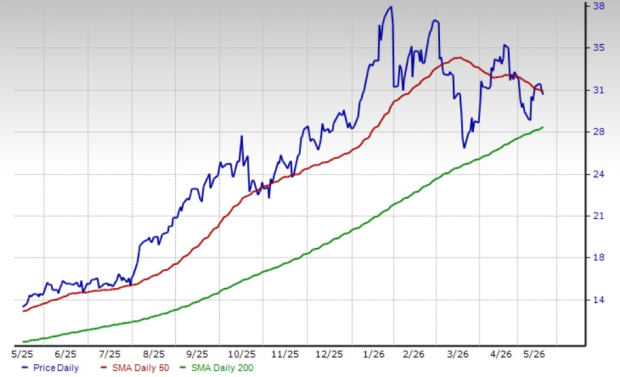

Kinross Gold Slips Below 50-Day SMA: What Should Investors Do Now?

Kinross Gold Corporation’s KGC stock slipped below the 50-day simple moving average (SMA) yesterday, flashing a bearish signal. The pullback is largely a function of the retreat in gold prices on inflation worries stemming from heightened tensions in the Middle East. The downside came despite its better-than-expected earnings in the first quarter, driven by higher realized prices and record margins.

Nevertheless, KGC has been trading above the 200-day simple moving average (SMA) since March 6, 2024, suggesting a long-term uptrend. The 50-day SMA continues to read higher than the 200-day SMA, indicating a bullish trend.

Kinross Trades Below 50-Day SMA

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

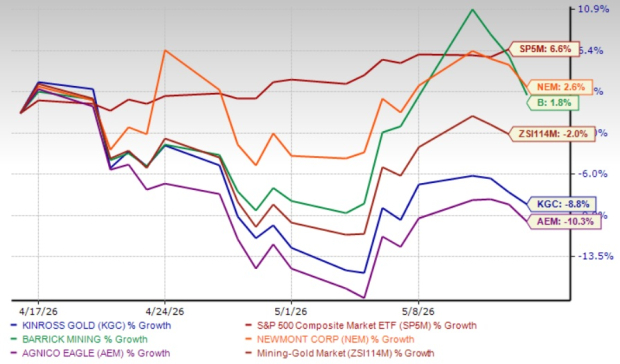

Amid falling gold prices, Kinross’ shares have lost 8.8% in the past month. KGC has underperformed the Zacks Mining – Gold industry’s decline of 2% and the S&P 500’s rise of 6.6%. Its gold mining peers, Barrick Mining CorporationB and Newmont CorporationNEM have gained 1.8% and 2.6%, respectively, while Agnico Eagle Mines LimitedAEM has lost 10.3%, over the same period.

KGC’s One-month Price Performance

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Given the pullback in Kinross’ shares, investors might be tempted to snap up the stock. But is this the right time to buy KGC? Let’s find out.

Development Projects to Underpin KGC’s Production Growth

Kinross has a strong production profile and boasts a promising pipeline of exploration and development projects. Its key development projects and exploration programs remain on track. These projects are expected to boost production and cash flow, and deliver significant value. The successful execution of these projects will position the company for a new wave of low-cost, long-life production.

KGC is progressing with the construction of three organic growth projects to expand its U.S. portfolio. This is aimed at extending mine life and cost optimization. The projects are Round Mountain Phase X and Bald Mountain Redbird 2 in Nevada, and the Kettle River–Curlew project in Washington.

Together, the projects are expected to contribute significantly to Kinross’ U.S. production profile and add a strong value proposition with a combined Internal Rate of Return (IRR) of 59% and a combined incremental post-tax Net Present Value (NPV) of $4.3 billion. They are expected to contribute 3 million ounces of life-of-mine production to KGC’s portfolio, adding grades and mine lives. Kinross Gold is planning to self-fund three growth projects entirely from operating cash flows, reflecting its disciplined strategy.

Tasiast and Paracatu, the company’s two biggest assets, remain the key contributors to KGC's cash flow generation and account for more than half of its production. Both Tasiast and Paracatu delivered solid performance in the first quarter of 2026, with production rising from the prior quarter and both operations remaining on track to meet the company’s 2026 guidance.

Kinross’ Strong Financial Health Backs Capital Allocation

KGC has strong liquidity of $3.9 billion and generates substantial cash flows, which allows it to finance its development projects, pay down debt and drive shareholder value. Kinross reactivated its share buyback program in April 2025. It completed a $600 million share repurchase program as of Dec. 31, 2025. The Toronto Stock Exchange, in March, accepted the notice to renew its normal course issuer bid program. KGC repurchased shares worth roughly $250 million in the first quarter and $300 million this year through April 29.

KGC generated a record free cash flow of roughly $2.5 billion last year. It returned $752.4 million to its shareholders through dividends and buybacks in 2025. The company also logged attributable free cash flow of $837.5 million in the first quarter, marking the fourth straight quarter of record free cash flow. It ended the quarter with about $1.4 billion in net cash.

In 2025, the company repaid $700 million of debt. With $1.7 billion in available credit (as of March 31, 2026) and no debt maturities until 2033, Kinross is well-positioned to support growth while strengthening its balance sheet and delivering shareholder value.

