Key Points

10 American companies are worth $1 trillion or more (so far), but only three are in the ultra-exclusive $4 trillion club.

I think Amazon could reach $4 trillion sometime in 2028, thanks to the incredible momentum in its cloud and e-commerce businesses.

Amazon is currently valued at $2.86 trillion, so investors could earn a 38% return from here if it does join the $4 trillion club.

There are 10 publicly listed U.S. companies worth $1 trillion or more, but only Nvidia, Alphabet, and Apple are currently in the ultra-exclusive $4 trillion club. Microsoft was also a member late last year, but its stock has since plummeted.

I think Amazon(NASDAQ: AMZN) could be the next company to cross the $4 trillion mark. Its cloud computing business continues to deliver accelerating revenue growth thanks to artificial intelligence (AI), and its world-leading e-commerce platform is increasingly profitable, boosting the company's overall earnings.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Amazon had a market capitalization of $2.9 trillion as of the market close on Wednesday, May 13, implying a potential 38% return for investors if the company joins the $4 trillion club. Read on.

Image source: The Motley Fool.

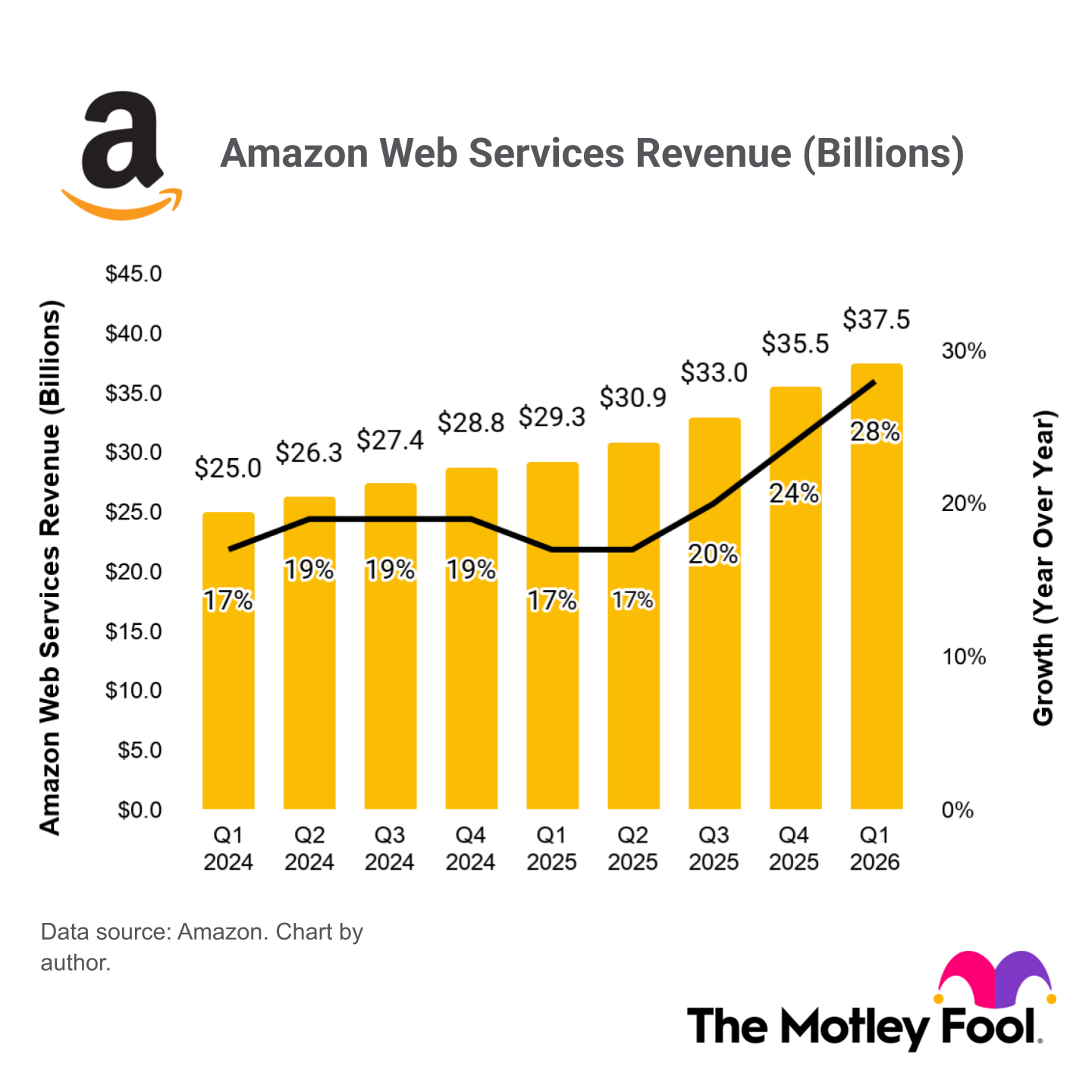

Accelerating growth at Amazon Web Services

Amazon Web Services (AWS) is the world's largest cloud computing platform. It offers hundreds of services to help businesses thrive in the digital age, from simple data storage and web hosting to complex software development and data analytics tools. But it has also become a leading destination for enterprises looking to develop and deploy AI software, which is fueling an acceleration in the platform's revenue growth.

