

Nova Andino Litio’s average realized sales price increased roughly 95% year over year in the first quarter, and it expects prices to increase further in the second quarter. SQM is operating at full capacity at the Mt. Holland mine and concentrator in Australia and continues to ramp up the Kwinana refinery.

SQM projects global lithium demand to surpass 1.9 million metric tons of LCE this year, along with a tight supply-demand balance. It raised its sales volume guidance for 2026, increasing expected volume growth from 10% to 15%.

Earlier this year, SQM and Codelco completed their strategic partnership to jointly develop the Atacama salt flat. The partnership was completed through the merger by absorption of Codelco’s subsidiary, Minera Tarar SpA, into SQM’s subsidiary, SQM Salar SpA.

This major milestone paves the way for the production of refined lithium in the Salar de Atacama until 2060 and contributes to making Chile a leader in lithium production. Improvements in process efficiency, the adoption of new technologies and the optimization of operations are expected to lead to incremental lithium production through 2060. The first quarter marked SQM’s first full quarter of operation alongside Codelco through the Nova Andino Litio partnership.

Sociedad Quimica’s robust balance sheet supports its capital investment in growth projects and shareholder-friendly actions. It exited the first quarter with strong liquidity, with cash and cash equivalents of around $2.8 billion. Sociedad Quimica, in early December 2025, issued a hybrid bond for roughly $430 million to refinance debt and fund its investment plan. SQM offers a dividend yield of 3.7% at the current stock price.

ALB & SQM: Price Performance, Valuation & Other Comparisons

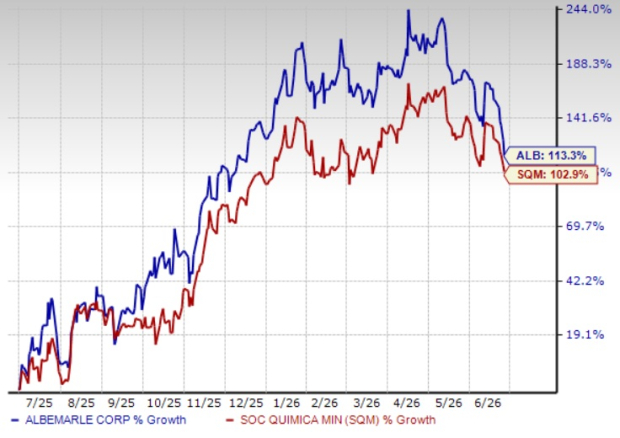

The ALB stock has surged 113.3% over the past year, while SQM has rallied 102.9%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

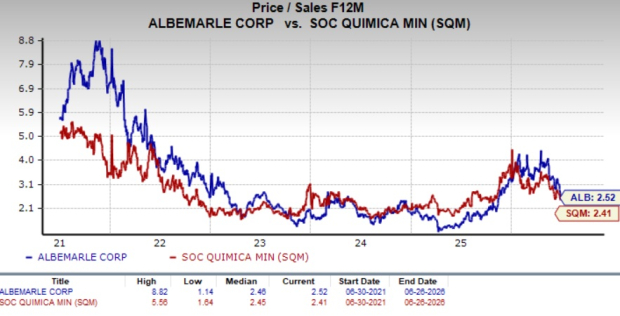

ALB is currently trading at a forward price-to-sales ratio of 2.52. SQM is currently trading at a forward price-to-sales ratio of 2.41, slightly below ALB.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

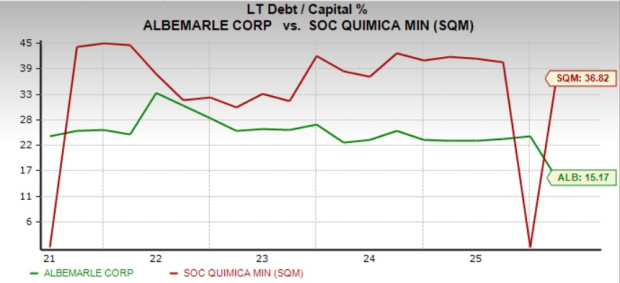

ALB’s long-term debt-to-capitalization is around 15.2%, lower than SQM’s 36.8%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

How the Zacks Consensus Estimate Compares for ALB & SQM

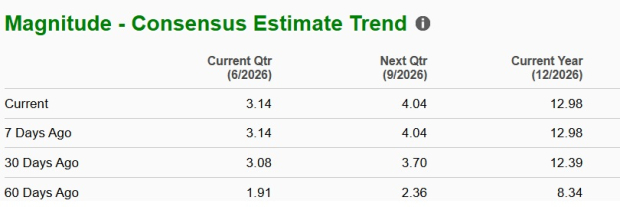

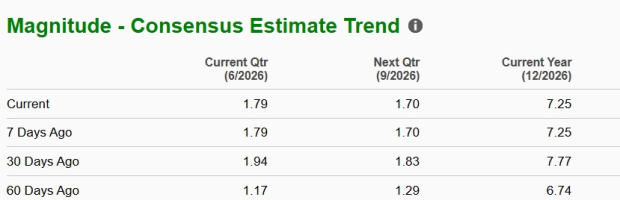

The Zacks Consensus Estimate for ALB’s 2026 sales implies year-over-year growth of 18.2%. The same for EPS suggests a 1,743% year-over-year rise. The EPS estimates for 2026 have been trending higher over the past 60 days.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The consensus estimate for SQM’s 2026 sales and EPS implies a year-over-year rise of 80.2% and 251.9%, respectively. The EPS estimates for 2026 have been trending northward over the past 60 days.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

ALB or SQM: Which Stock Holds the Edge?

ALB and SQM stand to benefit from higher lithium prices driven by EV and energy storage demand. Albemarle is benefiting from higher lithium volumes on project ramp-ups and actions to boost global lithium conversion capacity and productivity. SQM is delivering strong lithium volumes, expanding operations and is expected to benefit from the strategic partnership with Codelco.

ALB's higher earnings growth projections suggest that it may offer better investment prospects in the current market environment. Its lower leverage also suggests lower financial risks. Investors seeking exposure to the lithium space might consider Albemarle as the more favorable option at this time.

ALB currently carries a Zacks Rank #1 (Strong Buy), while SQM has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).