Briefing highlights

- What analysts say about high stock prices

- Markets at a glance

- Canadian exports rebound, deficit narrows

- U.S. trade gap widens

- BMO profit slips, dividend up

- Toronto home prices ease

- Laurentian Bank profit, dividend up

- Roots posts jump in sales

Lofty stock markets

As Goldman Sachs put it recently, "it has seldom been the case that equities, bonds and credit have been similarly expensive at the same time, only in the Roaring '20s and the Golden '50s."

As Goldman also put it recently, according to Bloomberg, "there will be a bear market, eventually."

So let's take the temperature as stock markets drive ever higher and observers question those valuations, particularly after U.S. Senate approval of a tax overhaul, which would slash the corporate rate, and ahead of the Federal Reserve's next meeting, at which a rate hike is expected.

Here's a sampling of observations since Sunday:

"The central question for asset allocators is where we are in the economic cycle and what comes next. Goldilocks has been a massive boon to risk assets as it typically is historically. A move into a period of reflation is less bullish for equities. Bonds underperform less in 'reflation' phase while commodities are typically the relative winners. A worse scenario would be a plateau phase for economic growth in which earnings growth typically slows sharply usually with slower growth in corporate leverage too, something now evident in the flow of funds. This is much more negative for risk assets. We are reluctant to call the end of the bull market just yet. But we will monitor cyclical developments and positioning ever more closely for signs that the equity overweight is no longer warranted in asset allocation portfolios." Citigroup

"According to traditional valuation gauges that take a long-term view, some stock markets did look frothy. At its recent levels in excess of 30, the cyclically adjusted price/earnings ratio (CAPE) of the U.S. stock market exceeded its post-1982 average by almost 25 per cent, comfortably sitting in the highest quartile of the distribution. … Admittedly, this is still short of the extraordinary peak of 45 reached during the dotcom bubble of the late 1990s. But it is almost twice the long-term average computed over the period 1881–2017 … Stock market valuations looked far less frothy when compared with bond yields." Bank for International Settlements

"According to the most recent University of Michigan's Survey of Consumers, the mean respondent estimates that there is a 64.5-per-cent probability of an increase in the stock market in the next year, which ranks as the highest such reading in the survey's history. This should be a source of concern to investors as such market bullishness ultimately increases the risk of an imminent position squaring correction. We still remain positive on financial market prospects for now and still recommend clients to play the growth trade. However, rather than overweighting equities as our favoured instrument to do so, we continue to prefer playing this trade through our regional and sector allocation. Hence, we remain comfortable with our neutral stance on equities against bonds at this time. We also remain concerned that a growing headwind for equities over the coming months will be the combination of accelerating inflation data and more restrictive central bank monetary policies." Luc Vallée, chief strategist, and Eric Corbeil, senior economist, Laurentian Bank Securities

"We expect the global political risk temperature to remain elevated in 2018, particularly in [advanced economies]. The current disconnect between the political outlook and economic and financial markets performance is itself a major risk. Trade is another important factor to watch. NAFTA is under threat and the risk of a trade war has risen, although it is still not our base case." Citigroup

"In more normal market conditions, the best-performing trade over the last 12-18 months will not be the top performer over the next 12-18 months because eventually smart money moves into a trade with lower valuations. But these are not normal market conditions. In this ultra-low volatility environment, momentum is a strong force to overcome. Tech has momentum and earnings growth behind it. After a swoon in tech stocks in June, there were similar calls for a more long-lasting shift out of tech and into energy as oil prices recovered. The Nasdaq 100 has gained over 14 per cent off its July lows when those calls were made. This time the sector chosen to replace tech is financials because of U.S. tax reform. Most economists think the Republican tax plan will have little impact on short-term economic growth, so lending is unlikely to pick up substantially to support the earnings of financials."

Jasper Lawler, London Capital Group

"If tax cuts boosted corporate profits without materially or permanently lifting real GDP growth, equities would always provide a more direct vehicle for trading Trumponomics than Treasuries or the dollar. The long-standing view of our U.S. equity strategists has been that successful tax reform would add about 200 points to a baseline end-2017 S&P500 projection of 2,550 (so 2,800 target for early 2018), largely through a $10 [earnings per share] boost from cutting corporate taxes by 15 points. Within the index, our rotation story is in line with the consensus view, so favouring domestics over multinationals, small over large cap and value over growth stocks. But since we've thought that the incremental earnings boost was not fully priced (we estimate that it's 50-per-cent discounted), our equity strategists reiterated these views [Monday] rather than faded last week's stock surge." JPMorgan Chase

"The mantra is that the stock market will continue to surge on tax momentum because the 'reform' isn't fully priced in. Well, from the numbers I've seen, the impact on S&P 500 [earnings per share] is $10 of upside from the tax stimulus, taking 2018 to $151. Think about that for a minute. Even at that level of earnings expectations, the forward [price/earnings] multiple would be bordering on 17.4x. If that is not a full priced stock market, one that is not discounting a very rosy economic outlook, then I don't know what is. I would contend that tax cuts are more than fully priced in." David Rosenberg, chief economist, Gluskin Sheff + Associates

