Can Higher-Margin Businesses Fuel Further Earnings Growth at GFS?

GLOBALFOUNDRIES Inc.GFS is increasingly shifting its business toward higher-margin segments, a strategy that appears poised to support further earnings growth in the coming years. During the first-quarter 2026 earnings call, management highlighted strong momentum in silicon photonics, high-performance silicon germanium (SiGe), and technology services, all of which carry margins above the company average.

A key growth driver is the Communications Infrastructure & Data Center business, which posted 32% year-over-year revenue growth in the first quarter. Demand for silicon photonics solutions used in AI data centers and optical networking remains robust, while GF’s SiGe capacity is already oversubscribed through 2027. Management noted that these offerings are meaningfully margin accretive and are expected to contribute substantially to long-term revenue and profit expansion.

Another emerging earnings lever is Technology Services, which includes intellectual property, software, licensing and engineering services. This segment represented 13% of first-quarter revenues, exceeding expectations. The integration of MIPS and the pending acquisition of Synopsys’ ARC IP business are expected to increase the contribution from software and licensing revenues, which typically generate higher margins than traditional wafer manufacturing. Management expects Technology Services to become a larger share of revenue over time and views it as a durable source of high-quality growth.

The benefits of this mix shift are already visible. GFS delivered a first-quarter gross margin of 29%, up 510 basis points year over year, marking its strongest first-quarter margin performance on record. Management attributed much of the improvement to growth in higher-value businesses and expects continued profitability gains as these segments expand.

Given the accelerating demand for AI-related networking solutions and the growing contribution from technology services, higher-margin businesses appear well-positioned to fuel GFS’ next phase of earnings growth.

How Do Competitors Compare in High-Margin Growth Markets?

GLOBALFOUNDRIES is not alone in pursuing higher-margin opportunities tied to AI infrastructure and advanced connectivity. A notable competitor is United Microelectronics CorporationUMC, which operates in the mature-node foundry market and serves customers across communications, automotive and industrial applications. While UMC benefits from a diversified customer base, GFS has been more aggressive in expanding into silicon photonics, high-performance SiGe and AI-driven networking solutions, areas that offer stronger long-term margin potential.

Another relevant competitor is Semtech CorporationSMTC. Semtech has significant exposure to high-speed optical connectivity and data-center infrastructure through its networking and signal-integrity products. However, GFS participates earlier in the semiconductor value chain by manufacturing key silicon photonics and optical-networking components. As AI data-center investments accelerate, GFS’ growing mix of silicon photonics, technology services and licensing revenues could support stronger margin expansion and earnings growth relative to many industry peers.

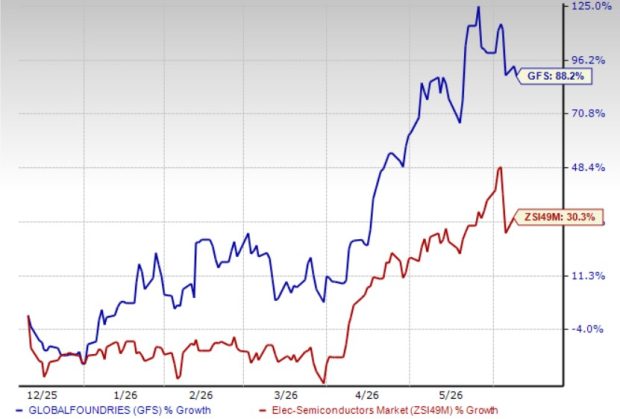

GFS’ Stock Price Performance & Valuation Trend

Shares of GlobalFoundries have surged 88.2% in the past six months, outperforming the Zacks Electronics - Semiconductors’ 30.3% growth.

Price Performance

Image Source: Zacks Investment Research

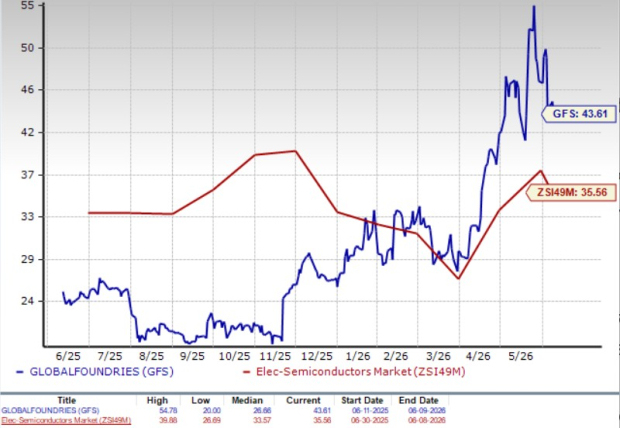

GFS stock is currently trading at a premium to its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 43.61, as shown in the chart below.

P/E (F12M)

Image Source: Zacks Investment Research

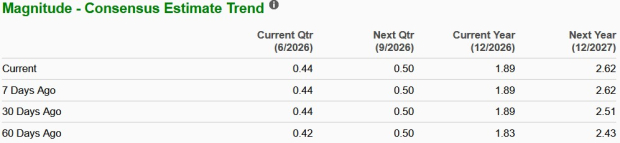

Earnings Estimate Revision of GFS

GFS’ earnings estimates for 2026 and 2027 have trended upward in the past 60 days to $1.89 and $2.62 per share, respectively. The revised estimates for 2026 and 2027 imply year-over-year growth of 9.9% and 38.6%, respectively.

Image Source: Zacks Investment Research

GFS currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpThis article originally published on Zacks Investment Research (zacks.com).