Can Omnichannel Investments Strengthen Dillard's Position?

Dillard's, Inc.DDS has been strengthening its retail position by complementing its physical store network with its digital platform, allowing customers to shop seamlessly across channels. The company’s continued emphasis on merchandising newness, expanding its store footprint and maintaining an established online presence at dillards.com suggests that omnichannel capabilities remain integral to its customer engagement strategy. DDS operates 272 stores across 30 states, alongside its Internet store, providing broad market coverage and multiple shopping touchpoints.

The benefits of this integrated approach are reflected in the first-quarter fiscal 2026 operating results. Total retail sales increased 3%, while comparable-store sales also rose 3%, indicating healthy consumer demand across the business. Notably, every merchandise category posted year-over-year sales gains, with home and furniture, ladies' accessories and lingerie, and shoes delivering the strongest growth. A broader omnichannel presence can help Dillard's showcase these categories more effectively, improve product availability and create a more convenient shopping experience for customers.

Dillard's also continues to invest in its physical network, opening a new 160,000-square-foot store in Beavercreek, OH, in the quarter. Rather than viewing stores and digital channels separately, the company appears positioned to leverage both as complementary assets. Coupled with management's continued focus on refreshing merchandise assortments, this strategy contributed to a higher retail gross margin of 45.8% and profitable sales growth in the fiscal first quarter.

Dillard's combination of an established online platform, nationwide store network and merchandise-led strategy provides a solid foundation to strengthen customer engagement and support long-term competitive positioning.

DDS’s Zacks Rank, Valuation & Share Price Performance

Shares of this Zacks Rank #1 (Strong Buy) company have gained 20.1% in the past year, underperforming the industry and S&P 500’s growth of 47% and 24.1%, respectively. The stock has outpaced the broader Retail-Wholesale sector’s return of 1.8%.

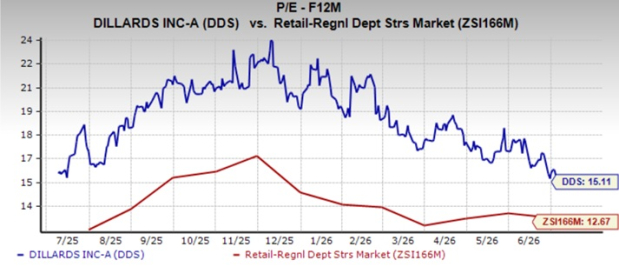

DDS Stock's 3-Month Performance

Image Source: Zacks Investment Research

From a valuation standpoint, DDS trades at a forward price-to-earnings ratio of 15.11X, higher than the industry’s average of 12.67X.

Image Source: Zacks Investment Research

Other Stocks to Consider

Genesco Inc. GCO is a specialty retail and branded company that sells footwear and accessories in retail stores throughout the United States, Canada, the U.K. and the Republic of Ireland. The company currently flaunts a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

GCO delivered a trailing four-quarter earnings surprise of 3.8%, on average. The Zacks Consensus Estimate for Genesco’s current financial-year EPS indicates growth of 55.2% from the year-ago reported number.

Tilly's Inc.TLYS is a specialty retailer in the action sports industry, selling clothing, shoes and accessories. The company currently sports a Zacks Rank #1.

TLYS delivered a trailing four-quarter earnings surprise of 155.3%, on average. The Zacks Consensus Estimate for Tilly's current financial-year sales and EPS indicates growth of 4.9% and 89.7%, respectively, from the year-ago reported numbers.

Urban Outfitters Inc. URBN is a lifestyle products and services company that sells fashion apparel, accessories, footwear, home goods and related offerings through a portfolio of global consumer brands. The company currently flaunts a Zacks Rank of 1.

The Zacks Consensus Estimate for Urban Outfitters’ current financial-year sales and EPS is expected to rise 8.8% and 11.8%, respectively, from the year-ago reported figures. URBN delivered a trailing four-quarter earnings surprise of 12.2%, on average.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).