Briefing highlights

- Projections for Canadian economic growth

- Loonie seen tumbling as low as 69 cents

- What to expect from interest rates

- Housing markets forecast to ease

- Analysts fret over Trump trade agenda

- Oil: It all comes down to price of a barrel

- Markets: Can stocks keep up their bull run?

1.8% to 2%

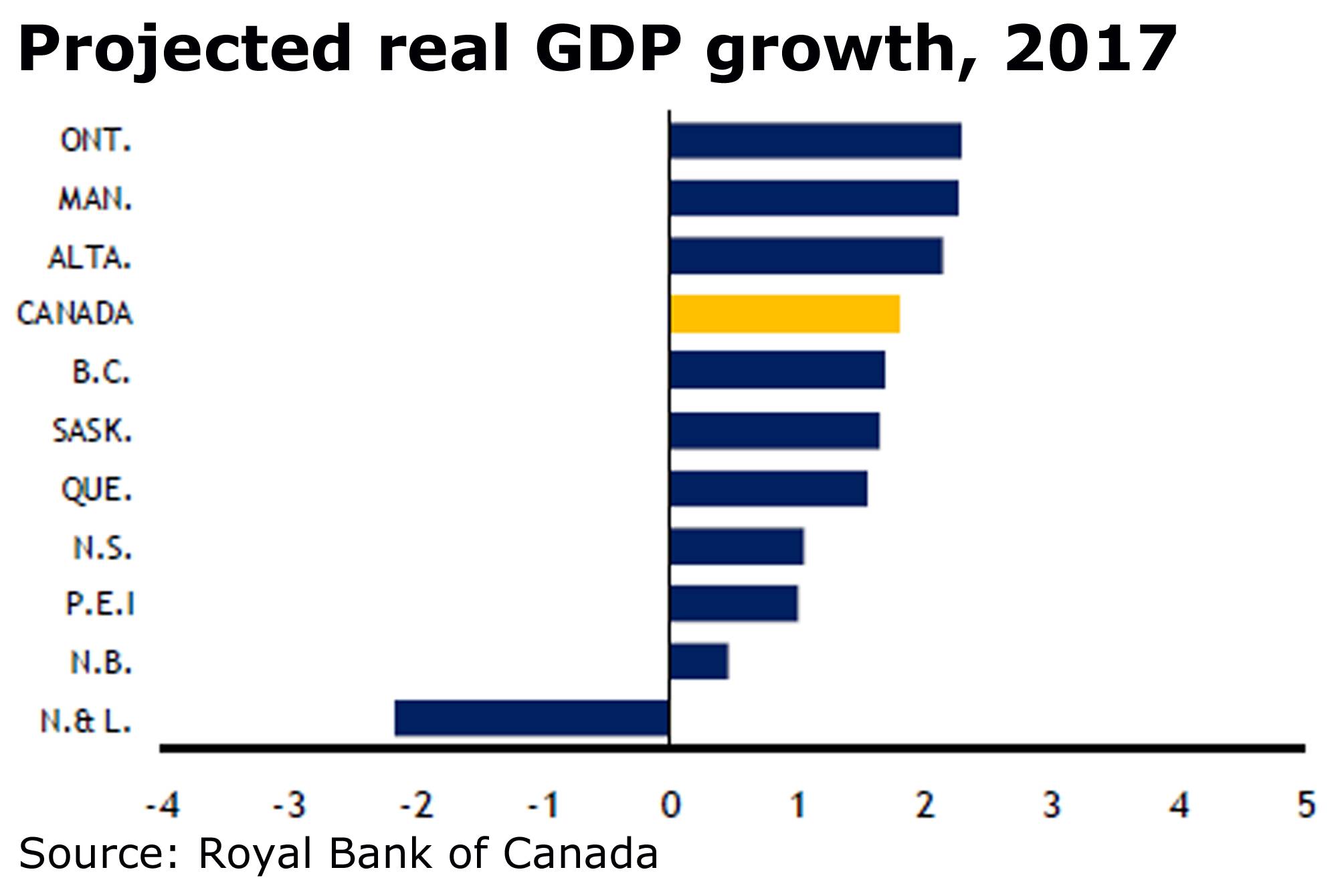

Projected 2017 economic growth

Economic growth

While observers differ on the exact speed, most agree it will be modest next year. Canada’s economy can be expected “to gain an inch, not a yard,” as Toronto-Dominion Bank put it in its latest outlook.

“Just stopping the bleeding of the past few years will help boost Canada’s economic trajectory,” said TD chief economist Beata Caranci.

This year was certainly nothing to crow about as Canada suffered the impact of the oil shock, the Alberta wildfires and other various and sundry.

Economists generally agree Canada’s economy will expand by about 2 per cent in 2017, give or take (largely take), a couple of basis points.

