Antero Resources (AR): Buy, Sell, or Hold Post Q1 Earnings?

Antero Resources has been treading water for the past six months, recording a small return of 1.5% while holding steady at $34.56.

Is there a buying opportunity in Antero Resources, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Antero Resources Not Exciting?

We’re cautious about Antero Resources. Here are two reasons why there are better opportunities than AR, plus one stock we’d rather own.

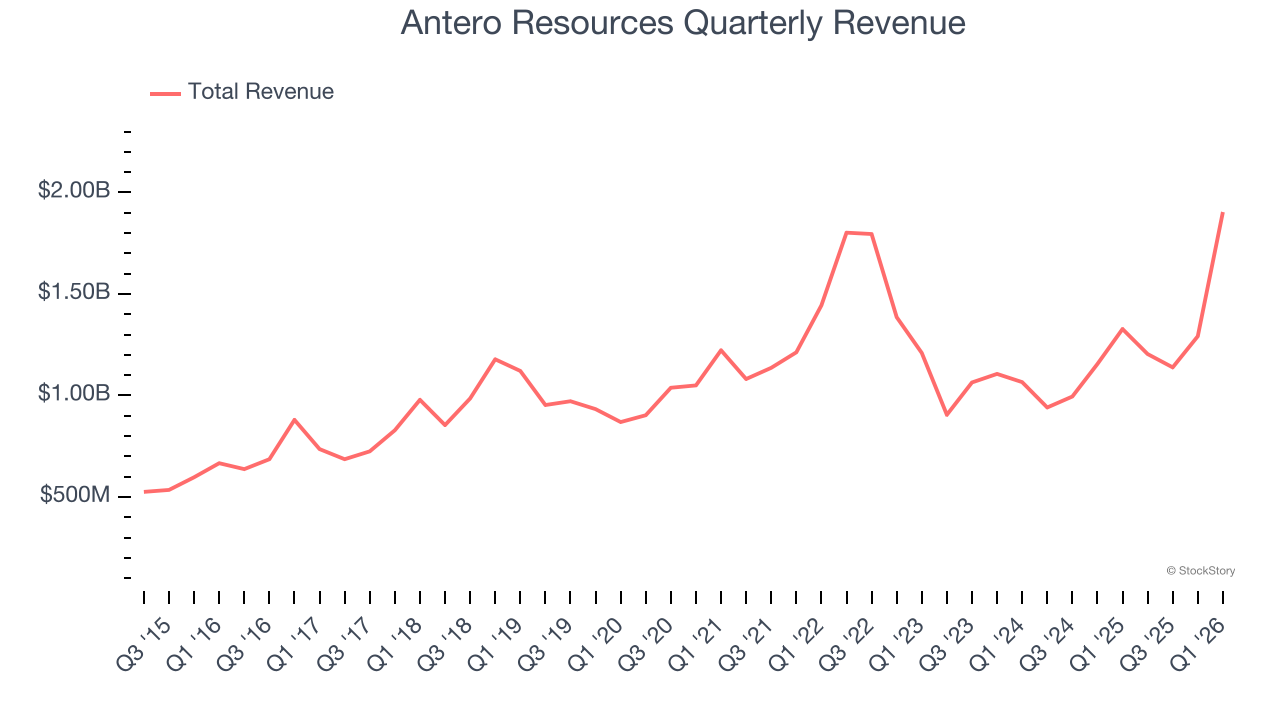

1. Long-Term Revenue Growth Disappoints

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Regrettably, Antero Resources’s sales grew at a sluggish 5.6% compounded annual growth rate over the last five years. This fell short of our benchmark for the energy upstream and integrated energy sector.

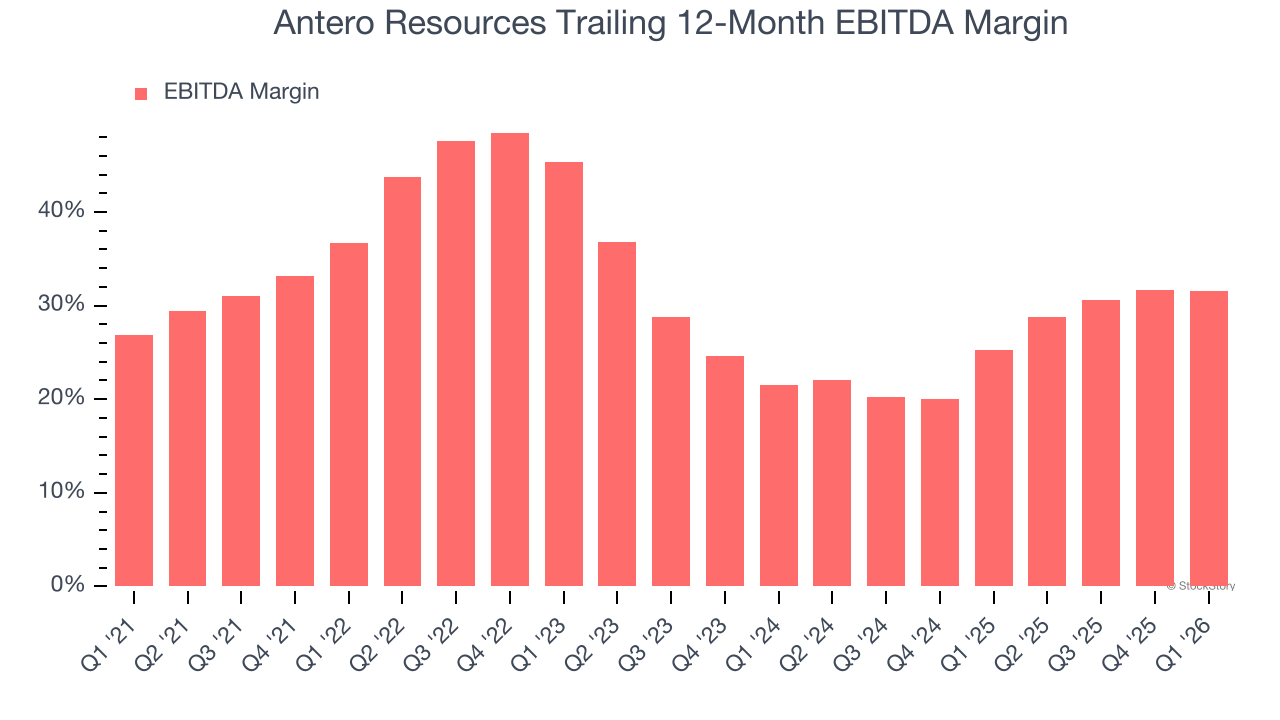

2. Shrinking EBITDA Margin

Adjusted EBITDA margin strips out accounting distortions tied to depletion and historical drilling spend, providing a clearer view of the cash-generating power of the underlying asset base before financing and reinvestment decisions.

Analyzing the trend in its profitability, Antero Resources’s EBITDA margin decreased by 5.1 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its EBITDA margin for the trailing 12 months was 31.6%.

Final Judgment

Antero Resources’s business quality ultimately falls short of our standards. That said, the stock currently trades at 7.8× forward P/E (or $34.56 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We’re fairly confident there are better stocks to buy right now. We’d suggest looking at one of our top software and edge computing picks.

Stocks We Like More Than Antero Resources

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.