Is FN Stock Worth Betting on at a Premium or Should Investors Wait?

Fabrinet FN is trading at a premium, meaning investors are willing to pay more for the stock. Based on a forward 12-month Price/Earnings (P/E), FN trades at 32.98X, compared with the Zacks Computer and Technology sector’s 25.1X. It also appears to be overvalued relative to peers in the sector, such as Microchip Technology MCHP and TE Connectivity TEL. Microchip and TE Connectivity’s forward earnings sit at 30.87X and 17.73X, respectively. Fabrinet currently has a Value Score of D.

FN Stock Looks Pricey

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Shares of Fabrinet have surged more than 100% over the past year, significantly outperforming both the broader sector and the sectoral players like Microchip Technology and TE Connectivity. The company is gaining from the rapid growth in automation and AI, serving as a key manufacturing partner for advanced optical transceivers, high-performance computing (“HPC”) clusters and industrial lasers.

1-Year Price Performance Comparison

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

AI Boom Supporting FN’s Price Surge

Fabrinet is leveraged to expand demand across telecom/DCI, datacom and HPC. The company’s HPC program continues to grow, supported by increased automation and strong execution capabilities, while also creating opportunities to gain additional market share as a qualified secondary supplier.

Fabrinet’s advanced engineering expertise and proficiency in sub-micron alignment make it the contract manufacturer of choice for leading hyperscalers and networking companies. The company is well-positioned to support simultaneous growth across the telecom/DCI, datacom and HPC markets.

The demand for faster, more sophisticated and energy-efficient electronics is driving greater adoption of automation. Industry growth is being fueled by control systems, including computers, robotics and information technologies, that oversee a wide range of industrial processes and machinery. The rising use of collaborative robots, which enhance manufacturing efficiency by operating alongside human workers, is expected to further support this trend. In addition, IoT-enabled factory automation solutions are contributing to the industry's expansion.

Fabrinet projects fiscal fourth-quarter 2026 revenues between $1.25 billion and $1.29 billion, supported by strong performance in both its Optical Communications and non-optical communications segments.

Other Positives for FN

The company’s debt-free balance sheet further strengthens its financial flexibility. Fabrinet ended the third quarter of fiscal 2026 with $945.9 million in cash and cash equivalents and zero total debt, supporting ongoing capacity expansion.

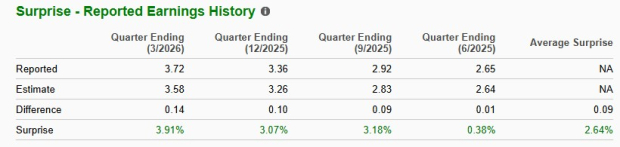

Fabrinet has an impressive earnings surprise history, as shown below.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Some Headwinds Remain

Datacom supply constraints remain a gating factor. Datacom revenues declined 6% sequentially in the fiscal third quarter, even as management stated that underlying demand exceeded what the company could ship.

Management described a broadening set of component and material shortages, citing lasers, memory and certain ASICs as constraints and expects the supply-demand imbalance to persist into the fiscal fourth quarter. While the company is expanding into hyperscaler-direct and merchant transceiver programs, sustained supply volatility can delay volume ramps and keep reported datacom revenues below demand. These constraints can also shift mix and utilization, creating variability in quarterly margins.

Fabrinet’s cost base is exposed to currency moves, and hedging can still leave residual earnings volatility. In the fiscal third quarter, the company recorded a $7 million foreign exchange revaluation gain, following a $3 million revaluation loss in the prior quarter, underscoring that these items can reverse quickly. As of March 27, 2026, management expected $8.9 million of losses in accumulated other comprehensive income to be reclassified into earnings within 12 months. Persistent currency volatility can hurt margins.

How to Play Fabrinet Stock Now

Fabrinet is well-positioned to benefit from the ongoing AI-driven expansion of digital infrastructure. Rising demand for AI-related optical and computing solutions, capacity expansion initiatives and new datacom program wins are expected to support the company’s continued growth trajectory. In addition, positive revisions to earnings estimates strengthen the investment case.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

However, risks related to datacom supply constraints and foreign exchange headwinds remain key concerns. Current market valuations appear to already reflect much of the anticipated growth. Investors are valuing Fabrinet not only on its present business performance but also on future potential, particularly the opportunities arising from AI-driven infrastructure investments. To justify its premium valuation, the company will likely need to execute exceptionally well and fully capitalize on the AI infrastructure buildout without significant setbacks.

Given the stock’s remarkable appreciation and the wide gap between current fundamentals and growth expectations, the risk-reward balance appears less attractive at current levels.

Accordingly, we believe existing shareholders should continue to hold FN stock. Prospective investors may be better served by waiting for a more favorable entry point. Fabrinet currently has a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).