Delta Air Lines to Report Q1 Earnings: What's in the Offing?

Delta Air Lines DAL is scheduled to report first-quarter 2026 results on April 8, before the market opens.

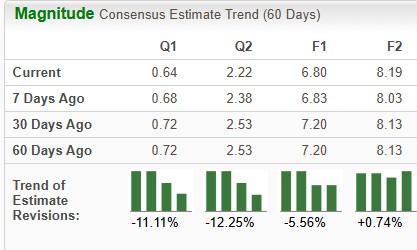

The Zacks Consensus Estimate for first-quarter 2026 earnings is pegged at 64 cents per share, indicating a 39.1% year-over-year increase. The measure has been revised 11.1% downward over the past 60 days. The same for revenues is pegged at $14.82 billion, indicating a 5.6% increase from the first-quarter 2025 actuals.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

For 2026, the Zacks Consensus Estimate for earnings is pegged at $6.8 per share, indicating a 16.8% year-over-year increase, and has been revised 5.6% downward over the past 60 days. The same for revenues is pegged at $66 billion, indicating a 4.1% increase from the first-quarter 2025 actuals.

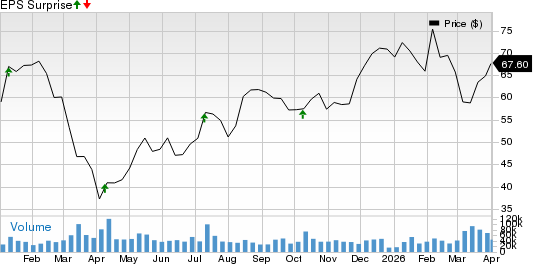

DAL has an impressive earnings surprise history, surpassing the Zacks Consensus Estimate in each of the trailing four quarters. The average beat is 7.9%.

Delta Air Lines Price and EPS Surprise

Delta Air Lines, Inc. price-eps-surprise | Delta Air Lines, Inc. Quote

Given this backdrop, let us examine the factors that might have influenced Delta Air Lines’ performance in the to-be-reported quarter.

We expect high fuel costs to have dented DAL’s bottom-line performance in the March quarter. The ongoing conflict in the Middle East has resulted in a sharp jump in oil prices. In the month of March alone, oil prices gained in excess of 50%. This has been naturally hurting the bottom line of airlines. This is because fuel expenses represent a key input cost for airlines. With most U.S. carriers having abandoned fuel hedging strategies, such an oil supply disruption has left them fully exposed to price spikes. However, Delta's refinery in Pennsylvania gives it some protection in this regard.

High labor costs are also likely to have hurt the bottom line. The Zacks Consensus Estimate for non-fuel unit cost or cost per available seat mile (CASM: adjusted) is pegged at 14.37 cents compared with 14.27 cents reported in the fourth quarter of 2025.

Despite the sharp rise in jet fuel, strong bookings are likely to have aided DAL’s top-line performance in the March quarter. The increasing ticket prices are likely to have covered the double-digit increase in airlines’ key input costs. Driven by strong consumer and corporate demand, which accelerated in March, Delta raised its first-quarter revenue forecast. The Atlanta-based company, encouraged by improving sales, reflecting all-around demand strength, expects first-quarter revenues to grow at a high-single-digit percentage compared with its earlier forecast of 5% to 7%. Total revenues are projected to be in the $15-$15.3 billion band.

What Our Model Says About DAL

Our proven model does not conclusively predict an earnings beat for Delta Air Lines this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. This is not the case here.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Delta Air Lines has an Earnings ESP of -7.20% and a Zacks Rank #3.

Highlights of DAL’s Q4 Earnings

Delta reported fourth-quarter 2025 earnings (excluding 31 cents from non-recurring items) of $1.55 per share, which beat the Zacks Consensus Estimate of $1.53. Earnings decreased 16.2% on a year-over-year basis due to high labor costs.

Revenues in the December-end quarter were $16 billion, beating the Zacks Consensus Estimate of $15.63 billion and increasing 2.9% on a year-over-year basis. Adjusted operating revenues (excluding third-party refinery sales) increased 1.2% year over year to $14.6 billion. Revenue growth was impacted by about 2 points due to the government shutdown

Stocks to Consider

Here are a few stocks from the broader Zacks Transportation sector that investors may consider, as our model shows that these have the right combination of elements to beat on earnings this reporting cycle.

J.B. Hunt Transport Services JBHT has an Earnings ESP of +1.15% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

JBHT is scheduled to report first-quarter 2026 earnings on April 15. The Zacks Consensus Estimate for first-quarter 2026 earnings has been revised 1.4% downward over the past 60 days. JBHT’s earnings beat the Zacks Consensus Estimate in three of the preceding four quarters and missed in the remaining one, the average beat being 6.1%.

Union Pacific UNP has an Earnings ESP of +1.20% and a Zacks Rank #3 at present. UNP is scheduled to report first-quarter 2026 earnings on April 23.

The Zacks Consensus Estimate for first-quarter 2026 earnings has been revised 1.4% downward over the past 60 days. UNP’s earnings beat the Zacks Consensus Estimate in two of the preceding four quarters (missing the mark on the other occasions). The average beat is 1.3%.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeThis article originally published on Zacks Investment Research (zacks.com).