A different look at the news

- Ottawa ‘at the mercy of the economy’

- A Mark Carney album cover I'd love to see

- A Clinton e-mail I'd love to see

- What to watch and read this weekend

- What to watch for in the coming days

The past week

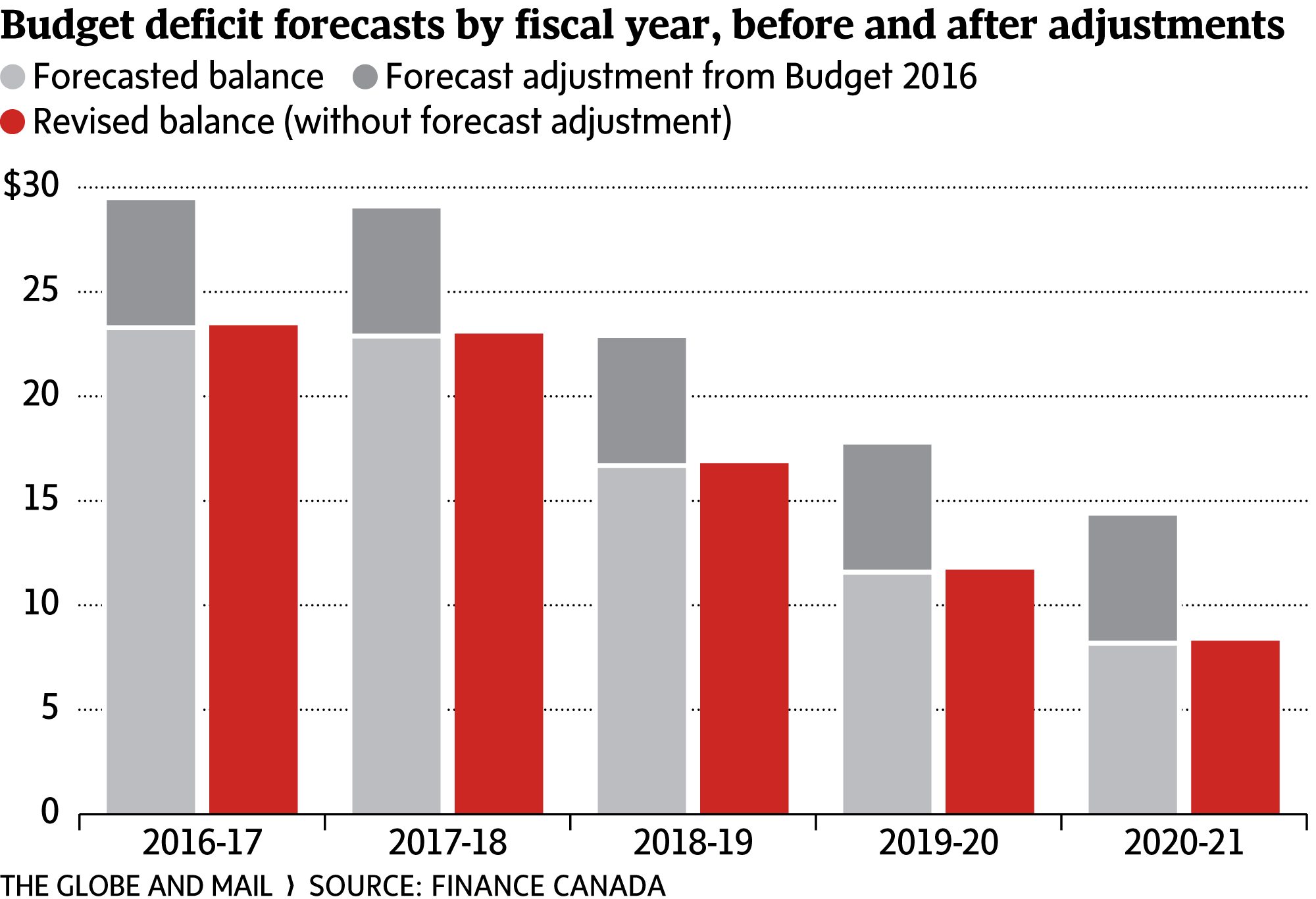

Markets are taking Bill Morneau’s fiscal update in stride.

One question, though, is whether Canada’s Finance Minister should have done more to help a tired economy.

He had the fiscal room to do more without raising too much fuss from the world’s credit rating agencies, observers say, but appears to have chosen a cautious approach.

As The Globe and Mail’s Bill Curry reports, Mr. Morneau and his governing Liberals are pumping tens of billions of dollars more into infrastructure projects over the next 12 years

His new measures include a national infrastructure bank that could be up and running by the end of next year.

“There’s not a lot of new material in this ‘mini-budget’ beyond some early details on the infrastructure bank, and a refreshed fiscal plan with the contingency scrubbed out,” said BMO Nesbitt Burns senior economist Robert Kavcic.

“In a nutshell, the weaker growth outlook and some additional spending have filled the contingency hole, leaving the broader fiscal plan little changed, but now more at the mercy of the economy.”

