URBN vs. ANF: Which Retail Giant Stock Should Investors Choose?

Urban Outfitters, Inc. URBN and Abercrombie & Fitch Co.ANF are two of the most influential specialty apparel retailers competing for market share in the global fashion and lifestyle industry.

While Urban Outfitters has built a diversified portfolio spanning Urban Outfitters, Anthropologie, Free People, FP Movement and the fast-growing Nuuly rental platform, Abercrombie has transformed itself into a modern lifestyle retailer led by the Abercrombie and Hollister brands. Both companies generate the majority of their revenues through direct-to-consumer channels while leveraging physical stores, digital commerce and omnichannel capabilities to strengthen customer engagement.

The comparison between URBN and ANF is especially compelling as both retailers continue gaining market share in an otherwise highly competitive apparel industry through differentiated brand portfolios, digital innovation and disciplined inventory management. Although they target overlapping fashion-conscious consumers, their strategies differ meaningfully. Urban Outfitters relies on a multi-brand ecosystem serving diverse demographics and lifestyle categories, while Abercrombie focuses on elevating two global brands through premium positioning and international expansion.

Let us dive into the two companies’ key statistics, market share, valuation, dividend strategies and stock performances to determine which is better positioned for growth in 2026.

The Case for URBN

Urban Outfitters' biggest competitive strength lies in its highly diversified business model, which continues to deliver consistent growth across multiple brands and channels. Unlike many specialty retailers that rely on a single banner, the company generates revenues through Urban Outfitters, Anthropologie, Free People, FP Movement, its wholesale operations and the rapidly expanding Nuuly subscription platform. This diversified portfolio helped URBN post its seventh consecutive quarter of record sales and earnings, with first-quarter revenues rising 11% year over year to a record $1.5 billion.

Every retail brand reported positive comparable sales, while four of five brands generated record first-quarter revenues. Nuuly's 35% revenue growth and wholesale revenue growth of 25% further demonstrate that URBN's growth engine extends well beyond traditional retail, reducing dependence on any single fashion cycle and allowing the company to consistently capture market share across multiple consumer segments. Management believes this diversification remains one of the company's strongest competitive advantages.

Another key strength is URBN's ability to grow brands while preserving their unique identities. Free People continues to post industry-leading momentum, FP Movement is rapidly emerging as a differentiated activewear brand, Anthropologie has now delivered more than five years of positive comparable sales, and Urban Outfitters itself is regaining momentum in both North America and Europe. The Urban Outfitters brand generated 9% comparable sales growth globally, driven by double-digit new customer acquisition, strong full-price selling and successful marketing initiatives. Management also highlighted that the European business continues to gain meaningful market share despite a weak regional retail backdrop, reflecting the strength of its merchandise assortment and brand positioning.

Technology and disciplined capital allocation further strengthen URBN's long-term investment case. The company continues to invest aggressively in artificial intelligence across merchandising, personalization, logistics, product development, fraud prevention and customer service to improve productivity and accelerate decision-making. AI-powered recommendation engines, search capabilities and automated customer support are already enhancing the customer experience, while technology investments are expected to shorten product development cycles and improve inventory productivity over time.

The Case for ANF

Abercrombie continues to benefit from one of the strongest brand transformations in the specialty apparel industry. The company delivered its 14th consecutive quarter of revenue growth and another record first quarter despite geopolitical disruptions in parts of Europe and the Middle East. Revenues increased to $1.1 billion, while operating income and earnings per share exceeded expectations. Growth remained broad-based across the Americas and APAC, supported by healthy customer traffic, stable conversion rates and continued pricing power. Management emphasized that both Abercrombie and Hollister continue to resonate with their respective target customers, allowing the company to maintain positive average unit retail growth while controlling promotional activity. This disciplined operating model has enabled ANF to consistently deliver profitable growth even in a volatile retail environment.

The company's two-brand strategy continues to strengthen its competitive positioning. Abercrombie has successfully evolved into an elevated lifestyle brand serving millennials and older Gen Z consumers, while Hollister maintains strong relevance among teens through fashion-forward assortments and culturally relevant marketing campaigns. Product innovation, strategic collaborations with brands such as Sperry and Kappa, expansion into categories like Abercrombie Baby & Toddler, and continued investment in larger-format stores provide multiple avenues for incremental growth.

