Is Atlanticus Stock Still Worth Buying After a 71% Rally in a Year?

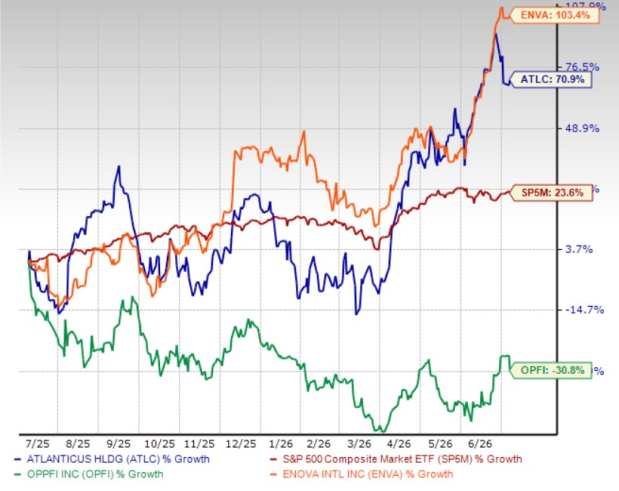

Atlanticus Holdings CorporationATLC has delivered a strong rally, with shares surging 70.9% over the past year compared with the S&P 500 index’s rise of 23.6%. Its peers, Opportunity Financial LLCOPFI has declined 30.8% while Enova International, Inc.ENVA has advanced 103.4% over the same period.

Price Performance

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The sharp rally raises an important question for investors: Is ATLC still worth buying at the current levels, or has much of the upside already been priced in? To answer this, let us assess the company’s growth drivers, earnings prospects, valuation and potential risks before deciding whether to buy, hold or wait for a better entry point.

ATLC’s Revenue Growth Momentum Remains Strong

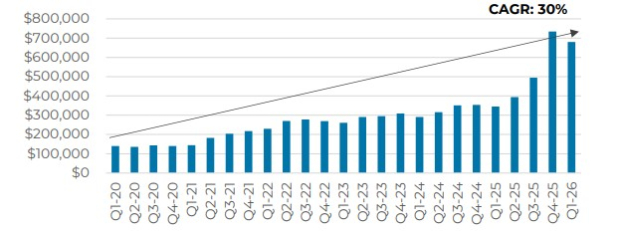

Atlanticus has demonstrated a clear acceleration in revenue growth, supported by higher managed receivables, expanding account volumes and the contribution from the Mercury acquisition, which was completed in the third quarter of 2025. Total operating revenues saw a compound annual growth rate (CAGR) of 30% from the first quarter of 2020 to the first quarter of 2026. This reflects the strength of the company’s enlarged platform and continued receivable expansion.

Revenue Growth Trend

Image Source: Atlanticus Holdings Corporation

The Mercury acquisition added a sizable general-purpose credit card portfolio, including $3.2 billion of receivables and 1.3 million serviced accounts, materially expanding Atlanticus’ revenue base and strengthening its position in the credit card market.

Atlanticus’ top line is expected to benefit from continued growth in general-purpose credit card receivables, higher marketing-led customer acquisition and ongoing contributions from the Mercury portfolio.Management expects general-purpose credit card receivables to continue growing through 2026 and outpace private-label credit receivables. This growth is likely to be supported by expanded marketing initiatives, as well as product, policy and pricing changes within the Mercury portfolio. These initiatives are expected to improve yields and support revenues in 2026 and beyond, though the full impact may take several quarters to materialize.

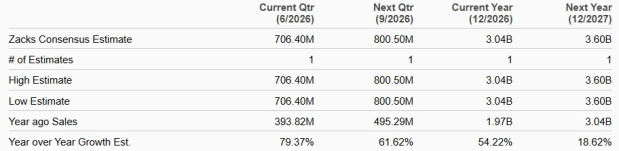

Reflecting this momentum, the Zacks Consensus Estimate for Atlanticus’ 2026 and 2027 revenues indicates year-over-year growth of 54.2% and 18.6%, respectively.

Sales Estimates

Image Source: Zacks Investment Research

Customer Expansion & Market Opportunity Support ATLC’s Growth

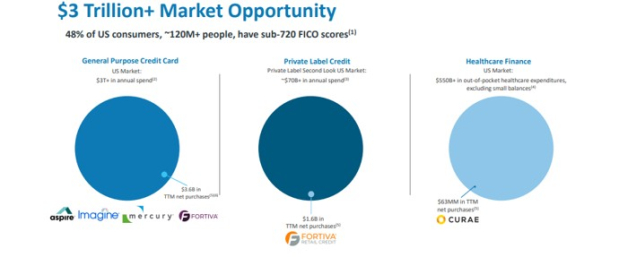

Atlanticus’ customer expansion is supported by a sizable and underpenetrated market opportunity. The company estimates a $3-trillion-plus addressable market, spanning nearly 48% of U.S. consumers across categories such as general-purpose credit cards, private-label credit and healthcare finance.

