The Bay Street financial district is shown in Toronto on Aug. 5, 2022.Nathan Denette/The Canadian Press

If 2022 was a bad year for Bay Street, the first three months of 2023 were worse.

The total value of new stock issues in the first quarter fell 36 per cent to $2.6-billion from $4.1-billion year-over-year, according to financial data service Refinitiv. Compared with the most recent 10-year first-quarter average of $10.6-billion, the start of this year was down an even more precipitous 75 per cent.

“Markets remain challenged, there is no doubt about it,” said Chris Blackwell, managing director and head of investment banking at Canaccord Genuity Group Inc. CF-T, which placed a close second behind Scotiabank as the top investment bank for stock deals in the first quarter of 2023. Natural resources companies, particularly miners focused on critical minerals such as lithium, “have been the lone bright spot in the first quarter and continue to be so today,” he said.

More than two-thirds of stock sales in the first quarter – 84 of 121 deals – were done by mining companies, as demand for key components of low-carbon technologies such as electric vehicle batteries remained strong. Canaccord has a leading mining franchise, Mr. Blackwell said, “and that was where there was a lot of traffic and a lot of interest.”

Merger and acquisition activity, despite being a bright spot amid an otherwise gloomy 2022, also declined on both a year-over-year and longer-term basis. Total deal value for the first three months of 2023 was US$35-billion, down 53 per cent from US$73-billion and 44 per cent below the most recent 10-year average of US$63-billion.

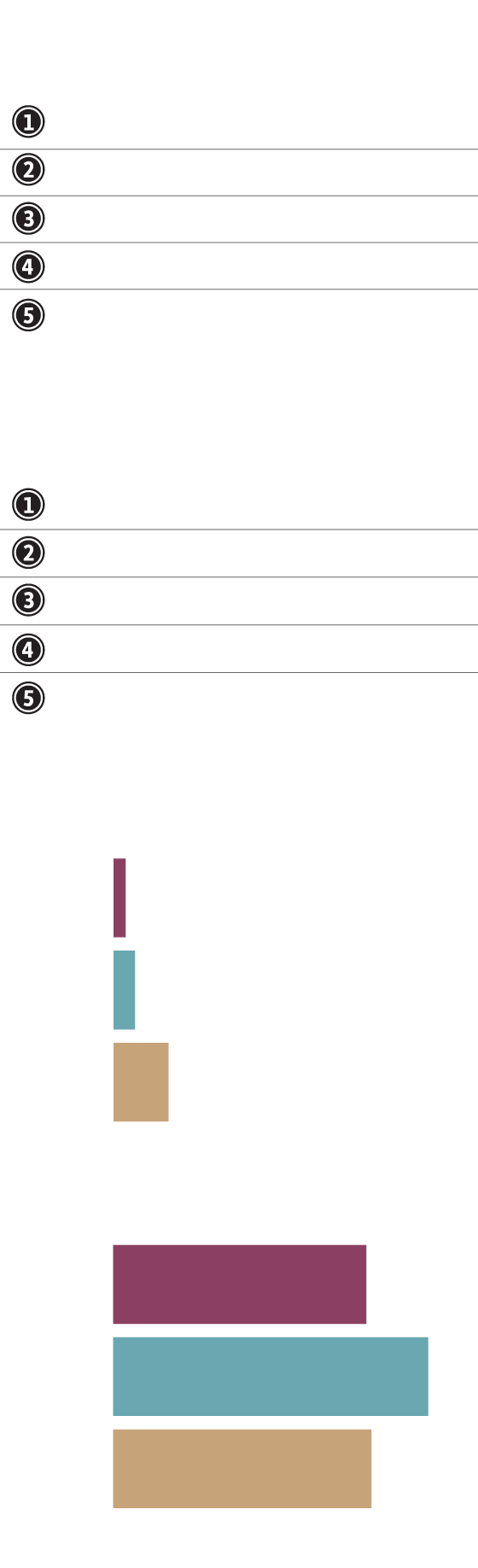

Top banks for equity underwriting

Value

(millions)

