Valeant Pharmaceuticals International Inc.'s diving share price has reinforced the idea that any company that rises above Royal Bank of Canada to the top of the S&P/TSX composite index, in terms of its weighting, is a stock to avoid.

But what if Toronto-Dominion Bank is the next usurper?

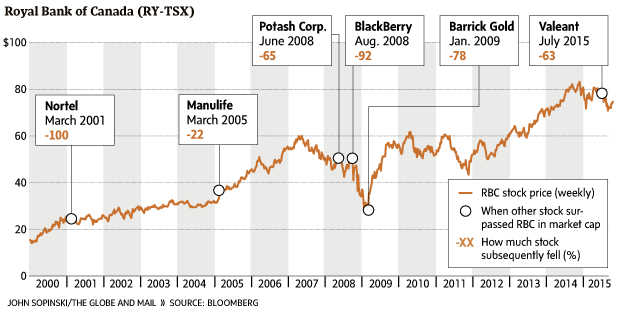

Valeant hit the top spot on the benchmark index in late July. The pharmaceutical company's share price was on its way to a record high of $346 as it gobbled up acquisitions, while RBC's share price was slumping amid concerns about the Canadian economy.

The divergence gave Valeant a 6.2 per cent weighting in the index, slightly above RBC's 6.1 per cent weighting.

But the switch lasted just two days. Since then, RBC's share price has recovered some lost ground while Valeant's has fallen more than 60 per cent – much of it over the past couple of days as investors recoil from allegations from a short-seller that the company has made questionable arrangements with specialty pharmacies. The sharp decline has reduced Valeant's weighting in the index to just 2.4 per cent and lowered its ranking to 10th spot.

Surpassing RBC on the index only to fall on hard times is not unusual. In fact, it's the norm: Over the past two decades, every stock that has made it to the top – Nortel Networks Inc., Barrick Gold Corp., Potash Corp. of Saskatchewan Inc., BlackBerry Ltd. (formerly Research In Motion Ltd.) and Manulife Financial Corp. – has subsequently fallen by double-digits at best. In the case of Nortel, the shares were wiped out.

The lesson: Companies tend to surge to the top of the TSX composite index because of investor infatuation with the stocks or their underlying commodities (gold! fertilizer!), rather than a more fundamental increase in profits and revenues. To put it bluntly, most of these stocks have popped like bubbles.

This has left RBC as the natural leader for decades, and has given it marketable cachet among customers as Canada's largest company and biggest bank.

But there is a threat to this status: TD is closing the gap with RBC without the benefit of investor infatuation. Instead, TD has integrated Canada Trust, expanded into the United States with the acquisitions of Banknorth and Commerce Bank, risen to the No. 1 credit-card provider in Canada after lagging its peers and put a focus on customer satisfaction with appealing marketing campaigns.

The gains have landed TD in second spot on the TSX composite index, and it has been closing the gap with RBC.

In 2005, TD's market capitalization was 26 per cent lower than RBC's. By 2010, the difference had shrunk to 16 per cent. Last year, the difference was 14 per cent and today it's just 8 per cent – or $99-billion versus RBC's $108-billion.

That's no longer a commanding lead by RBC. To be sure, the bank isn't standing still: It is close to completing its $5.4-billion (U.S.) acquisition of Los Angeles-based City National Bank, a private bank that has given RBC big plans for expanding its reach in the United States.

If the integration and expansion are successful, RBC may be able to build some distance with TD on the benchmark index. But no doubt, RBC is looking over its shoulder: Although it is a curse for companies to rise above RBC, TD – a rival bank with a similar investor base and valuation – would mark a notable exception.