“After two years of struggling with roughly 1-per-cent growth, we have bumped up our 2017 GDP outlook for Canada to 2 per cent,” said Bank of Montreal chief economist Douglas Porter.

“Beyond a firmer external backdrop, domestic growth will find some support from a roll-out of long-awaited infrastructure outlays and supportive financial conditions,” he added.

The federal government’s stimulus measures, including infrastructure spending, should help buoy the economy, analysts say.

“However, we expect that the economy’s main growth engine of the past two years – the housing sector – will lose momentum, partly owing to tighter mortgage insurance rules,” Mr. Porter said.

“On the flip side, the economy’s biggest drag of the past two years – business investment – is projected to nudge higher after a combined plunge of more than 18 per cent in 2015-16.”

Also on the dark side is an elevated jobless rate that’s projected to hover near the 7-per-cent level for at least the next couple of years.

So much, of course, depends not on only oil prices, but also the economic fortunes of the U.S., and its trading partners such as Canada, under Donald Trump.

British Columbia comes in for special mention because so much of its economy has been tied to housing, and the proverbial bubble there has burst, not in small part because both the provincial and federal governments have engineered a cool-down through tax and mortgage measures.

Canada’s westernmost province has led economic growth, and some economists believe it will continue to do so. Others, though see it slipping below Ontario.

“Giving up the top spot it held in 2016 will be British Columbia, where we expect the recent cooling in home resale activity to be largely sustained in 2017, thereby quieting off a powerful source of growth in the province during the past few years,” Paul Ferley, Royal Bank of Canada’s assistant chief economist, and his colleagues, senior economist Robert Hogue and economist Gerard Walsh, said in their latest outlook.

“Our GDP forecast for British Columbia (+1.7 per cent) would be weaker than the national average (1.8 per cent) for the first time in six years.”

RBC expects Ontario and Manitoba to take the lead. And while the Trump administration means uncertainty, Ontario could benefit from a stronger U.S. economy and a lower loonie.

The Canadian dollar

The loonie has gained of late as crude prices climbed on an agreement between OPEC and some non-OPEC producers to cut production next year.

