Party on! Stock markets just want to have a good time and right now they are cranking up the music and ignoring the banging on the walls. Forget the Strait of Hormuz, forget rising inflation. Stock prices are going to the moon.

And why not? The earnings season that is just wrapping up on Wall Street was spectacular, with companies in the S&P 500 index reporting profits that were more than 25 per cent higher than a year ago, according to market maven FactSet. Forecasters from Royal Bank of Canada, HSBC and Yardeni Research have hiked their year-end targets for the S&P 500. More upgrades are probably on the way.

Yes, as hard as it is to stop dancing when the music is still playing so loudly, prudent investors may want to start thinking about getting their coats and planning their rides home. After three years of stellar performance, the market is looking pricey. It is also looking increasingly unbalanced. Rather than spreading its risk widely, it is wagering huge amounts on a single bet – an all-in belief in technology.

As Barron’s noted this week, the tech sector has never been more dominant in the S&P 500 index, not even at the height of the dotcom boom of the 1990s.

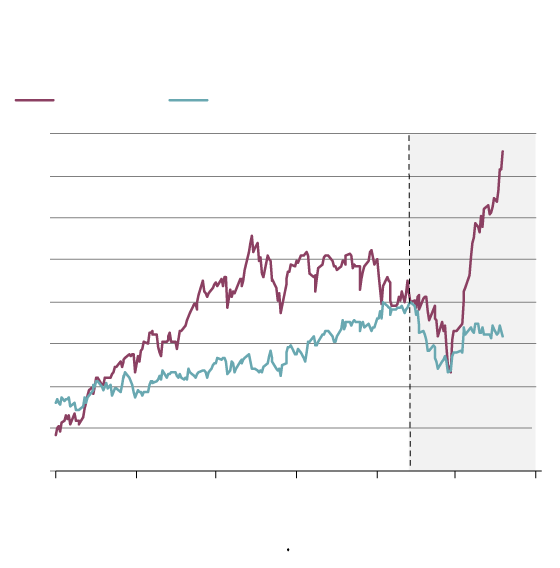

In tech, we trust

Since the start of the U.S.-Iran War, technology stocks have boomed.

(Change in S&P 500 sectors, Feb. 27=100)

Tech sectors

Other sectors, excl. energy and real estate

120

115

110

105

100

95

90

U.S.–Iran War

85

80

June

Aug.

Oct.

Dec.

Feb

.

April

June

2025

2026

.

the globe and mail, Source: Capital Economics

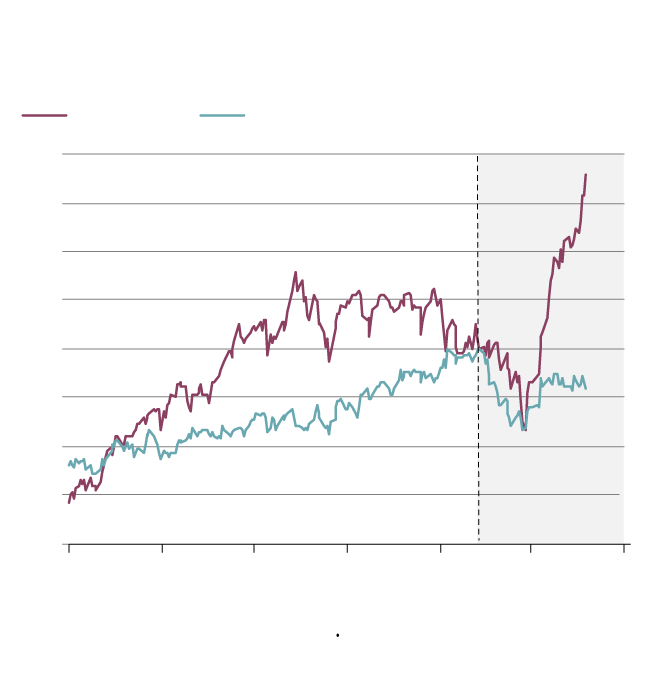

In tech, we trust

Since the start of the U.S.-Iran War, technology stocks have boomed.