Total Addressable Market

Image Source: Atlanticus Holdings Corporation

The company’s strategic actions have strengthened its ability to pursue this opportunity. The Mercury acquisition added scale, technology, origination capabilities and 1.3 million serviced accounts. Separately, the Vive portfolio acquisition added roughly $165 million of retail credit receivables and deepened Atlanticus’ relationships with major retail partners.

ATLC’s growing account base indicates that the company is capturing this opportunity at a greater scale. It served 6 million accounts by the first quarter of 2026 and added more than 600,000 accounts during the quarter. This marked a sharp improvement from 415,000 new accounts and 3.8 million total accounts served in the first quarter of 2025.

Overall, the expanding customer base improves Atlanticus’ revenue visibility by increasing the number of accounts that can generate interest income, fees, interchange and servicing revenues. With a larger platform, broader partner relationships and a sizable addressable market, the company appears well-positioned to continue increasing accounts served, which will support long-term earnings growth.

ATLC’s Technology-Led Model Creates Operating Leverage

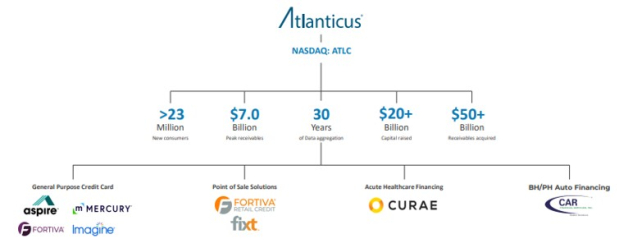

Atlanticus’ technology-led credit-as-a-service platform remains a key source of operating leverage. The platform allows the company to scale receivables, accounts and partner integrations without requiring a proportionate increase in infrastructure. It is supported by 100% automated decisioning, 100% cloud-based infrastructure and API-first integration capabilities, enabling bank, retail and healthcare partners to offer credit products across multiple channels, including general-purpose credit cards, point-of-sale financing and healthcare finance.

The company’s analytics platform is further supported by more than 40 active models in production and 40 billion cells of proprietary model training data. This enables AI/ML-driven decisioning and more targeted underwriting across economic cycles.

This technology foundation supports growth and efficiency. In the first quarter of 2026, Atlanticus highlighted that its platform had acquired more than $50 billion of receivables, served more than 23 million new consumers, raised more than $20 billion in capital and reached peak receivables of approximately $7 billion. The company’s ability to combine data, automation and capital access allows it to expand customer acquisition while maintaining focus on unit-level profitability.

Credit-as-a-Service Platform

Image Source: Atlanticus Holdings Corporation

Operating leverage is also visible in servicing efficiency. While expenses have increased alongside receivables growth and the Mercury acquisition, Atlanticus has reported reductions in servicing costs per account due to economies of scale and greater automation.

ATLC’s Earnings Prospects & Valuation Analysis

Analysts remain bullish on Atlanticus’s earnings outlook. Over the past 60 days, the Zacks Consensus Estimate for 2026 and 2027 earnings has moved upward. The 2026 and 2027 earnings estimates imply year-over-year growth of 52.2% and 37.7%, respectively.

Estimate Revision Trend

Image Source: Zacks Investment Research

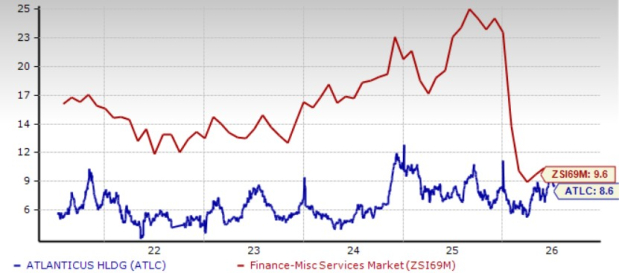

Despite its strong share-price rally, the company continues to trade at a discount to the industry. The stock is currently trading at a forward price-to-earnings ratio of 8.60X, below the industry average of 9.60X. ATLC is trading at a premium compared with Opportunity Financial while trading at a discount compared with Enova International. Opportunity Financial trades at a forward P/E of 4.52X, whereas Enova International trades at 12.85X.

Price-to-Earnings F12M

Image Source: Zacks Investment Research

Conclusion: Buy ATLC Stock Right Now

Atlanticus appears well-positioned for further upside, making the stock a compelling buy despite its strong rally over the past year. The company is benefiting from robust revenue growth, rapid customer additions, a large underpenetrated market opportunity and meaningful scale from the Mercury acquisition. Its technology-led credit-as-a-service platform supports operating leverage, while continued growth in general-purpose credit card receivables and expanded marketing efforts are expected to strengthen its top-line momentum.

The stock’s investment case is also supported by improving earnings and revenue expectations. Moreover, ATLC trades at a discount to the industry, indicating that its growth potential is not fully priced in.

While investors should continue to monitor funding costs, credit quality trends and Mercury integration risks, Atlanticus’s expanding receivables base, strong customer growth, operating leverage potential and favorable earnings outlook support a buy stance on the stock.

At present, ATLC sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>This article originally published on Zacks Investment Research (zacks.com).