AI is a multilayer opportunity for AWS. First, businesses need computing capacity to deploy AI software, and AWS delivers it through hundreds of data centers strategically located around the world. This infrastructure is powered by thousands of advanced chips from third-party suppliers such as Nvidia, but Amazon also developed its own. The company's latest Trainium2 chip offers 30% better price performance than competing hardware, and the upcoming Trainium3 will deliver a further improvement of up to 40%.

Amazon says it has a whopping $225 billion in revenue commitments from customers looking to rent Trainium chips, making it already one of the most successful product platforms in the company's history.

Then there's AWS Bedrock, where businesses can access the latest ready-made foundation models from top developers such as OpenAI and Meta Platforms to accelerate their AI software development projects. Bedrock had over 125,000 customers at the end of the first quarter of 2026 (ended March 31), and their spending increased by a whopping 170% from the fourth quarter of 2025, just three months earlier.

Overall, AWS delivered $37.5 billion in revenue during the first quarter, a 28% increase from the year-ago period. That growth rate accelerated for the third-straight quarter, highlighting the platform's significant AI-driven momentum.

Even faster growth might be on the horizon, as AWS ended the first quarter with a staggering $364 billion in customer orders awaiting more data center infrastructure to come online. That doesn't even include an additional $100 billion from a recent deal between AWS and AI start-up Anthropic.

E-commerce has become a huge tailwind for Amazon's bottom line

Although most of the attention is rightly on AWS, Amazon's legacy e-commerce business is also quietly booming. Online stores and third-party seller services performed particularly well during the first quarter, as both posted accelerating revenue growth both sequentially and year over year. However, profitability was the real headline.

Amazon's North American and international e-commerce segments combined to deliver $9.7 billion in operating income during the quarter, up 47% from the year-ago period. Back in 2023, Amazon split its American fulfillment network into eight distinct regions to shorten the distance each product travels to reach customers, which continues to reduce the company's logistics costs, thus boosting its profit margins.

But Amazon is also investing heavily in robotics to improve productivity in its fulfillment centers, which is another tailwind for its bottom line.

Amazon has a mathematical path to the $4 trillion club

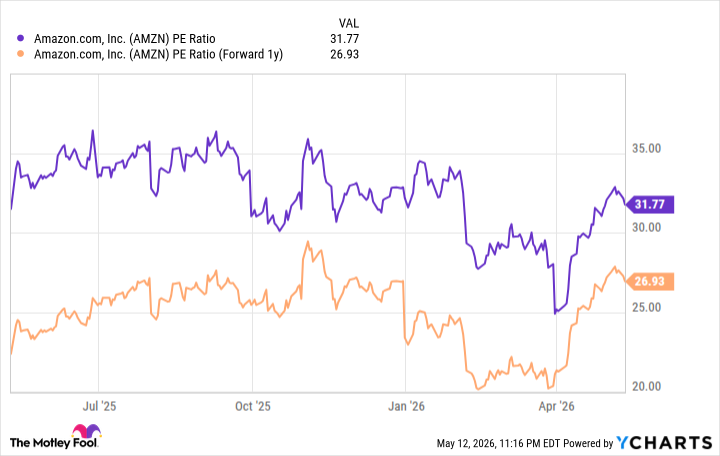

Based on Amazon's trailing-12-month earnings of $8.37 per share, its stock is trading at a price-to-earnings (P/E) ratio of 31.7. It's much cheaper than the Nasdaq-100 index, which trades at a P/E ratio of 35.6, suggesting Amazon might be undervalued relative to its big-tech peers.

Looking forward, Wall Street thinks Amazon can grow its earnings to $9.87 per share in 2027 (according to Yahoo! Finance), placing its stock at a forward P/E ratio of 26.9.

Data by YCharts.

That means Amazon stock would have to climb by 18% before the end of next year just to maintain its current P/E ratio of 31.7, and by 32% to trade in line with the current P/E of the Nasdaq-100. That would place its market capitalization somewhere between $3.37 trillion and $3.77 trillion.

Amazon's P/E ratio was above 35 for a large portion of the past two years, so the high end of that market cap range looks entirely realistic. In that case, the company would have to grow its earnings by only a further 6% in 2028 to justify a $4 trillion valuation. That's a relatively low bar, considering Wall Street predicts its earnings will grow at more than twice that rate in both 2026 and 2027.

In other words, I think Amazon has a great shot at joining the exclusive $4 trillion club sometime in the next two-and-a-half years.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $585,773!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $56,963!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $472,205!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you joinStock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of May 14, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has a disclosure policy.