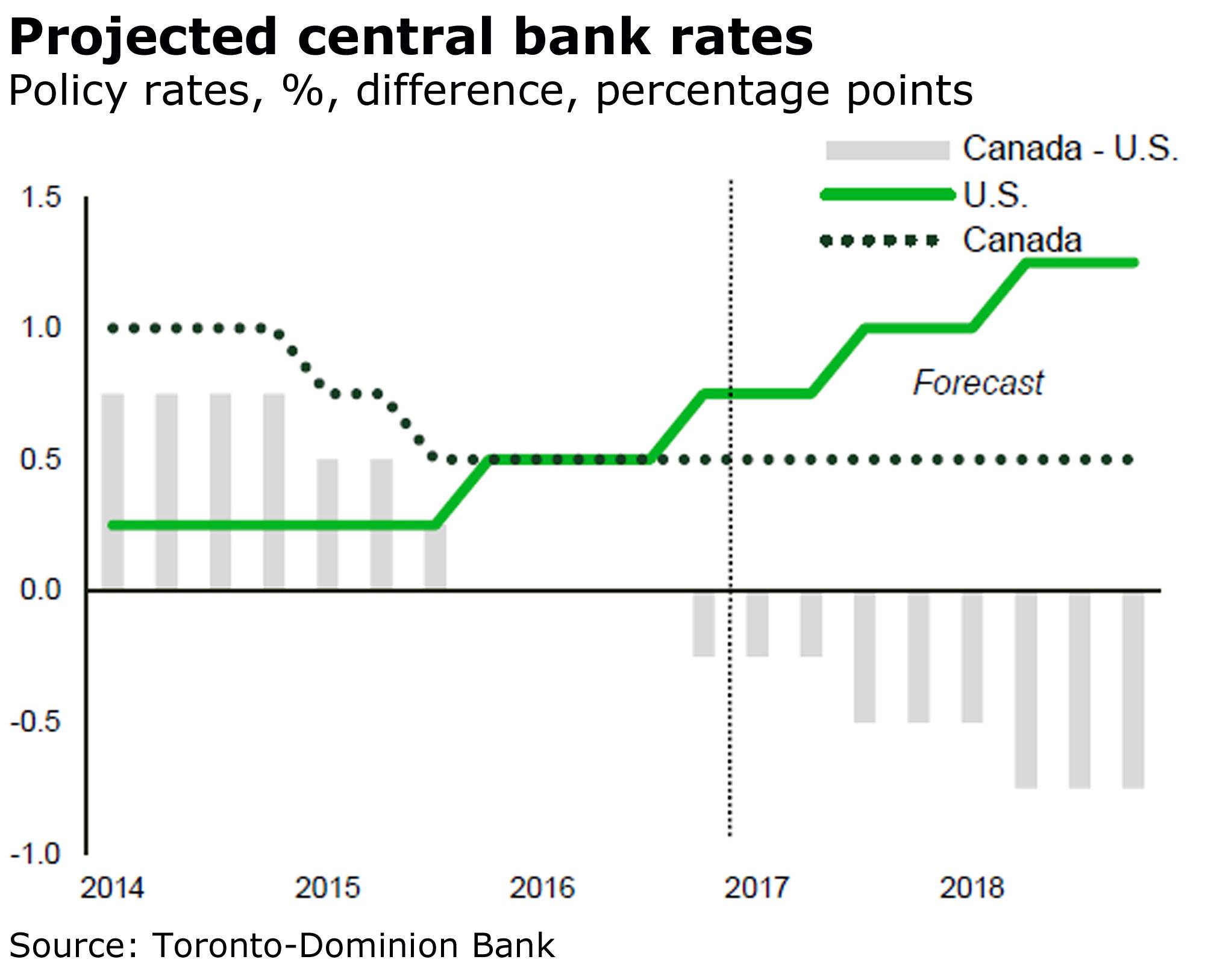

While the outlook for the currency will depend partly on oil prices, also at play are central bank policies, which are diverging in Canada and the United States.

The Federal Reserve is in the midst of a hiking cycle, albeit gradual, while the Bank of Canada isn’t expected to raise its benchmark rate until 2018 or possibly even 2019, all of which combine to make the loonie less attractive, a boon to exporters.

Most forecasters expect the currency to slide again, to about 72 cents (U.S.) but potentially as low as 69 cents.

“HSBC’s FX team now sees a weaker Canadian dollar going forward with USD/CAD at 1.35 at the end of 2016 and rising to 1.45 by mid-2017,” said HSBC Bank Canada chief economist David Watt.

What he means is that, when you flip the bank’s foreign exchange forecast around, HSBC projects the loonie to close out 2016 at about 74 cents and tumble further to a shade below 69 cents within six months.

Mr. Watt is at the low end of the loonie forecasts, and among those observers who also expect Governor Stephen Poloz and his Bank of Canada colleagues to cut their benchmark overnight rate to just 0.25 per cent from its current 0.5 per cent.

Interest rates

We already know that Canada’s central bank won’t raise rates, and will perhaps even cut, while its U.S. counterpart goes for possibly a couple more increases in 2017, depending on everything from market volatility to the Trump factor.

But longer-term rates are already on the rise in the wake of the U.S. election, and this has rippled into Canada.

“Though our forecast for a gradual tightening of monetary conditions by the Federal Reserve remains unchanged, we have shifted our forecast for global bond yields upwards in the wake of the U.S. election,” TD said in its outlook.

“Unfortunately for Canada, higher rates in the U.S. mean higher rates in Canada,” the bank added.

“This will act as a form of tightening in financial conditions at a time when the Canadian economy is no better off.”

Among other things, the run-up in yields threatens to jolt Canada’s housing markets further.

Housing

Housing markets are already adjusting to the recent federal mortgage and tax measures and B.C.’s new 15-per-cent tax on foreign buyers of Vancouver area homes.

Resales in Vancouver have collapsed. And while Toronto’s market is still on fire, the pace of growth in home prices is forecast to ease.

Indeed, the latest numbers from the Canadian Real Estate Association and the freshest reading of the Teranet-National Bank home price index show the impact, though Vancouver prices are still well up from a year ago.

“While Vancouver and the Fraser Valley have seen the sharpest falloff in activity in recent months, worsening affordability and tougher mortgage qualifying rules appear to be dampening momentum in the [Greater Toronto Area] and Southwestern Ontario,” said Bank of Nova Scotia senior economist Adrienne Warren.

“Tight supply amid near record demand continues to support strong price appreciation in the latter markets, while more balanced market conditions are putting downward pressure on prices in B.C.’s Lower Mainland,” she added.

“We anticipate a further softening in national sales and price appreciation in the coming months.”

Bond yields, which have been rising on the outlook for fiscal policy and inflation in the U.S., add another factor because of their link to mortgage rates.

“We don’t expect yields to rise significantly from current levels in the coming months, but if we’re wrong, the real estate market adjustment would certainly deepen,” said TD’s Ms. Caranci.

So again we see the Trump factor playing out, though its biggest impact may well be on trade.

Trade

This could be a biggie for Canada, given the incoming Trump administration’s threats, and it’s certainly among the greatest unknowns.

Donald Trump has oft complained about China and Mexico, but Canada could be caught up as he pulls out of the Trans-Pacific Partnership and renegotiates or, as he has threatened, tears up the North America free-trade agreement.

The Americans are eyeing our lumber and livestock exports, and who knows what else could be on the new agenda.