(Change in S&P 500 sectors, Feb. 27=100)

Tech sectors

Other sectors, excl. energy and real estate

120

115

110

105

100

95

90

U.S.–Iran War

85

80

June

Aug.

Oct.

Dec.

Feb

.

April

June

2025

2026

.

the globe and mail, Source: Capital Economics

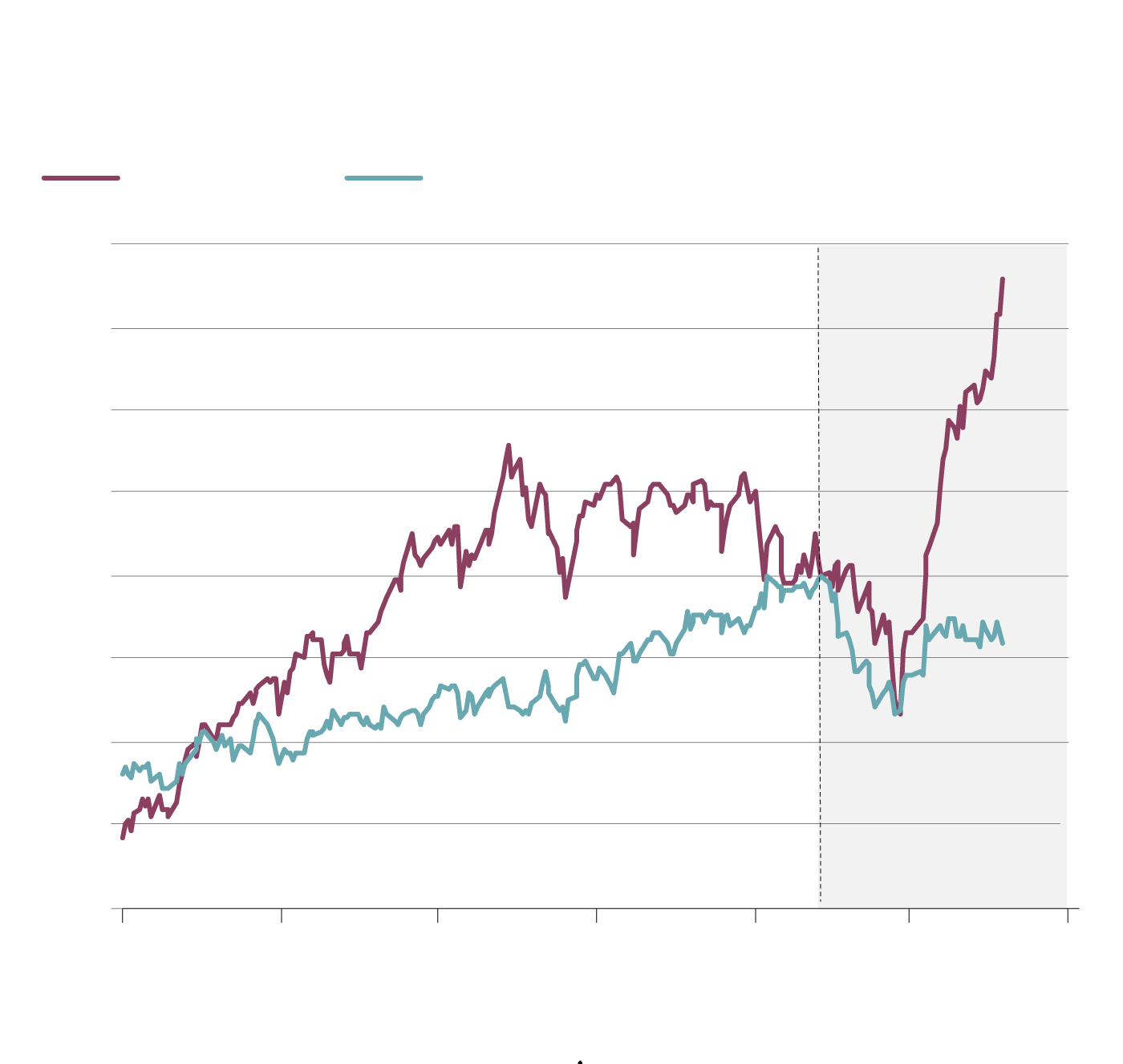

In tech, we trust

Since the start of the U.S.-Iran War, technology stocks have boomed.

