Can Opendoor Scale Acquisitions While Maintaining Capital Discipline?

Opendoor TechnologiesOPEN is showing increasing confidence that it can grow acquisition volumes while maintaining the financial discipline needed to achieve profitability. The company’s first-quarter 2026 earnings call highlighted significant progress on both fronts, suggesting that its revamped operating model is beginning to deliver results.

A key indicator is the sharp increase in acquisition activity. Opendoor entered into contracts on more than 5,000 homes during the quarter, its strongest performance since 2022, while home purchases rose 45% sequentially to 2,474 properties. Management noted that this growth is not being fueled by aggressive pricing but by improved underwriting, better customer conversion and new offerings such as cash now, more later.

Just as important, the company appears determined to avoid the capital-intensive mistakes of the past. Opendoor ended the quarter with $999 million in unrestricted cash and emphasized that inventory growth has been accompanied by improving inventory quality and faster resale velocity. Homes on the market for more than 120 days declined to 10% from 51% two quarters earlier, reducing holding costs and improving capital efficiency.

Management also stressed that growth will be supported by existing liquidity and financing capacity rather than by dilutive equity raises. The company has $7.1 billion of non-recourse borrowing capacity available, providing ample room to fund acquisitions while preserving shareholder value.

With contribution margins improving for six straight months and adjusted EBITDA expected to reach break-even in the second quarter, Opendoor believes it can continue to scale acquisitions while remaining disciplined. If these trends persist, the company may be positioned to achieve profitable growth even in a challenging housing market.

Rivals Are Also Pursuing Growth With Financial Discipline

Opendoor operates in a competitive real estate technology market where balancing growth and capital efficiency remains a key challenge. Two notable peers in this space are Offerpad SolutionsOPAD and Zillow GroupZG.

Offerpad Solutions, another iBuyer-focused company, has adopted a cautious growth strategy following the housing market slowdown. Like Opendoor, Offerpad Solutions has prioritized inventory quality, disciplined home acquisitions and faster inventory turnover to reduce market risk. The company continues to focus on improving unit economics and preserving liquidity rather than pursuing growth at any cost, reflecting a similar emphasis on capital discipline.

Meanwhile, Zillow Group has taken a different approach after shutting down its Zillow Offers home-flipping business in 2021. Instead of owning large inventories of homes, Zillow Group is expanding its asset-light housing ecosystem through services such as mortgages, touring, seller solutions and transaction facilitation. This strategy allows Zillow Group to benefit from housing-market activity while minimizing balance-sheet risk and capital requirements.

While their business models differ, both competitors highlight the industry's broader shift toward profitable growth, operational efficiency and prudent capital allocation.

OPEN’s Stock Price Performance, Valuation & Estimates

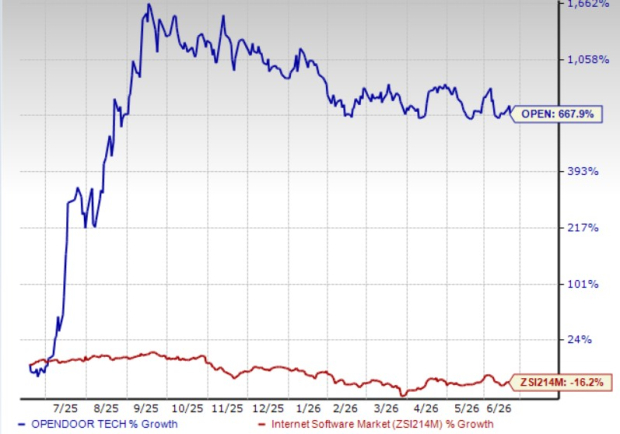

Shares of Opendoor have skyrocketed 667.9% in the past year against the industry’s 16.2% decline.

OPEN One-Year Price Performance

Image Source: Zacks Investment Research

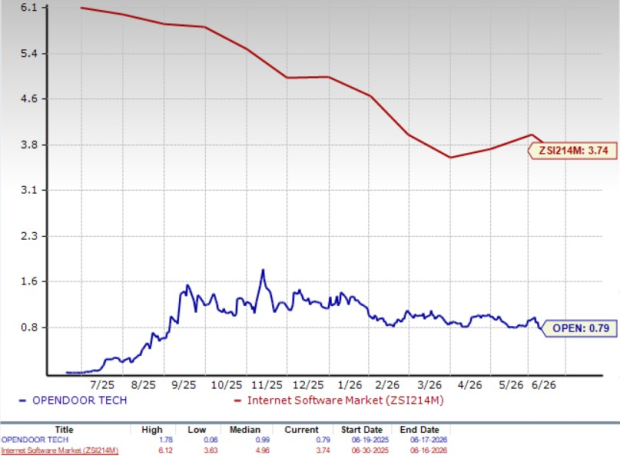

From a valuation standpoint, OPEN trades at a forward price-to-sales (P/S) multiple of 0.79, significantly below the industry’s average of 3.74.

OPEN’s P/S Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

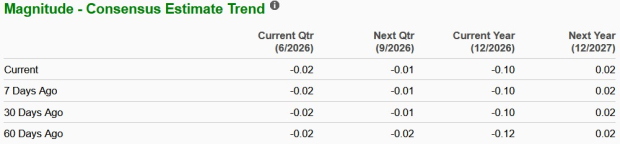

The Zacks Consensus Estimate for OPEN's 2026 loss per share indicates a 61.5% year-over-year improvement. Loss per share estimates for 2026 have narrowed in the past 60 days.

EPS Trend of OPEN Stock

Image Source: Zacks Investment Research

OPEN stock currently has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).