Wells Fargo Revenues Are Rising, But Can It Bend the Cost Curve?

Wells Fargo & Company’s WFC revenue growth has become challenging over the past few years. Revenues witnessed a negative CAGR of 0.3% over the last six years (2019-2025) due to elevated funding costs during the period, which weighed on net interest income (NII) growth. However, the first-quarter 2026 results showed that the trend has reversed and the bank is gaining revenue momentum, but expense control remains a key test for its turnaround story.

Total revenues rose 6% year over year to $21.4 billion, supported by a 5% increase in NII and an 8% rise in non-interest income. The improvement reflected higher loan and deposit balances, lower deposit costs, stronger Markets results and higher asset-based fees in Wealth and Investment Management.

The bigger question is whether Wells Fargo can convert revenue growth into stronger operating leverage. On that front, the results were mixed but encouraging. Non-interest expenses increased 3% year over year to $14.3 billion, slower than the pace of revenue growth. That helped pre-tax pre-provision profit rise 14% and improved the efficiency ratio to 67% from 69% a year earlier. Still, the cost curve has not fully bent. Year over year, personnel expenses increased as higher revenue-related compensation, especially in Wealth and Investment Management, offset some benefits from efficiency initiatives. Non-personnel expenses also rose due to higher advertising, technology and equipment costs.

The underlying efficiency story, however, remains intact. The company has been actively engaging in cost-cutting measures, including the streamlining of its organizational structure, closure of branches and the reduction in headcount. In the first quarter of 2026, Wells Fargo’s headcount fell to 201,000 from 215,000 a year earlier, marking 23 consecutive quarters of reductions. Also, WFC has become more deliberate in its branch location strategy, as the number of branches declined 1.5% year over year to 4,093 at the end of the first quarter of 2026.

Management’s outlook suggests discipline will remain a priority. Wells Fargo maintained its 2026 non-interest expense guidance at $55.7 billion, suggesting rise from the $54.8 billion recorded in 2025, as it continues investing in technology and strategic initiatives.

For investors, the takeaway remains balanced. While Wells Fargo is benefiting from positive operating leverage, rising compensation, technology and regulatory-related expenses could constrain near-term margin improvement. The bank is making progress in controlling costs, though the pace of improvement remains gradual.

How WFC’s Peers Are Performing?

Citigroup, Inc.C reported first-quarter 2026 revenues of $24.6 billion, up roughly 14% year over year, making it the company’s highest quarterly revenues in a decade. The results underscore the strength of its diversified business model and the progress of its strategic repositioning. However, C’s operating expenses in first-quarter 2026 rose 7% year over year, with severance also contributing as the firm continues headcount actions and delayering.

Looking ahead, with continued momentum in core businesses, rising NII and fee income, and ongoing restructuring efforts, Citigroup expects revenues to see a 4-5% compound annual growth rate through 2026.

PNC Financial’s PNC first-quarter 2026 total revenues of $6.2 billion rose 13% year over year. The increase was driven by growth in non-interest income and NII. Also, non-interest expenses increased 11.2% year over year due to FirstBank’s operating and integration expenses, increased business activity and continued investments to support growth.

Looking forward, PNC Financial's rising NII and fee income, along with the January 2026 acquisition of FirstBank Holding Company, will drive growth. PNC’s management expects 2026 revenues to rise 11% from the 2025 reported level.

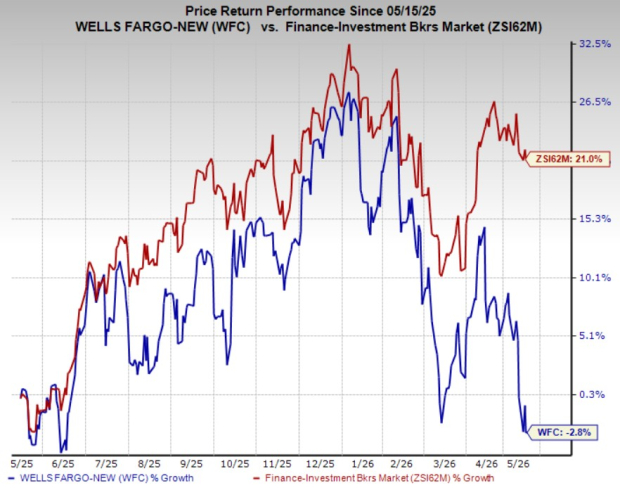

Wells Fargo’s Price Performance & Zacks Rank

WFC shares have declined 2.8% in the past year against the industry’s growth of 21%.

Image Source: Zacks Investment Research

Wells Fargo currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>This article originally published on Zacks Investment Research (zacks.com).