No. of

issues

Rank

Banks

Scotiabank

$328

5

Canaccord Genuity Group

327

9

BMO Capital Markets

229

9

BofA Securities

194

1

National Bank of

Canada Financial

193

3

Top banks for debt underwriting (total)

Value

(billions)

No. of

issues

Rank

Banks

RBC Capital Markets

$10.8

51

Scotiabank

7.9

33

TD Securities

7.8

44

CIBC World Markets

7.7

50

National Bank of

Canada Financial

6.9

64

TOTAL EQUITY

Value ($ billions)

Q1 2023

2.6

4.1

Q1 2022

10yr avg

Q1 2013–

Q1 2022

10.6

TOTAL DEBT

Value ($ billions)

Q1 2023

49

61

Q1 2022

10yr avg

Q1 2013–

Q1 2022

50

THE GLOBE AND MAIL, SOURCE: refinitiv

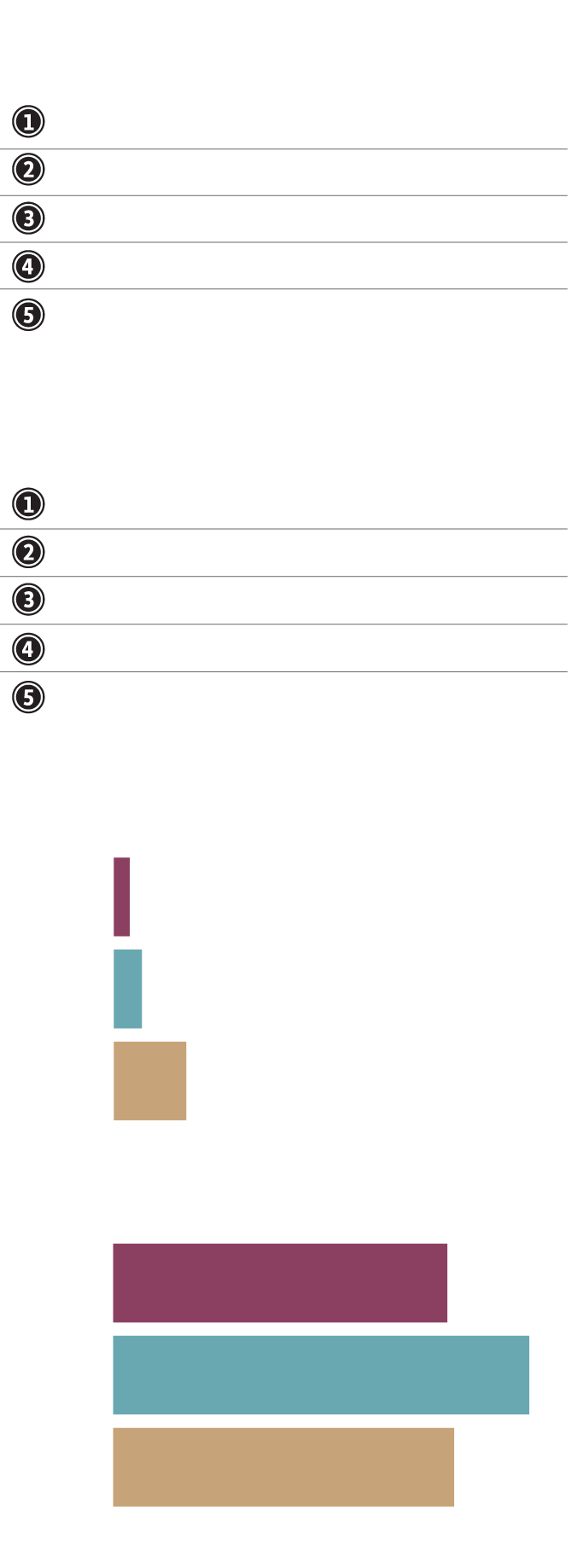

Top banks for equity underwriting

Value

(millions)