Certainly, changes to NAFTA could have a severe impact on Canada, which relies on the U.S. market for the bulk of its exports, even though our trade relationship with our neighbour isn’t out of whack.

TD’s Ms. Caranci wonders if Mr. Trump’s trade bark may be worse than his bite because he’s rarely attacked Canada as he leads the U.S. into a more protectionist era.

“Should that be the case, U.S. tax reform measures that boost investment and consumer spending south of the border would succeed in lifting demand for Canadian exports,” she said, though she cited the risks surrounding Mr. Trump’s policies.

“It is conceivable that Canada develops a stronger trade relationship with the U.S. over the long run, helping to recoup some of the lost ground in market share. But, until we see what side the coin lands on, U.S. policy uncertainty could act as a near-term constraint to business capital spending.”

Others fear something ugly.

“Though there is uncertainty over the aggressiveness of his trade policies, Mr. Trump has suggested imposing import tariffs of 45 per cent on goods imported from China and 35 per cent on goods imported from Mexico, including autos and auto parts,” said HSBC’s Mr. Watt.

“Canada had largely avoided the spotlight as a potential target of trade actions, but it has come under greater scrutiny in the post-election period,” he added.

“Accordingly, we see think that Canada is at risk of suffering some direct and some collateral effects from a shift toward isolationism in the U.S. in the New Year. A basic reason for Canada’s exposure is that it is still the third-largest source of imports to the U.S.”

Canada could benefit from Mr. Trump on the oil side, of course, notably his desire to build TransCanada Corp.’s Keystone XL pipeline.

Oil

Keystone aside, so much depends on the price of that barrel.

Observers expect to see a rise in prices of West Texas intermediate, the U.S. benchmark, and Brent, though many wonder if the OPEC countries will live up to their individual production caps, which also could affect how it all plays out.

“We remain of the view that WTI and Brent will average $56.40/barrel and $59/barrel in 2017, and a further price recovery will likely be Brent-led given that North America will most likely be the last region to rebalance,” said Helima Croft, RBC’s head of commodity strategy, and her colleagues Michael Tran and Christopher Louney.

A welcome development, this, for Canada’s commodity-dependent provinces Alberta, Saskatchewan and Newfoundland and Labrador.

“Along with the ramping up in federal infrastructure spending, we believe that brighter prospects in Alberta and Saskatchewan will be a key contributor to stronger expected growth of 1.8 per cent in Canada in 2017 compared to 1.3 per cent in 2016” said RBC’s Mr. Ferley, Mr. Hogue and Mr. Walsh.

“Such a strengthening in growth, however, clearly is contingent on our outlook for oil prices being realized.”

They expect economic growth of 2.2 per cent in Alberta and 1.7 per cent in Saskatchewan “as energy revenues begin to recover and confidence starts to rebuild following two very difficult years in 2015 and 2016.”

Newfoundland and Labrador is another matter, its economy projected by RBC to contract by 2.2 per cent.

“A recent pick-up in oil production is poised to bring a temporary pause to the two year-long contraction in Newfoundland and Labrador’s economy in 2016; however, we expect that the continued souring of conditions in other sectors, as well as a fall in capital investment spending and persistent fiscal austerity at the provincial level will be dominant forces causing the contraction to resume with even greater intensity in 2017,” Mr. Walsh said.

Speaking of intensity, oil prices will of course also factor into the performance of stock markets that are already on a notable run.

Markets

Stock markets have been riding high, in some cases to record levels, in the wake of the Trump victory, envisioning a bump in U.S. economic growth.

Can that last as Mr. Trump takes office and investors get some clarity on what, to this point, has been a vague agenda?

“When it becomes evident to both investors and Congress that growth can’t sustain a 2-per-cent-plus pace, the mood will change quickly,” warned Benjamin Tal, deputy chief economist at Canadian Imperial Bank of Commerce.

Market observers obviously have different forecasts for how major stock indexes will fare next year, again citing the Trump uncertainty.

But BMO’s Mr. Porter noted that the S&P 500 would mark its ninth consecutive gain should the key stock index record a positive total return. That would rival the longest run ever, he added, recalling the 1991-99 surge in the tech sector.

“Admittedly, this streak is holding up on a technicality, as only dividends kept equity returns in the black in 2015 and 2011, but the longevity of the bull market is indeed impressive,” Mr. Porter said.

“Stocks will face the usual wall of worry next year, with rates rising, robust valuations and a new array of political uncertainty,” he added.

“But if the new administration can indeed deliver even a modest helping of stimulus, a lighter regulatory touch, some tax relief on earnings repatriation, and avoid serious protectionism, growth could surprise on the high side. That’s not asking too much, is it?”

As for Canada’s S&P/TSX composite, here’s Mr. Porter’s “stretch call” as the index nears its own record: “TSX 18,000? (i.e., essentially a repeat performance of the crackling gains seen in 2016.)”