What's Fueling Citigroup's Robust Capital Return Strategy?

Citigroup Inc.’s C capital return strategy, centered on dividends and large-scale share buybacks, is fueled by a combination of strong earnings power, excess capital buffers and disciplined balance sheet management.

In the first quarter of 2026, C revenues rose roughly 14% year over year, making it the company’s highest quarterly revenues in a decade. The results underscore the strength of its diversified business model and the progress of its strategic repositioning. Also, C ended the first quarter of 2026 with a CET1 ratio of 12.7%, about 110 basis points above its regulatory capital requirement, providing a sizable buffer. This gives the bank ample internal capital to distribute without weakening its financial position.

The company has an efficient share repurchase plan in place. In January 2025, Citigroup's board of directors approved a $20-billion common stock repurchase program with no expiration date. In the first quarter of 2026 alone, the bank repurchased $6.3 billion of common stock. As of March 31, 2026, $0.5 billion worth of authorization remained available.

During the 2026 Investor Day presentation held on May 7, the company highlighted that its capital allocation priorities include investing in growth, maintaining dividends in line with shareholder expectations, preparing for different macroeconomic and regulatory scenarios, and returning excess capital through buybacks. The company also noted that its board authorized a $30-billion multi-year common stock repurchase program, expected to begin in the second quarter of 2026.

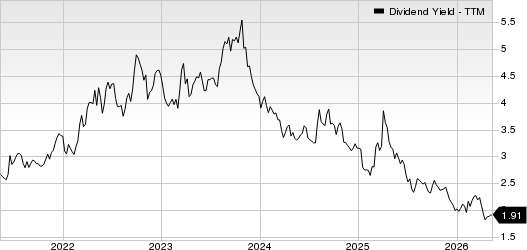

Alongside buybacks, Citigroup continues to deliver consistent dividend payouts. Post-clearing the 2025 Fed stress test, the company hiked its dividend 7.1% to 60 cents per share. In the past five years, C raised its dividends three times. It currently has a payout ratio of 26%. It has a dividend yield of 1.91%.

Citigroup Inc. Dividend Yield (TTM)

As of March 31, 2026, Citigroup’s cash and due from banks and total investments aggregated to $467.8 billion, higher than its total debt (short-term and long-term borrowing) of $379.6 billion. Thus, given its strong capital position, decent liquiidty and earnings strength, C is expected to sustain improved capital distributions in the future, thereby continuing to enhance shareholder value.

How Do C Peers Maintain Disciplined Capital Distribution?

Similar to Citigroup, its peers PNC FinancialPNC and Wells FargoWFC have impressive capital distribution plans.

After clearing the 2025 Federal Reserve stress test, PNC Financial hiked quarterly cash dividends on common stock by 6% to $1.70 per share. Apart from regular dividend hikes, the company has a share repurchase program in place. As of March 31, 2026, the company had remaining authority to repurchase up to nearly 32 million common shares. Given PNC Financial’s earnings and liquidity strength, its capital-distribution activities seem sustainable and are likely to stoke investors’ confidence in the stock.

Similarly, post clearing the Federal Reserve’s 2025 stress test, Wells Fargo raised its common stock dividend 12.5% in July 2025 to 45 cents per share. The company also has a share repurchase program in place. As of March 31, 2026, the company had remaining authority to repurchase up to $25.7 billion of common stock. Given its robust capital position and ample liquidity, Wells Fargo’s capital-deployment activities seem sustainable and will boost investor confidence in the stock.

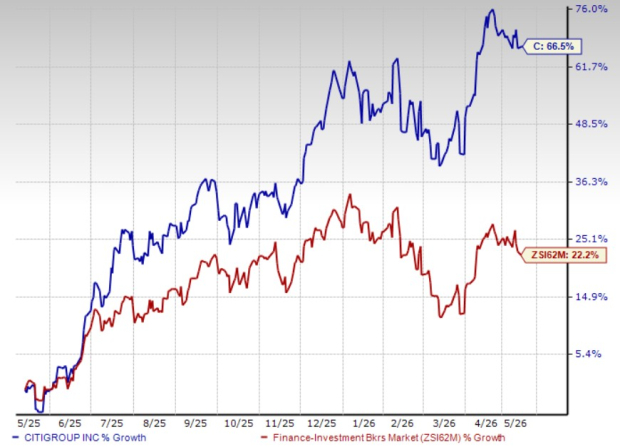

C’s Price Performance, Valuation & Estimates

Shares of Citigroup have surged 66.5% in the past year compared with the industry’s growth of 22.2%.

Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, C trades at a forward price-to-earnings (P/E) ratio of 11.16X, below the industry’s average of 12.69X.

Price-to-Earnings F12M

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for C’s 2026 and 2027 earnings implies year-over-year rallies of 33.6% and 16.4%, respectively. Estimates for both years have been revised upward over the past 30 days.

Estimate Revision Trend

Image Source: Zacks Investment Research

Citigroup currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).