The annual tax season has many paying attention to how much they pay to the government and whether they’re paying more at a time when inflation has left a major dent in purchasing power. The Globe and Mail conducted an assessment to look how much tax burdens have changed in the past decade.Graeme Roy/The Canadian Press

As Canadians reckon with meteoric rises in the cost living since the start of the COVID-19 pandemic in 2020, taxes have continuously been in the spotlight.

They’ve been the focus of political parties, with promised tax cuts for the middle class during the recent federal election campaign, a Liberal turnaround on proposed increases in capital-gains taxes and a scrapped consumer carbon tax.

Meanwhile, annual tax season is near its end, drawing people’s attention to exactly how much they pay to the government and whether they’re paying more at a time when inflation has left a major dent in purchasing power.

With that in mind, The Globe and Mail set out to assess how much people’s tax burdens have actually changed over the past 10 years. We considered more than just income taxes, and included the impact of property taxes, sales taxes and other levies to try and get a full picture of how much of your money goes to tax.

We worked with Jay Goodis, an accountant and chief executive of Tax Templates, to create profiles of four representative households across the country. They include a high-earning couple in Toronto with sizable capital gains, a middle-income renter couple in Vancouver and a small business owner in Halifax who is retiring.

To compare with taxation 10 years ago, we adjusted their incomes by inflation and calculated taxes under the 2014 tax rules. That means each of our tax profiles earned 79 per cent of their 2024 income in 2014.

We compiled property price and taxation data from municipalities across the country, and then spoke with Canadians for Tax Fairness and the Fraser Institute to fill in the blanks.

There are some limits to our approach. There is a vast array of specific tax credits for parents, first-time homebuyers, people who work from home and other demographics that we could not take into account. Some of these credits can lead to thousands of dollars in annual tax savings.

Our overall conclusions? Taxation for the middle class has remained relatively flat over the past decade. For higher-income folks, it has incrementally increased, something Katrina Miller, interim executive director at Canadians for Tax Fairness, said has been the goal of federal governments. For other groups, such as seniors, taxation has actually decreased.

“What it does show is that in incremental amounts, we can see upper-income brackets have seen taxes go up slightly, and people in lower-income brackets or seniors with fixed income, we’ve seen their tax decrease slightly,” said Ms. Miller. “That’s essential because that’s really been the focus of government tax policy.”

However, she said governments still have work to do to ensure people at the highest income levels are taxed fairly and can’t take advantage of loopholes to have lower effective taxation than most Canadians.

Middle-income renters

Our example is Sam and River, a middle-income couple who rent in Vancouver. Both in their late 20s, they make $70,000 a year each, roughly the average salary in the city, for a total household income of $140,000.

They each paid $11,139 in taxes for 2024, for a total of $22,278. They also each paid $4,977 in Canada Pension Plan contributions and Employment Insurance premiums. That means 16 per cent of their earnings went to income taxes, or 23 per cent if you include CPP and EI.

If you adjust their income for inflation, they would have made $55,300 each in 2014, for a total household income of $110,600.

In 2014, they each would have paid $9,346 in income taxes, plus $3,340 in CPP and EI. That means 17 per cent of their income went to taxes, or 23 per cent if you include CPP and EI.

Sam and River paid a slightly smaller percentage of their income in taxes in 2024, but the change is barely noticeable. If you include CPP as a tax, their tax rate actually went up by 0.08 percentage points. (Mr. Goodis says you could argue that CPP is more of an investment in your own future than a tax, however.)

Mr. Goodis said the biggest changes that affected the couple’s tax rate were a reduction of the second-lowest federal tax bracket from 22 per cent to 20.5 per cent, which came into effect in 2016. On the other hand, CPP added to their tax expenses.

A lack of change to their taxation continues when you consider their expenses. We used the Fraser Institute’s Tax Freedom Day Report to understand how taxes on expenses such as gasoline, alcohol and other purchases have changed.

In the institute’s study, an average family’s income rise by 68 per cent over the decade, but their sales tax burden rose by just 67 per cent, from $5,791 to $9,681. Taxes on liquor, alcohol and other types of amusement went from $2,473 to $2,585, an 5-per-cent increase.