No. of

issues

Rank

Banks

Scotiabank

$328

5

Canaccord Genuity Group

327

9

BMO Capital Markets

229

9

BofA Securities

194

1

National Bank of

Canada Financial

193

3

Top banks for debt underwriting (total)

Value

(billions)

No. of

issues

Rank

Banks

RBC Capital Markets

$10.8

51

Scotiabank

7.9

33

TD Securities

7.8

44

CIBC World Markets

7.7

50

National Bank of

Canada Financial

6.9

64

TOTAL EQUITY

Value ($ billions)

Q1 2023

2.6

4.1

Q1 2022

10yr avg

Q1 2013–

Q1 2022

10.6

TOTAL DEBT

Value ($ billions)

Q1 2023

49

61

Q1 2022

10yr avg

Q1 2013–

Q1 2022

50

THE GLOBE AND MAIL, SOURCE: refinitiv

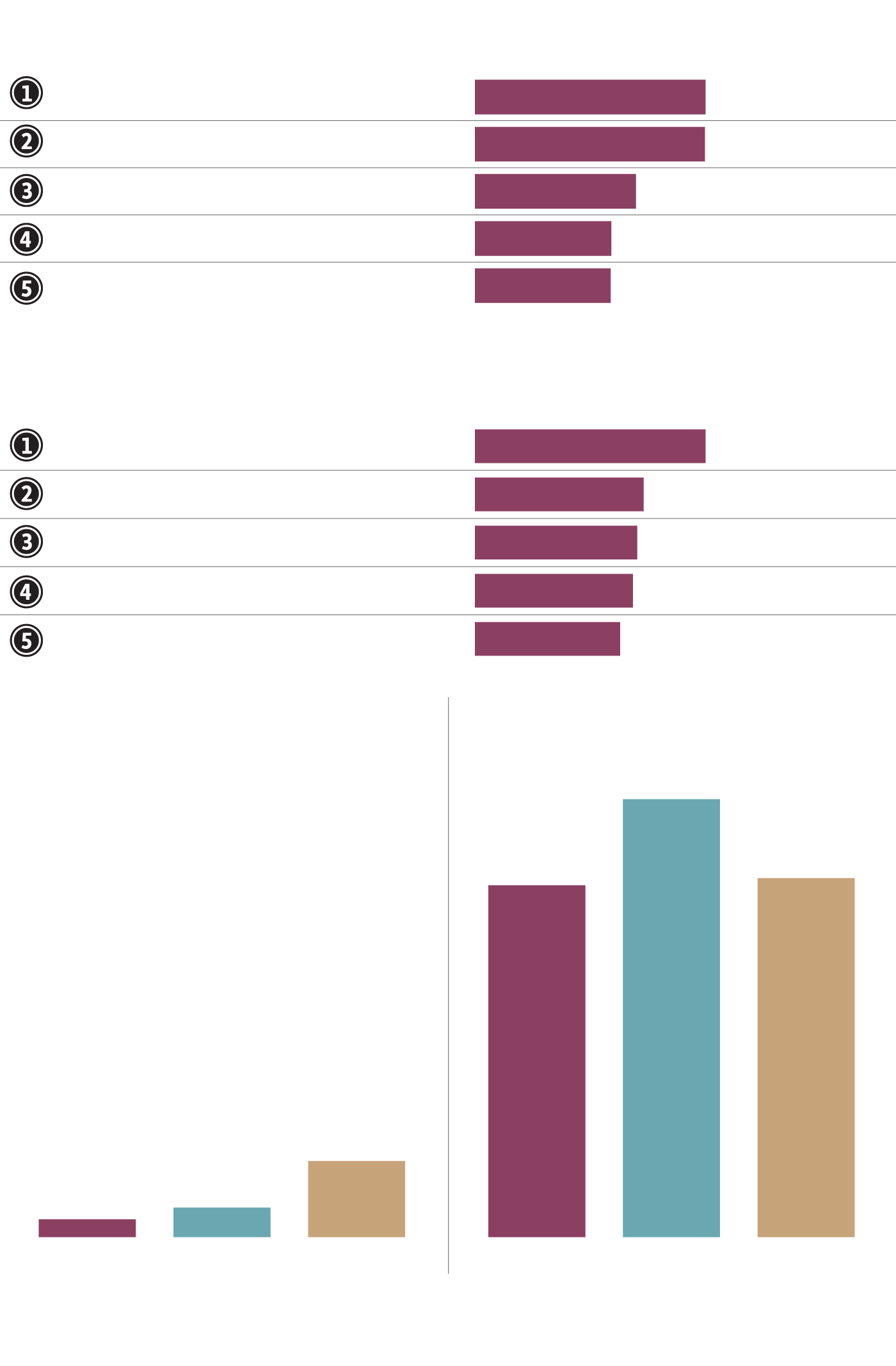

Top banks for equity underwriting

Rank

Banks

Value (millions)

No. of issues

Scotiabank

$328

5

Canaccord Genuity Group

327

9

BMO Capital Markets

229

9

BofA Securities

194

1

National Bank of Canada Financial

193

3

Top banks for debt underwriting (total)

Value (billions)

Rank

Banks

No. of issues

RBC Capital Markets

$10.8

51

Scotiabank

7.9

33

TD Securities

7.8

43

CIBC World Markets

7.7

50

National Bank of Canada Financial

6.9

64

TOTAL EQUITY

TOTAL DEBT

Value ($ billions)

Value ($ billions)

61

50

49

10.6

4.1

2.6

Q1 2023

Q1 2022

10yr avg

Q1 2013 -

Q1 2022

Q1 2023

Q1 2022

10yr avg

Q1 2013 -

Q1 2022

THE GLOBE AND MAIL, SOURCE: refinitiv

“We continue to see a lot of fence sitters in the market looking for direction but not getting any,” Mr. Blackwell said. “And the downside risk that everybody is focused on in both Canada and the U.S. is recession. That is what has caused folks to be more cautious.”

Debt markets, meanwhile, showed surprising resilience during early 2023 in the face of dramatically higher interest rates. While total value of debt offerings – both government and corporate – was down almost 19 per cent compared with the first quarter of 2022, to $49-billion from $61-billion, it was less than 2 per cent below the most recent 10-year first-quarter average of $50-billion.

