Can Western Digital's Strong Cash Flow Outweigh its Leverage Concerns?

Western Digital CorporationWDC is benefiting from booming AI-led demand and deeper customer commitments through long-term contracts. The company’s solid demand trends, improved execution and disciplined cost management are supporting its overall operating performance. These factors are helping drive revenue and margin expansion and reinforce its competitive positioning in a dynamic storage market.

The company’s key financial strength lies in its consistent and improving cash flow generation. In the second quarter of fiscal 2026, cash generated from operations rose sharply to $745 million from $403 million in the prior-year period, while free cash flow surged 95% to $653 million. This robust performance highlights the company’s ability to convert earnings into cash efficiently, providing flexibility in capital allocation.

Western Digital has demonstrated a clear commitment to returning value to shareholders. It declared a cash dividend of 12.5 cents per share and, along with share repurchases, returned more than 100% of its free cash flow during the fiscal second quarter. Since initiating its capital return program, it has distributed $1.4 billion through buybacks and dividends, reflecting confidence in its cash-generation capabilities and financial stability.

However, despite strong operations, the company still faces concerns due to high debt and a stretched balance sheet. As of early January 2026, Western Digital held $2 billion in cash and cash equivalents against $4.7 billion in long-term debt. This elevated leverage level could limit its financial flexibility, particularly when it comes to pursuing acquisitions or funding additional growth initiatives. The company must consistently generate strong cash flows to comfortably meet its debt obligations, making it vulnerable to any potential downturn in demand or execution. Although Western Digital’s strong and improving cash flow provides a solid foundation and supports shareholder returns, its high leverage remains a notable concern.

How WDC’s Competitors are Placed on Leverage & Liquidity

Seagate Technology Holdings plcSTX generates strong cash flow, supporting investments in innovation, acquisitions and growth while returning capital through dividends and buybacks. In fiscal 2025, it reduced debt by $684 million, highlighting balanced capital allocation. In second-quarter fiscal 2026, it delivered $723 million in operating cash flow and $607 million in free cash flow, returning $154 million via dividends and repaying $500 million in debt. However, leverage remains elevated, with $1.05 billion in cash versus $4.5 billion in long-term debt and a high debt-to-capital ratio. This may pressure financial flexibility despite solid cash generation and growth prospects.

NetApp NTAP cash and cash equivalents were $3 billion as of Jan. 23, 2026. Its long-term debt was $2.49 billion. Net cash from operations was $317 million, while free cash flow was $271 million (free cash flow margin of 15.8%). Net cash balance provides the required flexibility to pursue any growth strategy, whether through acquisitions or otherwise. A strong balance sheet helps NetApp continue its shareholder-friendly initiatives of dividend payouts. The company returned $303 million to its shareholders as dividend payouts and share repurchases in the fiscal third quarter. NetApp returned $200 million to its shareholders through share repurchases and distributed $103 million in dividends. The company returned $1.57 billion to its shareholders as dividend payouts and share repurchases in fiscal 2025. NetApp’s ability to generate solid free cash flow is expected to help it sustain the current dividend payout (0.35) level, at least in the near term.

WDC Price Performance, Valuation and Estimates

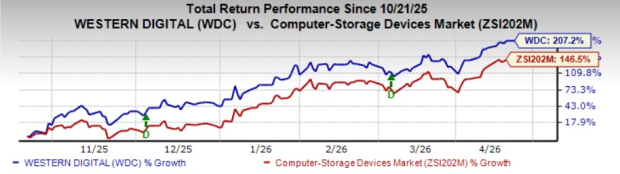

In the past six months, shares of WDC have surged 207.2% compared with the Zacks Computer-Storage Devices industry’s growth of 146.5%.

Image Source: Zacks Investment Research

In terms of forward price/earnings, WDC shares are trading at 29.18X, higher than the industry’s 15.35X.

Image Source: Zacks Investment Research

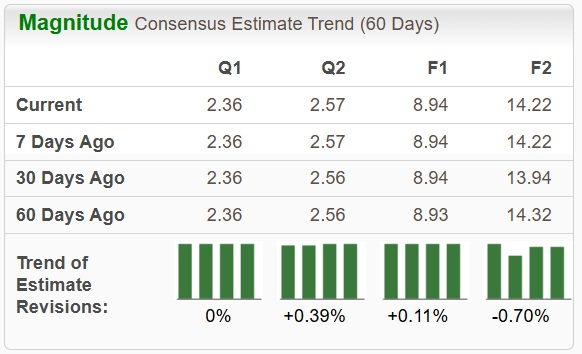

The Zacks Consensus Estimate for WDC’s earnings for fiscal 2026 has been revised marginally upward over the past 60 days.

Image Source: Zacks Investment Research

Currently, Western Digital has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).