Their auto, fuel and motor taxes went up from $1,530 to $2,147, a 40-per-cent increase (it should be noted that the 2024 figure includes consumer carbon pricing, which has been scrapped).

In the institute’s total roundup of the taxes paid (including income and property taxes), the family paid $40,121 in 2014 and $66,932 in 2024, an increase of 67 per cent. That’s the same pace of growth as their income.

Retirees

We created an income profile for a couple of 72-year-olds named Robert and Mary, who can afford to be snowbirds. They own a semi-detached house in the Toronto suburb Etobicoke.

Mr. Goodis said a couple like this would generally have an household income of around $125,000. We gave them each a total income of $62,500 for 2024, which includes Old Age Security (OAS) income of $8,618, CPP of $16,375 and a pension income of $37,507.

They each face a tax bill of $9,498, leaving them with a net income of $53,002 each. So, 15 per cent of their income went to taxes.

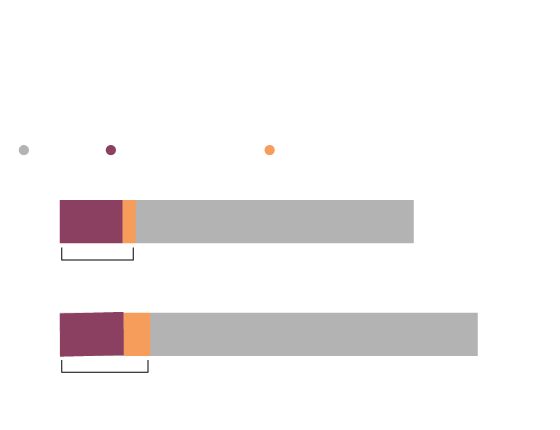

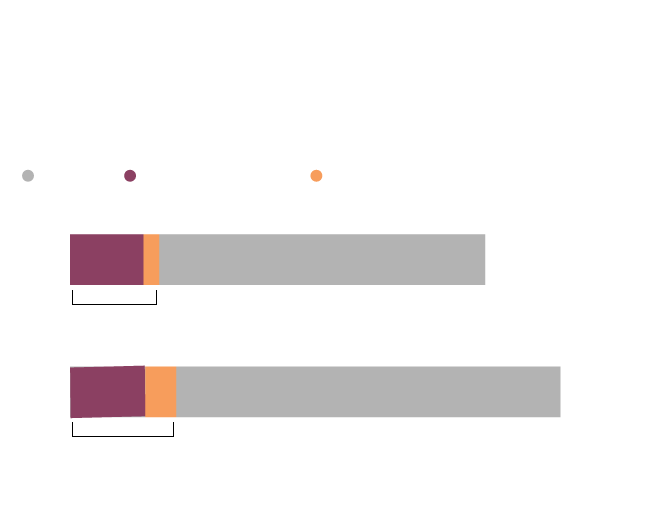

Tax burden steady

The below graph shows that income taxes barely moved between

2014 and 2024, even as the couple's income rose. Property taxes,

which rose much faster than inflation, are the only reason their

overall tax burden didn't drop more.

Total property taxes

Income

Total income taxes

$18,924

$3,904

2014

$105,800

24%

$18,996

$7,801

2024

$125,000

22%

the globe and mail

Tax burden steady

The below graph shows that income taxes barely moved between

2014 and 2024, even as the couple's income rose. Property taxes,

which rose much faster than inflation, are the only reason their

overall tax burden didn't drop more.