The corporate debt proportion of total debt showed an even softer decline, falling less than 9 per cent to $17-billion from $19-billion year-over-year. The latest quarterly total was also in line with the most recent 10-year average.

“Rates today are actually far better than even in October of last year,” said Rob Brown, co-head of debt capital markets for RBC Capital Markets, the top investment bank for debt issuances in the first quarter of 2023. “Spreads have moved wider over the course of the year, but given the move in underlying rates it has actually improved all-in funding cost dynamics for non-financial corporate issuers.”

Government of Canada 10-year bond yields, for example, were as high as 3.6 per cent in the final months of 2022 but are under 3 per cent today.

Patrick MacDonald, Mr. Brown’s co-head, said the year-over-year decline in total debt was not representative of the current strength in debt markets, in part because in late 2021 and early 2022 – during the early stages of the historically swift rise in interest rates – issuers were engaged in what he described as “insurance planning.”

That means the companies issuing the debt “didn’t necessarily need the funding, but given all the significant uncertainty, they wanted to ensure their balance sheets were very well capitalized,” Mr. MacDonald said. “As a result, we saw a tremendous amount of interest for new issues in the bond market, and that was met with a tremendous amount of interest from investors.”

Canaccord’s Mr. Blackwell said he is not expecting the comparative lack of interest among equity market participants to last much longer.

“We are signing NDAs and taking information and doing some work around valuation and positioning in anticipation of when we see that market start to turn,” he said. “And as it always does, it is going to turn quickly.”

The inflection point will come, he said, whenever interest rates start to fall.

At a certain point central banks “are going to have to start cutting rates. The million-dollar question is when,” he said. “Is it this fall? Is it next year? That I don’t know, but it will come.”