(Change in S&P 500 sectors, Feb. 27=100)

Tech sectors

Other sectors, excl. energy and real estate

120

115

110

105

100

95

90

U.S.–Iran War

85

80

June

Aug.

Oct.

Dec.

Feb

.

April

June

2025

2026

the globe and mail, Source: Capital Economics

.

The sector, narrowly defined, now accounts for 37 per cent of the market benchmark’s value. Add in tech-adjacent companies such as Meta Platforms Inc. META-Q, Amazon.com Inc. AMZN-Q and Alphabet Inc. GOOGL-Q, and the tech sector, broadly defined, makes up about half of the S&P’s market capitalization.

The biggest tech companies tower over the broad economy. Nvidia Corp. NVDA-Q, the microchip maker, is worth more than the entire Canadian stock market. It is also worth more than the entire healthcare sector of the S&P 500.

Opinion: The market is not ignoring nothing. It may be underpricing something

Does this make sense? Maybe, but only if you are willing to make some big assumptions.

To justify Nvidia’s value, or the value of the tech sector in general, you have to believe that competitors won’t emerge to challenge its quasi-monopoly. You also have to believe that lavish spending on anything to do with AI will continue, and that enormous expenditures on AI infrastructure will soon begin to generate massive profits, which will then justify even more spending.

There are good reasons to question these assumptions. But at current prices, the market isn’t factoring in much room for doubt.

Consider, for instance, the price-to-sales ratio, a measure of how share prices compare to how much companies are taking in as revenue. It’s a simple, reliable measure of value – and it’s blinking red.

On average, the stocks in the S&P 500 are selling for an average 3.65 times their underlying revenue. That is double the 30-year average of 1.81.

The only way to justify this lofty price-to-sales multiple is to assume that companies are going to start extracting much higher profits from every dollar of their sales. But here’s the thing: They already are. Corporate profits as a share of the overall U.S. economy are sitting at record highs.

If you buy into the S&P 500 at today’s prices, you are making an implicit wager that profit margins will keep on soaring and will reach even more stratospheric heights. You are betting that asset-light, high-margin tech companies will replace lower-margin manufacturers and retailers, and that this shift will reconfigure our notions of what level of profit is sustainable.

This is where things get tricky. The vast amounts of money being spent on the physical side of the AI boom suggest that a permanent boom in profit margins is unlikely.

Opinion: Are eager investors telling themselves an incomplete story about AI?

The big tech investors, or hyperscalers, such as Alphabet and Meta, used to be shining examples of the asset-light business model. Now they are now being forced to spend hundreds of billions of dollars on microchips and data centres to keep up with AI’s insatiable appetite for computing power. Their massive investments in physical infrastructure are changing the economics of their businesses, making them look a lot more like traditional manufacturers.

It’s not yet clear how the hyperscalers will generate a payback on their investments. At this point, AI is fascinating and seductive, but it has yet to result in any surge in corporate productivity or obvious hard-dollar benefits to its users.

One early attempt to gauge the productivity benefits of the new technology by non-profit researcher METR found that software engineers initially felt that AI was helping them do their work 20 per cent faster. When output was measured more precisely, though, it turned out that AI was actually making them 19 per cent slower.

A more recent effort to measure AI’s impact on coding efficiency by software development platform Faros came to broadly similar conclusions. Its analysis found that AI boosts the amount of code being written. It is not always good code, though, and it frequently requires fixing. The bottom line, according to Faros, is: “More code. Declining quality. Accelerating incidents.”

AI will continue to improve and these issues may fade. The point here is simply that the payback from AI could take much longer to materialize than the market is assuming. If so, both the tech sector and the broad market will have to sober up.