Total property taxes

Income

Total income taxes

$18,924

$3,904

2014

$105,800

24%

$18,996

$7,801

2024

$125,000

22%

the globe and mail

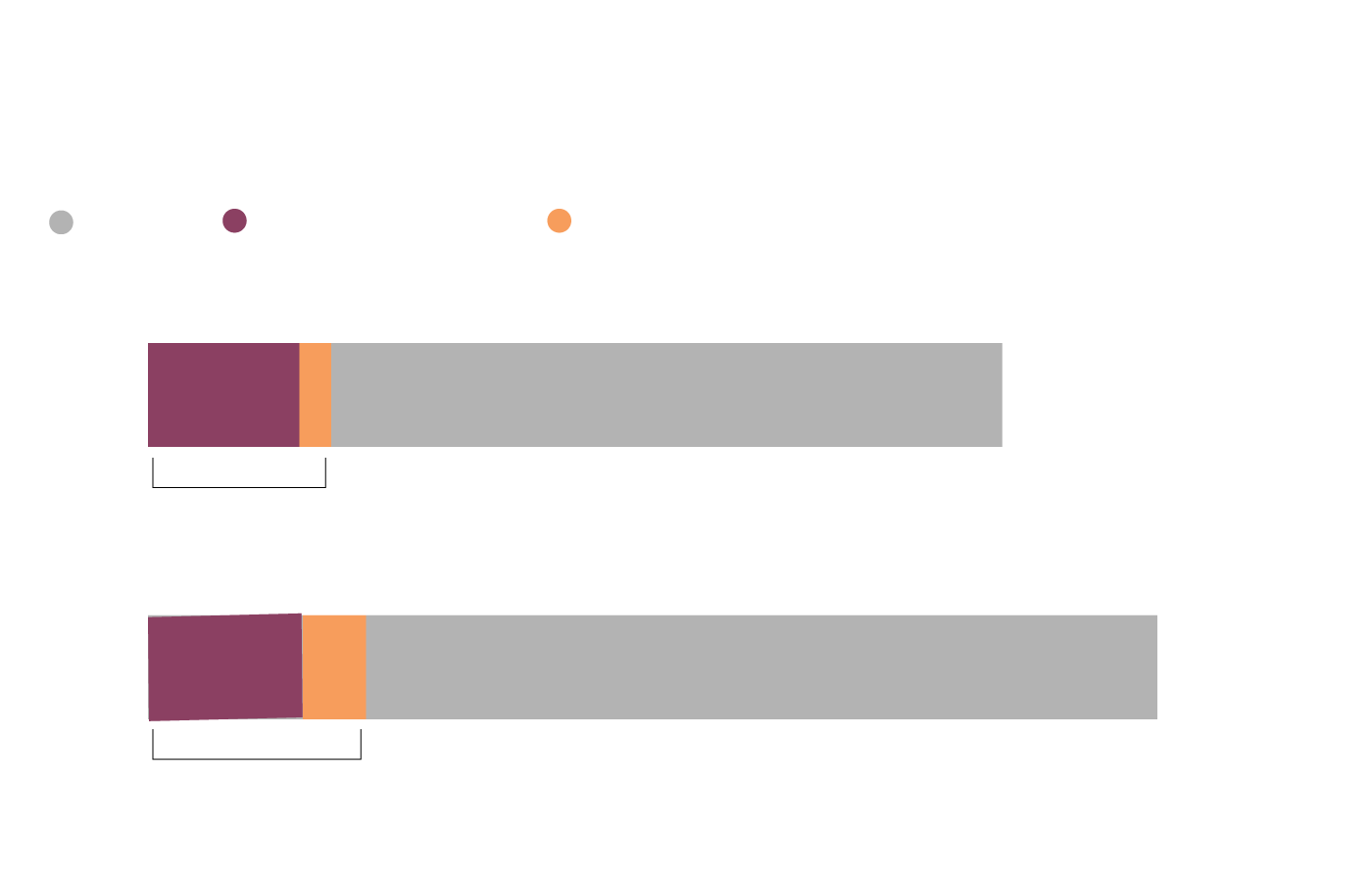

Tax burden steady

The below graph shows that income taxes barely moved between 2014 and 2024,

even as the couple’s income rose. Property taxes, which rose much faster than inflation,

are the only reason their overall tax burden didn't drop more.

Total property taxes

Total income taxes

Income

$18,924

$3,904

2014

$105,800

24%

$18,996

$7,801

2024

$125,000

22%

the globe and mail

In 2014, adjusting for inflation, Robert and Mary each earned an income of $52,900, including OAS of $6,677, CPP of $12,460 and pension income of $33,764. They each faced a tax bill of $9,462, leaving them with a net income of $43,439. So, 18 per cent of their income went to taxes.