KGC’s board has approved a 14% increase to its quarterly dividend, amounting to 16 cents per share on an annualized basis. Kinross is targeting to return 40% of its free cash flow through share buybacks and dividends in 2026. KGC offers a dividend yield of 0.5% at the current stock price. It has a payout ratio of 7%.

Favorable Gold Prices to Drive KGC’s Margins and Cash Flow

Notwithstanding the recent pullback, still-elevated gold prices should boost KGC’s profitability and drive cash flow generation. While gold prices have fallen from their January 2026 highs, they remain supportive. Geopolitical tensions, a weaker U.S. dollar, tariff threats and concerns over the independence of the Federal Reserve drove bullion to a record high of nearly $5,600 per ounce in late January. This was followed by a brief pullback to below $4,900 per ounce due to aggressive profit-booking and a rebound in the U.S. dollar after hitting a four-year low.

The yellow metal strengthened again in early March, surging past $5,400 per ounce, as safe-haven demand spiked, following joint U.S.-Israel strikes on Iran. A stronger U.S. dollar, inflation fears tied to a spike in oil prices and the Fed’s hawkish tone weighed on gold prices, dragging bullion to near $4,400 per ounce in late March.

Bullion surged to near $4,800 per ounce in early April after the United States and Iran agreed to a two-week ceasefire, leading to crashing oil prices and easing inflation worries. This was followed by another brief pullback on inflation concerns following failed U.S.-Iran ceasefire talks and the announcement of a U.S. naval blockade of the Strait of Hormuz. Gold prices again gained ground, surpassing $4,800 per ounce as oil prices fell on hopes of a U.S.-Iran truce, before slipping to near $4,700 per ounce on continued geopolitical tensions despite the U.S.-Iran ceasefire extension.

Gold further slipped to a one-month low below $4,600 per ounce in late April, stemming from inflation worries from a surge in oil prices amid stalled U.S.-Iran talks and closure of the Strait of Hormuz. Renewed escalation in the Middle East pulled down prices further to around $4,500 per ounce in early May, before climbing back above $4,700 per ounce later last week on hopes of de-escalation and a decline in oil prices. Prices have again fallen below $4,600 per ounce lately amid uncertainties linked to the Middle East tensions and inflation woes, fueling a hawkish shift in interest rate expectations.

Higher Production Costs a Drag on KGC’s Margins

Kinross is exposed to headwinds from higher production costs. It saw first-quarter attributable all-in-sustaining costs (AISC) of $1,732 per ounce, marking a 28% increase from the year-ago quarter. Attributable production cost of sales per gold equivalent ounce was $1,380, up 33% from the prior-year quarter’s levels, in part, due to higher royalty costs. Kinross expects AISC to be $1,730 per ounce (+/-5%) in 2026, indicating a year-over-year increase from $1,571 per ounce in 2025, partly due to inflationary impacts. AISC is expected to be impacted by cost inflation from elevated crude oil prices.

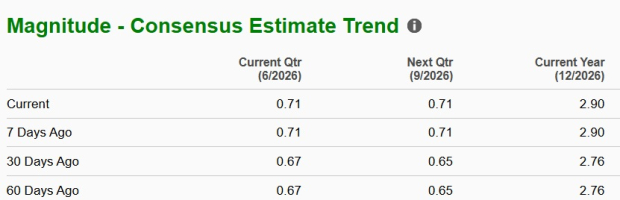

Positive Analyst Sentiment for KGC Stock

Earnings estimates for KGC have been rising over the past 60 days, reflecting analysts’ optimism. The Zacks Consensus Estimate for 2026 and the second quarter has been revised upward over the same time frame.

The Zacks Consensus Estimate for 2026 earnings is currently pegged at $2.90, suggesting year-over-year growth of 57.6%. Earnings are also expected to register roughly 61.4% growth in the second quarter.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

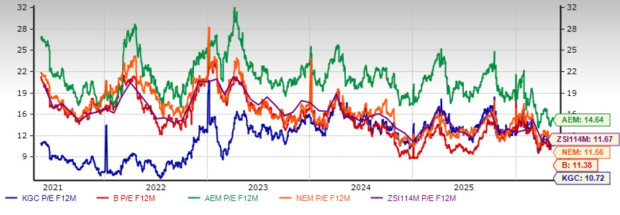

A Look at Kinross Stock’s Valuation

Kinross Gold is currently trading at a forward 12-month earnings multiple of 10.72, an 8.1% discount to the peer group average of 11.67X. KGC is trading at a discount to Newmont, Agnico Eagle and Barrick Mining. Kinross Gold, Barrick Mining and Newmont have a Value Score of B each, while Agnico Eagle carries a Value Score of D.

KGC’s P/E F12M Vs. Industry, B, NEM & AEM

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

How Should Investors Play the KGC Stock?

Kinross boasts a robust development pipeline and a healthy financial position. Upward revisions in earnings estimates and an appealing valuation further strengthen its investment case. The company continues to deliver solid financial results while prioritizing shareholder returns, supported by strong free cash flow generation and rapid deleveraging amid favorable gold prices. However, elevated production costs amid an inflationary environment remain a concern. Retaining this Zacks Rank #3 (Hold) stock will be prudent for investors who already own it.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).