ASX Expects Over $3.5B in LEAP Revenues in 2026: Is More Growth Ahead?

ASE Technology Holding Co., Ltd.ASX appears increasingly confident about the trajectory of its Leading Edge Advanced Packaging (LEAP) business, raising its 2026 LEAP revenue outlook by 10% and now expecting the segment to generate more than $3.5 billion in revenues this year. The revised forecast reflects stronger-than-anticipated demand for advanced packaging and testing services tied to artificial intelligence (AI) applications.

Management noted that demand for LEAP services continues to exceed expectations, prompting the company to increase capital spending plans. ASE Technology is allocating an additional $600 million in machinery investments, with a significant portion earmarked for LEAP-related wafer sort capacity. The new equipment is expected to be deployed in the fourth quarter to support further capacity expansion in 2027.

The strength of the LEAP business was evident in first-quarter results. ASE Technology's ATM (Assembly, Testing and Materials) segment generated record revenues of NT$112.4 billion, up 30% year over year and 2% sequentially despite typical seasonal weakness. Management attributed the resilience largely to continued strength in LEAP services and traditional advanced packaging demand.

Importantly, management believes the current growth cycle may still be in its early stages. ASE Technology stated that it expects even stronger incremental LEAP revenue growth in 2027 than in 2026, citing robust customer demand and expanding opportunities across both advanced assembly and testing. The company also highlighted particularly strong momentum in wafer sort, which is becoming a key investment priority. ASX reported a first-quarter ATM gross margin of 26%, ahead of its original expectations, and expects margins to trend toward the upper end of its structural range as utilization improves and new capacity ramps.

With AI-related demand showing little sign of slowing and customers seeking additional advanced packaging capacity, ASE Technology's upgraded LEAP outlook suggests the company may still have another growth leg ahead. The combination of rising AI content, expanding customer engagements and significant capacity investments positions ASX to capitalize on what management describes as "very, very strong momentum" heading into 2027.

How ASX's AI Growth Story Compares With Rivals

Amkor Technology, Inc.AMKR and United Microelectronics CorporationUMC are also benefiting from AI-driven semiconductor demand, but through different parts of the value chain.

Amkor Technology is one of the world's leading outsourced semiconductor assembly and test providers and is seeing strong momentum from advanced packaging programs supporting AI and high-performance computing applications. In its first-quarter 2026 earnings call, management highlighted record quarterly revenues, growing demand across advanced packaging technologies and expanding engagements with leading chipmakers developing next-generation AI processors.

United Microelectronics occupies a different position in the semiconductor ecosystem as a specialty foundry focused on mature and specialty process technologies. While it is not a traditional packaging provider, management continues to see resilient demand across communications, industrial, consumer and AI-related applications. UMC is benefiting from strong momentum in its 22-nanometer platform, expanding its specialty technology portfolio and increasing customer engagements in emerging areas such as advanced packaging, silicon photonics and AI infrastructure solutions.

Both Amkor Technology and United Microelectronics remain well-positioned to benefit from the broader semiconductor upcycle. Nevertheless, ASE Technology's upgraded LEAP revenue outlook, aggressive capacity expansion plans and expectations for even stronger growth beyond 2026 suggest that it offers one of the most direct investment exposures to the accelerating demand for advanced AI packaging solutions.

ASX’s Price Performance, Valuation & Estimates

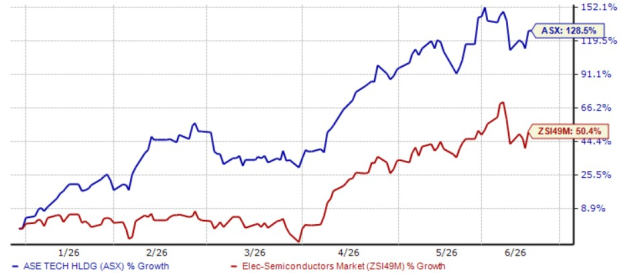

ASE Technology stock has surged a stellar 128.5% year to date (YTD) compared with the industry’s growth of 50.4%.

ASX’s YTD Price Performance

Image Source: Zacks Investment Research

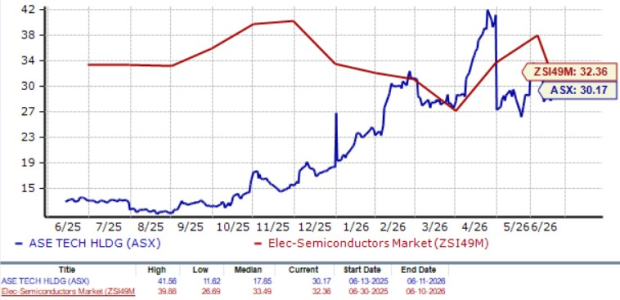

From a valuation standpoint, ASX stock trades at a forward price-to-earnings (P/E) multiple of 30.17, below the industry’s average of 32.36.

ASX’s P/E Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

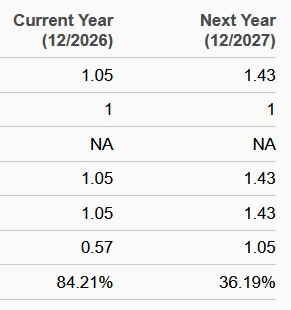

Over the past 60 days, the Zacks Consensus Estimate for ASE Technology’s 2026 earnings per share has increased to $1.05, as shown below. The estimated figure calls for 84.2% growth from 2025.

EPS Trend of ASX Stock

Image Source: Zacks Investment Research

ASX’s Zacks Rank

ASE Technology currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).