In this scenario, Robert and Mary paid three percentage points less of their income toward taxes in 2024. Mr. Goodis said a reduction of the second-lowest tax bracket in 2024, an enhanced basic personal exemption and an exempt pension income amount that was introduced in 2015 all helped the couple’s taxes grow slower than inflation.

However, he added that other factors could make the couple’s taxation even lower, since a couple this age in 2024 would have had more time to save in their tax-free savings account, allowing for more tax-free income in retirement.

Property taxes are one segment in which their taxes increased. We considered the average assessed value of an Etobicoke home. In 2024, the couple would have a property tax bill of $7,801, a 81-per-cent increase from 2014, when it was $3,904.

However, the couple’s combined tax bill was still slightly lower in 2024, at 22 per cent of their income, than the 24 per cent in 2014.

Capital-gains earners

How much money did capital-gains earners save when the federal government walked back its plans to hike the capital-gains inclusion rate to 66.7 per cent from 50 per cent for earnings above $250,000?

We created a profile of two high-income earners named Kevin and Julia in Toronto.

Kevin earned $150,000 in salary in 2024 and sold a second home for $500,000 profit, while his wife, Julia, made $100,000.

Capital gains

This graph shows that the lack of a capital gains tax hike allowed

the couple to keep three per cent more of their income

Total taxes

% income

With capital

gain hike

$223,582

30%

Without

capital

gain hike

$201,278

27%

the globe and mail

Capital gains

This graph shows that the lack of a capital gains tax hike allowed

the couple to keep three per cent more of their income

Total taxes

% income

With capital

gain hike

$223,582

30%

Without

capital

gain hike

$201,278

27%

the globe and mail

Capital gains

This graph shows that the lack of a capital gains tax hike allowed

the couple to keep three per cent more of their income

Total taxes

% income

With capital

gain hike

$223,582

30%

Without

capital

gain hike

$201,278

27%

the globe and mail

If the capital-gains inclusion rate were hiked, the couple’s total tax bill would have been $223,582, or roughly 30 per cent of their income. Instead, it will be $201,278, roughly 27 per cent of their income.

Overall, the couple saved more than $20,000 on their taxes for 2024, which Ms. Miller said was relatively small when you consider the size of earnings and the increase only applying in years of major capital gains.

When we adjusted the couple’s 2014 income for inflation, Kevin and Julia’s total tax bill accounted for 26 per cent of their income. Ms. Miller said this means the government’s goal of slightly shifting tax burdens toward high-income families is likely succeeding.

Small business owners

The federal government’s plans to hike the capital-gains tax also included changes to the lifetime limit of gains earned by owners of some small businesses that are exempt from tax. Now that the changes have been canned, a lesser-known change to taxation may have a larger impact on business owners and other people who earn non-standard forms of income.

It’s called the alternative minimum tax (AMT), and it kicks in for certain high earners to ensure that they face a reasonable tax bill by treating 100 per cent of capital gains as income, rather than 50 per cent under ordinary tax rules. It also limits how people can use capital losses as a deduction on their income. This article describes how it works. We used a profile of a single woman in her 60s named Melissa who is retiring and sold her Halifax storefront business for $2.5-million last year, while also paying herself a salary of $75,000.

She paid $510,459 in taxes for 2024, $169,908 of which was added through federal and provincial AMT rules. She also paid $4,056 in CPP contributions, meaning a total of 20 per cent of her income went to taxes.

If the capital gains increases had not been walked back, the picture is not very different. She would have paid roughly $3,000 dollars more in taxes, for a total of 21 per cent of her income. The difference shows that the AMT can still lead to a higher tax bill for people who earn a high income in a given year.

For our 2014 profile, Melissa earned a salary of $59,250 and sold her business for $1,975,000. Income taxes comprised of 15 per cent of her income.

The results show that despite a five-percentage-point increase in Melissa’s tax payments, taxation is still relatively small for capital gains compared with salaries. For example, her 2024 taxes were 20 per cent of her income, while Kevin and Julia’s were 27 per cent of their income. Even though Melissa had a larger income, less of it was taxed because of a larger proportion of capital gains.