ANF is also building a stronger long-term foundation through digital transformation and disciplined capital allocation. During the quarter, the company successfully completed its multi-year merchandising ERP implementation, creating a modern technology platform that supports faster product development, global partnerships and future channel expansion. Artificial intelligence is increasingly being embedded across forecasting, inventory planning, customer service and digital commerce to improve efficiency and enhance customer engagement.

How Does the Zacks Consensus Estimate Compare for URBN & ANF?

The Zacks Consensus Estimate for Urban Outfitters’ fiscal 2027 earnings implies year-over-year growth of 10.5%, whereas the same for fiscal 2028 indicates an uptick of 9.9%. Estimates for fiscal 2027 and 2028 have been revised upward by 0.7% and 0.8%, respectively, in the past 30 days.

EPS Estimate Trend of URBN

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Abercrombie’s fiscal 2026 and 2027 EPS suggests year-over-year growth of 7.7% and 10%, respectively. The EPS estimates have moved down by a penny to $10.62 in the past 30 days, whereas for 2027, the estimates have moved down by 10 cents to $11.69.

EPS Estimate Trend of ANF

Image Source: Zacks Investment Research

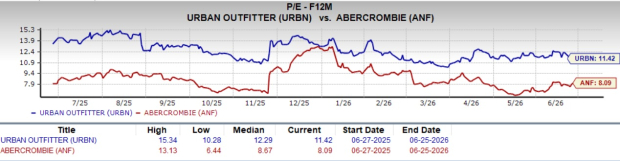

Price Performance & Valuation of URBN & ANF

URBN currently trades at a forward 12-month P/E ratio of 11.42X, below the Zacks Retail – Apparel and Shoes industry average of 15.14X, suggesting the stock remains reasonably valued despite its strong operating momentum. ANF, meanwhile, trades at a lower forward P/E of 8.09x, which may appeal to value-oriented investors but also indicates the market is assigning a greater degree of uncertainty to its earnings outlook amid regional headwinds and a more concentrated two-brand portfolio.

While both retailers appear attractively valued relative to the industry average, URBN's premium to ANF is supported by its broader portfolio diversification, multiple growth engines across retail, wholesale and subscription, and a longer runway for margin expansion and international growth.

Image Source: Zacks Investment Research

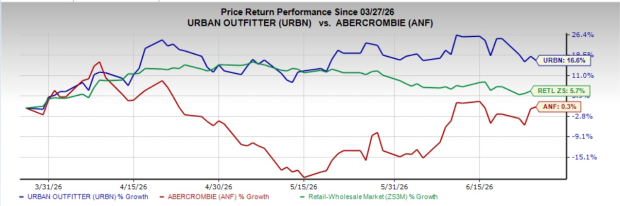

This positive fundamental outlook is also reflected in recent share price performance. URBN stock has gained 16.6% over the past three months, comfortably outperforming ANF's modest 0.3% rise as well as the industry's 5.7% gain. The outperformance underscores investors' confidence in Urban Outfitters' diversified growth strategy, record operating performance, expanding market share across multiple brands and continued investments in digital capabilities, AI and its fast-growing Nuuly subscription business. By comparison, Abercrombie's muted stock performance suggests investors remain more cautious despite the company's healthy fundamentals, as it continues to navigate regional headwinds in EMEA and execute on growth initiatives across its two-brand portfolio.

Image Source: Zacks Investment Research

The Verdict

Both Urban Outfitters and Abercrombie remain fundamentally strong specialty apparel retailers with compelling long-term growth opportunities. Abercrombie has executed an impressive brand transformation, continues to deliver consistent sales growth and is investing in digital capabilities and international expansion. However, Urban Outfitters stands out with its broader and more diversified portfolio, multiple growth engines across retail, wholesale and subscription, accelerating AI initiatives and stronger earnings momentum. The company has also demonstrated superior stock performance, upward earnings estimate revisions and greater resilience through its multi-brand strategy.

URBN currently carries a Zacks Rank #2 (Buy), whereas ANF has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).