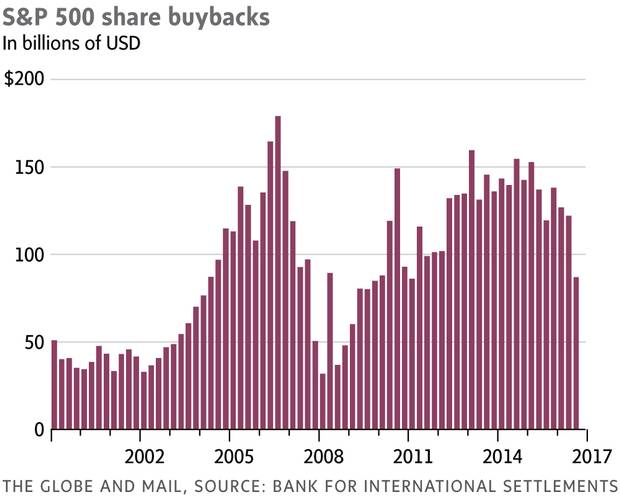

"Dividends per share of U.S. equities have been growing at a much faster rate since the [Great Financial Crisis], giving rise to questions about long-term sustainability … This is because the faster growth was supported in part by a significant shift in corporates' dividend policy. The share of net income paid out in dividends has increased by more than half over the last five years. … The dividend payout ratio is back to the relatively high levels observed in the 1970s, and thus may be approaching an upper bound. High dividends per share were also supported by stock repurchases. Except for a short interlude in 2008–09, share repurchases have been very large since the early 2000s. … When and if interest rates begin to rise, corporates may have the incentive to tilt their capital structure back to equity, or at least to reduce stock repurchases, which could raise further questions about stock market valuations." Bank for International Settlements

"Possibly the biggest challenge for investors is likely to be judging when the current expansionary business cycle will end. Cycles are increasingly mature, particularly in the U.S. Resilience to shocks is falling, as slack is low, pent-up demand is moderating and financial vulnerabilities are rising. Monitoring resilience, including asset valuations and leverage, and signs of excess demand and euphoria will be crucial. Deteriorating financial conditions may signal or indeed cause a slowdown in the real economy." Citigroup

Read more

- Follow Inside the Market

- ‘Mundane works’: BMO’s Brian Belski on how to invest in rising Canadian stocks in 2018

- Ian McGugan: Today’s apparently calm market disguises a rapidly brewing storm

- Relax, the stock market’s end isn’t nigh. (You’ve got a year or so)

- Ian McGugan: The two most worrisome indicators for markets right now

- Scott Barlow: Mining, energy investors need to start watching China immediately

- Tim Shufelt: The ‘sleeping giant’ within the TSX that could be the market’s next outperformer

Markets at a glance

Read more

Exports rebound, trade gap narrows

Some good news for Canadian exporters: Our trade deficit narrowed markedly in October as shipments to the U.S. and elsewhere rebounded.

Canada's trade gap narrowed to $1.5-billion from September's $3.4-billion, Statistics Canada said today, as exports climbed 2.7 per cent and imports fell 1.6 per cent.

The export rebound followed four months of declining shipments.

Leading the narrower shortfall were a 4.1-per-cent jump in exports to the U.S., whose shipments to Canada fell 0.6 per cent.

"We're eagerly awaiting signs on Q4 growth after the third quarter's slowdown, and trade data for October give us reason for optimism," said Nick Exarhos of CIBC World Markets.

And here's something for President Donald Trump and his NAFTA negotiators to glom onto: Canada's surplus with the U.S. widened to $3.5-billion from September's $2-billion.

When you look at real terms, or just by volume, imports slipped 3.9 per cent while exports rose 1.2 per cent. On that basis, Canada jumped to a surplus of 131-million from a $2-billion deficit.

"The broad-based gains in exports only translated into a volume increase of 1.2 per cent, as some of the increase was due to firmer oil pricing, of which we'll see more of in the November figures," Mr. Exarhos said.

"That's a positive first sign on October GDP, but we still have more work to do in reversing the past few months' disappointment on real exports," he added.

"Nevertheless, today's figures are positive for the [Canadian dollar] and slightly negative for the front end of the Canadian [yield] curve, although there is still no real chance of a Bank of Canada rate hike tomorrow."

Read more

BMO profit slips, dividend up

Bank of Montreal capped the latest round of earnings among Canada's major banks with a 9-per-cent drop in fourth-quarter profit.

It raised its quarterly dividend by 3 cents to 93 cents.

BMO profit slipped to $1.2-billion, or $1.81 a share. Adjusted profit, which the bank said cut earnings per share by 17 cents, fell 6 per cent to $1.3-billion or $1.94.

The bank posted an annual profit of almost $5.4-billion or $7.92 a share, though, up notably from a year earlier.

Its provision for credit losses rose in the quarter to $208-million, and return on equity declined to 12.1 per cent.

"We are making good progress against our financial and strategic objectives," said chief executive officer Darryl White.

"BMO's Q4 adjusted earnings missed expectations, although it was on the back of reinsurance claims that cost it 17 cents per share," said Barclays analyst John Aiken.

"We believe that the headline miss, the decline in U.S. margins and the fact that much of the growth in the quarter was generated by capital markets are unlikely to garner much support in the market," he added.

"That said, this will likely be offset by the better-than-anticipated dividend increase and strong domestic retail performance. Consequently, we would not expect to see any material over- or underperformance by BMO today."

Read more

Toronto home prices ease

Toronto home prices dipped in November as new listings soared, leaving unsold inventory at more than double the level from the same time last year, The Globe and Mail's Janet McFarlandj reports.

The Toronto Real Estate Board said the average home sold for $761,757 in the Greater Toronto Area in November, down 2.4 per cent compared to October.

The price drop halted a modest price recovery that began in September and continued in October after a downturn through the spring and summer.

Read more

- Janet McFarland: Toronto home prices dip in November

- Janet McFarland: Tougher mortgage rules could shut out 50,000 potential home buyers a year: report

More news

- Laurentian Bank raises dividend as profit more than doubles

- Roots reports sales up 13 per cent from a year ago