Here’s what other economists had to say:

“Bill Morneau has been finance minister for all of a year, but he’s learned pretty quickly to deal with economic disappointment. Over the course of a single budget and two fiscal updates, Canada’s Liberal government has witnessed firsthand the fiscal fallout that attends subpar growth and lukewarm inflation. Although hardly unique to Canada’s sovereign, a lower and flatter trajectory for nominal GDP has robbed the government of hoped-for revenue. Importantly, the sizeable amount of prudence set aside in budget 2016 (fully $6-billion per year) has been called on to blunt the impact on the budget balance.” Warren Lovely, National Bank

“Finance Minister Morneau recently outlined the objective of his government as striving to find balance between short-term actions and the ‘essential goal of keeping [his] eye on the long game.’ Today’s progress report on how the fiscal situation is evolving seemingly embodied this view with an ambitious infrastructure plan to boost longer-term growth. This comes at a cost, however. Larger deficits through the projection period and a lack of a balanced budget fiscal anchor are disappointing developments. Furthermore, the removal of the adjustment for risk has the potential to increase the deficit profile should unforeseen risks materialize. That being said, the possibility for increased private financing to support these ambitious government efforts is a positive development given the demographic and productivity headwinds facing Canada.” Laura Cooper, Royal Bank of Canada

“The lack of new fiscal stimulus in the short term leaves that monetary policy as the sole source of stimulus if the Canadian economy underperforms. We expected the update to contain some new spending in the short term to compensate for the lack of impact from the tax credit to families, allowing the [Bank of Canada] to remain on the sidelines for some time. With this in mind, we believe that the likelihood that the BoC may need to provide more easing next year has increased.” Charles St-Arnaud, David Wagner, Nomura

“What is typically a staid affair was made more exciting with the announcement of expanded infrastructure spending and the creation of a national infrastructure bank. Both of these are welcome developments: Should it work as promised, the infrastructure bank may provide a way to turn limited federal funds into significant project spending. It remains to be seen how successful the scheme will be as it will depend on the types of projects made available.” Brian DePratto, Toronto-Dominion Bank

“Although the Liberals will fail to achieve their core fiscal election promises, they can afford to run moderate budget deficits without fears of them triggering higher government debt servicing costs. As we have mentioned before, Canada is in good fiscal shape when compared to most other countries … In fact, policy makers could probably afford to run even larger budget deficits if the economy were to slump again, which would reduce the pressure on the Bank of Canada to risk resorting to unconventional policies like central banks have done in some other countries.” David Madani, Capital Economics

An album cover I'd love to see ...

“The rumours of Mark’s demise aren’t true.”

Your weekend

As Barry Hertz puts it in his review of Hacksaw Ridge, director Mel Gibson “has a thing for pain.” So, too, might moviegoers.

My colleague Barry notes how soldiers are burned, shot, stabbed and turned inside out, with guts just about everywhere.

But in terms of movie-going pain, check out what Barry thinks of Mr. Gibson’s first film in 10 years.

For something more uplifting, read Johanna Schneller’s look at Rachel McAdams, the star of Doctor Strange who first graced the stage at the age of 12 at a kids’ theatre camp in St. Thomas, Ont.

Which, according to Barry’s review of Doctor Strange, may be time better spent than seeing the movie itself.

For your reading pleasure - and maybe you want to read this one in the newspaper, rather than online - take a look at Navneet Alang’s review of David Sax’s The Revenge of Analog: Real Things and Why They Matter. It’s a book about how certain things, like vinyl, are making a comeback.

Or you could have some real fun, and take my colleague Evan Annett’s Ultimate U.S. Election Quiz.

As for me, after I do the quiz I’m going to sit home and watch TV. Because my friend John Doyle told me to. He writes this weekend about Sunday night’s Frontier – a new drama about Canada in the 18th century – and (step aside, Mel Gibson) it’s got greed, murder, rage, revenge and pillage. Business readers may want to check it out, too: It’s an action piece about the fur trade wars.

And don’t miss my colleague Dave McGinn’s latest on our mid-life years. Here’s what he says this week:

“In the latest instalment of Halftime, my series on life in your 40s, I spoke to Anne Merklinger, CEO of Own the Podium. She was a competitive swimmer and a competitive curler and, on top of that, has had a stellar career as an executive. It was no surprise, I guess, that in reflections about her own life during her 40s she stressed over and over again how important it is to hustle for what you want.”

If you’d like to share your thoughts on the series or suggest ideas, please get in touch. Dave can be reached at dmcginn@globeandmail.com Or use the hashtag #globehalftime .

The week ahead

An e-mail I'd love to see ...

You’ll be staying up late on Tuesday, and possibly pulling an all-nighter depending on how things play out in the U.S. presidential race.

That all-nighter depends on your feelings about Donald Trump and Hillary Clinton, and what you’ve got invested where.

Put simply, the markets will take a calmer view if Ms. Clinton wins the White House. If Mr. Trump emerges victorious, all bets are off.

And while they are the show, they’re not the only show.

“As we consider what the presidential election means for the U.S. economy, it is worth acknowledging that the executive branch of the government is only but one branch,” said Megan Greene, the chief economist at Manulife Asset Management in Boston.

“The Legislative (the House of Representatives and Senate) and Judicial (Supreme Court) branches are also crucial in determining what the next administration will be able to achieve over the next four years,” she added in a report on Tuesday’s election.

“Our base case scenario is that the House of Representatives will be controlled by the Republican Party, with current House Speaker Paul Ryan remaining in his role. Far-right-wing members of his party are making noises about dumping Ryan, but the lack of an alternative suggests the Speaker will remain in the office for now. The Senate, on the other hand, is too close to call. “

What to expect on the markets?

“If Hillary Clinton wins the election, the equity markets are likely to fall the next day on the back of fears of taxes rising and eating into corporate profitability,” Ms. Greene said.

“Over the medium term, however, we expect a Clinton administration to provide some fiscal stimulus and to deliver growth roughly in line with the U.S. potential growth rate (1.5-2 per cent). This should underpin a recovery in equities and a moderate tick up in 10-year Treasury yields,” she added.

“The market response to a Trump victory is less clear. On the one hand, we expect a Trump victory would be a risk-off event, with a much higher degree of policy uncertainty than we would have in the event of a Clinton win. As a result, we might see a flight to U.S. Treasuries given that they are the largest, most liquid asset class in the world. But looking at Trump's policy proposals, we believe we could expect lower taxes, higher spending, more debt and an economic recession.”