Nvidia vs. Intel vs. TSMC: The American AI Ecosystem

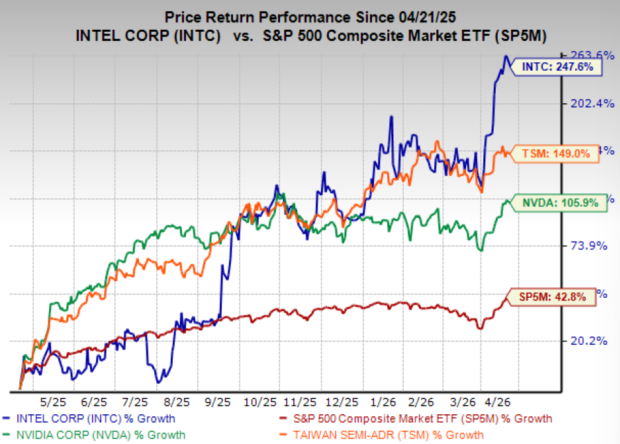

Nvidia (NVDA) may be the undisputed king of the AI boom and Taiwan Semiconductor (TSM) its key partner, but over the past year, Intel (INTC) has quietly delivered a superior stock performance. Shares of Intel have surged roughly 248% over the last 12 months, compared to a 149% gain for Taiwan Semiconductor, 106% gain for Nvidia and a 43% rise in the S&P 500.

At first glance, this divergence may raise the question of whether leadership in AI chips is starting to shift? But that isn’t the right question. What’s actually happening is far more important, as these companies appear to be evolving into complementary pillars of the American AI ecosystem, rather than direct competitors.

Nvidia carries a Zacks Rank #1 (Strong Buy) and Taiwan Semiconductor a Zacks Rank #2 (Buy), while Intel sits at a Zacks Rank #3 (Hold), reflecting the differences in execution certainty and turnaround potential. But all are increasingly critical to the same structural trend: the global buildout of AI infrastructure.

Image Source: Zacks Investment Research

Intel Shares Rally as Foundry Turnaround Gains Credibility

For years, Intel’s attempt to build a competitive foundry business looked like a costly misstep. The segment posted billions in cumulative losses through 2023–2025, and investors doubted whether the company could ever compete with TSMC.

That narrative is beginning to shift as Intel has ramped chipmaking equipment orders by more than 50% year-over-year to start 2026, signaling a meaningful acceleration in capacity buildout. Its 18A process node, which is producing leading edge 1.8nm chips has entered high-volume manufacturing at around 10,000 wafer starts per week, with yields steadily improving toward commercially viable levels.

More importantly, the upcoming 14A node represents a philosophical shift. Unlike prior generations, it is being designed from the ground up for external customers, incorporating next-generation technologies like RibbonFET and High-NA EUV lithography. Yields were estimated around 55% by mid-2025 and are likely in the 65–75% range entering 2026, tracking toward commercial competitiveness.

The new question is whether it can win meaningful external business and compete with the likes of foundry leader Taiwan Semiconductor. TSMC has of course been the majority producer of leading-edge chips necessary for the AI boom thus far, but diversifying and reshoring that ability is key to the broader AI expansion plans.

Though the price action in Intel stock had been choppy through the first three months of the year, it held up considerable better than the broad market and has been on an absolute tear over the last several weeks. The stock has broken out to new multi-year highs over the last two weeks, indicating significant buying from institutional investors.

Image Source: TradingView

Taiwan Semiconductor Constructing US Footprint

Domestic effort to reshore chip production has not been lost on Taiwan Semiconductor as they have also joined in on the effort. TSMC's Phase 1 fab (Fab 21) began production with a 4nm process in early 2025 at a rate of 10,000 wafers per month, with plans to scale to 30,000 wafers. Apple announced in February 2026 it would purchase more than 100 million chips manufactured at TSMC Arizona.

The second fab is planning to manufacture 3nm chips starting in 2027 and the third fab is expected to produce 2nm chips by 2028–2029. While it is currently behind Intel in current US production, its plans in the US are staggering. As of March 2025, planned investment increased by $100 billion from $65 billion to $165 billion, and the number of planned fabs grew from three to six, plus two advanced packaging lines and an R&D center.

And it may go even further with reports suggesting TSMC is now considering expanding to 12 fabs and four advanced packaging facilities in Arizona, as part of a broader $500 billion intergovernmental deal between the US and Taiwan.

Taiwan Semi stock has been among the best and most consistently performing stock of the AI leaders, thanks to it mission critical role in the buildout and powerful growth rates despite its mammoth size. Last week’s earnings report demonstrated the company’s continued dominance, with Q1 sales growing 40.6% in USD YoY and earnings 58.2%. That said, the geopolitical risks always lurk in the background, hence the efforts to reshore US production.

Nvidia, Intel and TSMC and the Division of Labor

Nvidia’s evolving relationship with Taiwan Semiconductor has been critical to the buildout thus far, but its emerging partnership with Intel may become even more so.

In early 2026, Nvidia made a $5 billion strategic investment in Intel, taking roughly a 4% stake. While Nvidia is not currently manufacturing its GPUs with Intel, the investment signals supply chain diversification.

Today, Nvidia is heavily reliant on Taiwan Semiconductor. That concentration creates geopolitical risk given Taiwan’s proximity to China.

Intel offers a potential domestic alternative. This dynamic highlights a broader shift in the semiconductor industry. Nvidia dominates chip design and AI compute architecture. Intel is working to reestablish itself as a leading-edge manufacturer on US soil.

Nvidia shares have languished for more than eight months as concerns about excessive AI capex, valuations and more recently, the conflict with Iran weighed on the stock. However, in the last couple of weeks, as the AI theme, broader market and Nvidia stock have seen a surge in momentum. NVDA just broke out from a huge technical consolidation, signaling what could be the start of the next leg higher.

Image Source: TradingView

Intel’s Opportunity in Advanced Packaging and Support

While attention has been focused on leading-edge fabrication, one immediate constraint in AI infrastructure may be advanced packaging, which is the process of integrating multiple chiplets into a single high-performance system.

This is where Intel has a real opportunity as its EMIB packaging technology is already being used by major customers and is reportedly being evaluated by companies like Amazon and Google for next-generation AI chips.

This creates a near-term example of their potential marriage in action. Nvidia may design the most advanced AI chips, but Intel could play a role in packaging and assembling those systems, or competing architectures, into deployable solutions.

With TSMC’s advanced packaging capacity largely sold out, this is a tangible opening for Intel to gain share.

Furthermore,the US government has taken a nearly 10% stake in the company and awarded it billions in contracts tied to secure semiconductor manufacturing. Intel is now effectively the only American firm with leading-edge fabrication capabilities on domestic soil.

This positions the company as a cornerstone of national industrial policy and gives it a notable advantage.

Intel Reports Earnings this Week

Intel reports earnings on April 23, and investors will be watching closely for updates on 18A yields, 14A customer pipelines, and overall foundry traction. Additional catalysts include potential partnership announcements at Computex and continued progress in winning external customers.

The AI buildout appears to have created a new structure in the semiconductor industry, one where design leadership and diversified manufacturing capability are distinct challenges that benefit from distinct players.

Nvidia remains the clear leader in AI compute and TSMC in fabrication, while Intel is working to reestablish itself as a critical manufacturing and infrastructure provider.

If Intel’s turnaround continues to gain traction, the most significant shift could be the emergence of a more resilient and diversified ecosystem, one where all companies play essential roles.

For investors, that may ultimately be the most important story.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).