Everpure Jumps 34% in a Year: Should Investors Bet on the Stock?

Everpure P stock has gained 33.9%, outperforming the industry’s 10.4% return and the Zacks S&P 500 Composite's 27.6% rise.

Over the past year, the company has outpaced its close competitors, XylemXYL and DanaherDHR. Xylem's shares have plunged 13.6% and Danaher's share price has decreased 8.8%.

1-Year Share Price Performance

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Even over the past three months, Everpure's share price has increased 20.8%, while Danaher and Xylem have declined 5.8% and 10.4%, respectively.

Considering this impressive rally, let us analyze further to determine whether investors should add Everpure to their portfolios.

P’s Subscription Momentum Raises Future Revenue Visibility

During the first quarter of fiscal 2027, Everpure registered 17% year-over-year growth in its subscription revenues. On a similar note, subscription annual recurring revenues grew 19% year over year, with remaining performance obligation registering a 41% jump. It is a clear double green light since it indicates that the company expects guaranteed income right now, as well as secured a pipeline of income for the future. Therefore, the company’s subscription momentum highlights a structural pivot that can draw in highly predictable and recurring revenue streams.

Long-term investors might consider this shift highly beneficial. It replaces dynamic sales with stable recurring cash flows, which protects Everpure’s financial health during economic setbacks. High revenue visibility reduces investment risks, optimizes capital efficiency and fuels enterprise valuation.

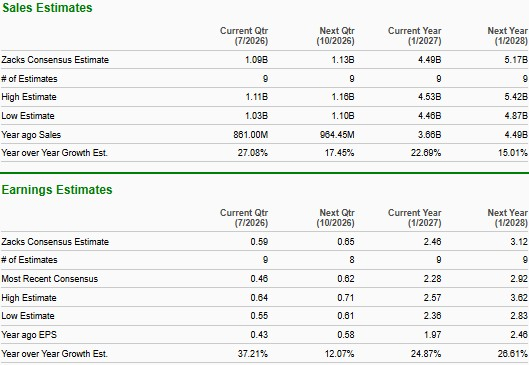

Everpure Trades Higher Than Industry: A Deserved Premium

The P stock is currently trading at a forward 12-month price-to-earnings (P/E) multiple of 28.58X and holds a P/E-to-growth (PEG) ratio of 1.48. While traditional metrics flag the stock as overvalued relative to the industry’s P/E multiple of 22.31X and PEG ratio of 1.15, the premium is fully justified when we consider the lofty 53.2% return on equity Everpure delivers to its shareholders, which exceeds the industry’s 12.2%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The company does not pay out any dividends, retaining 100% of its net income. Hence, reinvesting every dollar of earnings at a 53.2% internal rate of return fuels the company’s growth engine that allows it to move ahead of its peers easily.

Considering the P/E and PEG ratios, we find that the earnings growth rate of the company and the industry is close to 19.3%. While the expected growth rate is the same for Everpure and the industry, the company needs a mere fraction of its CapEx to hit that target, which will free up a hefty cash flow.

The capital-light scalability of Everpure’s business serves as an economic moat, providing a strong margin of safety during market volatility and superior earnings quality. Therefore, paying a substantial premium for Everpure’s stock is a rational trade-off to invest in a business that raises shareholder value at a faster pace.

P’s Bright Top & Bottom-Line Prospects

The Zacks Consensus Estimate for fiscal 2027 revenues is pegged at $4.5 billion, suggesting 22.7% growth from the year-ago quarter’s actual. For fiscal 2028, it is anticipated to gain 15% year over year. For earnings, the consensus estimate for fiscal 2027 is pegged at $2.46 per share, suggesting a 24.9% rise from the year-ago quarter’s actual. For fiscal 2028, it is expected to jump 26.6%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Over the past 30 days, two EPS estimates for fiscal 2027 and 2028 have been revised upward with no downward adjustments, highlighting optimistic sentiments among analysts. In the same period, the Zacks Consensus Estimate for fiscal 2027 and 2028 earnings per share moved up 1.3% and 1.7%, respectively.

Everpure: Initiate an Immediate Buy

The P stock is a compelling buy due to its financial health, shift to recurring revenues and solid capital returns. Double-digit growth in subscription revenues, combined with metrics indicating certainty in future revenues, should raise top-line visibility for investors that aids them in ascertaining profitability.

Despite trading at a premium, Everpure’s valuation is completely justified due to its strong capital return, dramatically outpacing the industry figure. The company can easily reinvest all of its earnings at an elite rate, providing a bedrock for the scalability of the company’s capital-light model.

A strong top and bottom-line outlook, coupled with optimistic analyst sentiment, is a major green flag for investors as it solidifies Everpure’s growth trajectory. A mix of economic moat, high earnings quality and shareholder value creation positions Everpure as a premium stock that investors should find worthwhile adding to their portfolio.

Everpure has a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).